Inflation is generally expected to peak at some point over the next several months. Or at least in a few key developed economies.

The UK isn’t one of them, but the US is. Calling the top is everywhere and always a mug’s game, but efforts to identify peak inflation in the post-pandemic era will be remembered as a fool’s errand among fool’s errands — a uniquely hapless escapade even as economic forecasting goes.

Some suggested the cooler-than-anticipated monthly read on average hourly earnings that accompanied the April jobs report was further evidence to support a peak inflation narrative in America. The same might be said of March’s monthly core CPI print, which also came in lower than anticipated.

But at this point, the burden of proof is on those suggesting inflation will recede, a remarkable turn of events. Decades of disinflation in the developed world meant that burden rested squarely on the shoulders of those insisting it wouldn’t recede right up until 2022.

Even if inflation (or core inflation anyway) technically peaks in the US, “lower inflation is likely to be ‘transitory’ given the biggest macro story of 2022,” BofA’s Michael Hartnett said. The reference to “transitory” was a joke at the expense of too many economists, for whom that word is now profane. The “story” Hartnett referenced revolves around supply shortages for four things: Energy, food, housing and labor.

Let’s take natural gas as a proxy for energy. Prices in Europe are hostage to war headlines, so perhaps it’s better to look at prices in the US, which are perched near the highest in 13 years (figure below).

Inventories are low, exports have surged and shale drillers are slow to act. “If this is what it looks like in May, what does it look like in the peaks of summer?”, one former Citadel trader wondered, during remarks to Bloomberg. He suggested a “cold start” to winter might “create some extreme price moves.”

As for food, global prices are the highest on record. The conflict in Europe’s “breadbasket” threatened to transform and already perilous situation into an outright crisis. Now, soaring fertilizer prices may push food costs even higher while crimping yields. Natural gas is a crucial feedstock for nitrogen fertilizers (the most used fertilizers globally) and sanctions have impacted potash production.

A composite gauge compiled using fertilizer benchmark prices of US Gulf Coast Urea, US Cornbelt Potash and NOLA Barge DAP, and value-weighted based on annual global demand, has nearly quadrupled over the past two years (figure below).

As the cost of food production goes up, the supply of food goes down, pushing prices higher still, BofA’s Hartnett cautioned. “Food prices are seriously vulnerable to super-spikes on poor harvests,” he added.

On the labor front, the supply crisis can be illustrated with one familiar chart. Jerome Powell cited the statistic visualized in the figure (below) on at least three occasions this week while speaking to reporters following the largest Fed rate hike in two decades.

There are nearly two job openings for every American counted as officially unemployed.

That represents the most acute labor shortage in modern US history, and it isn’t going to resolve quickly. The longer it takes to normalize, the longer wage pressures will persist. If consumer prices don’t come down, scarce workers, recognizing both their own plight (characterized by falling inflation-adjusted incomes) and the plight of their employers (who are desperate to hire and retain labor), will demand more money. That could feed a wage-price spiral, as companies seek to pass along rising wages to consumers via higher prices.

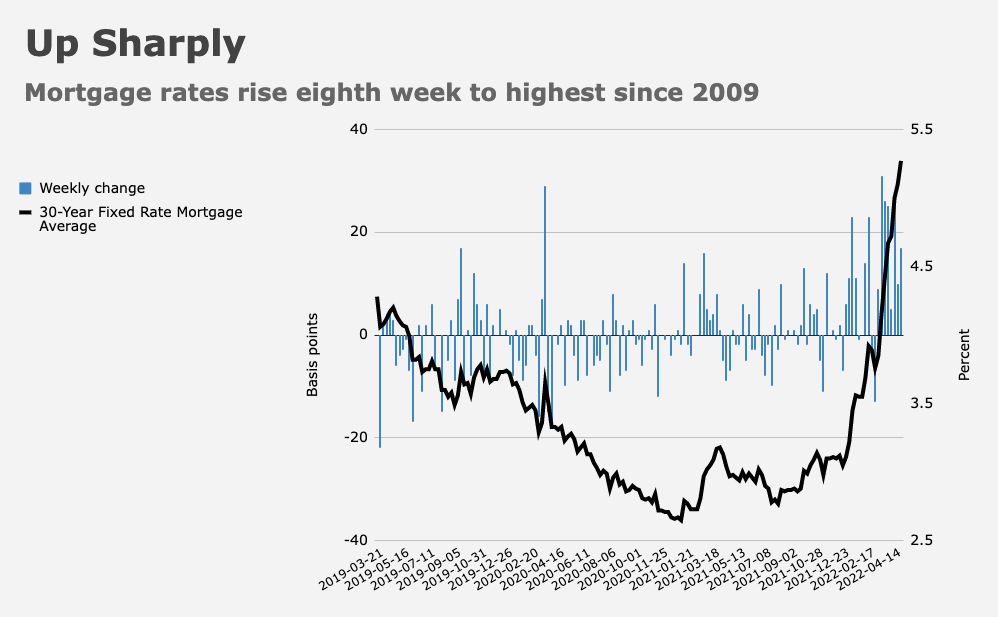

Finally, we turn to housing. Although the cost of homes may start to come down as borrowing costs surge (mortgage rates just rose an eighth week to the highest since 2009), the vast majority of US mortgages are fixed rate, and besides, supply is still an issue and demographics should support demand.

The figure (below) is poignant. Permits are the highest in almost 50 years but inventories are near record lows.

Of course, there’s a point beyond which the only housing statistics that matter are current mortgage rates and prices. People can’t buy what they can’t buy (to adapt a familiar tautology).

Let me expand on that briefly. “Regular economic people,” as Powell called average Americans this week, can’t afford to finance half-million dollar homes in an environment where mortgage rates are rising inexorably over a very compressed time frame. Past a certain threshold, the math simply won’t work.

Analysts in advanced economies always view the world through the lens of developed markets, which leads them to employ the following sort of logic: Millennials need houses, housing supply is constrained, so demand will remain robust. That’s true, right up until it isn’t, which brings us full circle.

When people starve, or freeze to death, it’s not because they failed to recognize the desirability of feeding themselves and keeping warm. A little demand destruction wouldn’t be the worst thing in the world for overheating housing markets in advanced nations. When it comes to food and energy prices, though, we’re compelled to drop the jargon and stop speaking in euphemisms.

In the developing world (and especially in frontier economies), “demand destruction” vis-à-vis food is starvation. For the lowest-income Europeans, “demand destruction” vis-à-vis energy is freezing. Maybe not to death, but 246 Texans would doubtlessly attest to that risk if only they were available to be interviewed.

{kind=link}

H —

You titled the previous story characterizing the financial markets in terms of being a “doomsday machine.” With apologies to Crocodile Dundee, what you describe above is a real doomsday machine.

I hadn’t heard the 246 figure before. That # is shocking