The pandemic era continues to be a market trivia lover’s delight.

Seemingly every week we get a new “since” or “only” moment. For example, after last week, big-cap US tech is averaging a +/- 1.5% close-to-close daily move for December (figure below). That’s only occurred in five Decembers since 2000.

Tech is being pulled this way and that by the ebb and flow of the macro, Fed communications, hedging dynamics and idiosyncratic news, as well as concerns about valuations and sensitivity to bond vol.

It’s confusing. Maddening, even. And market participants are beginning to sound like Donald Trump rambling to Maria Bartiromo after pulling an all-nighter on Twitter.

“I don’t have conviction. And I think a lot of investors are like that,” one strategist told Bloomberg’s Lu Wang. “They look at the world and they have a view. But it’s not a powerful view.” (“You see what’s happening, Maria. And the people — they see it too. And they’re not happy about it. That I can tell you.”)

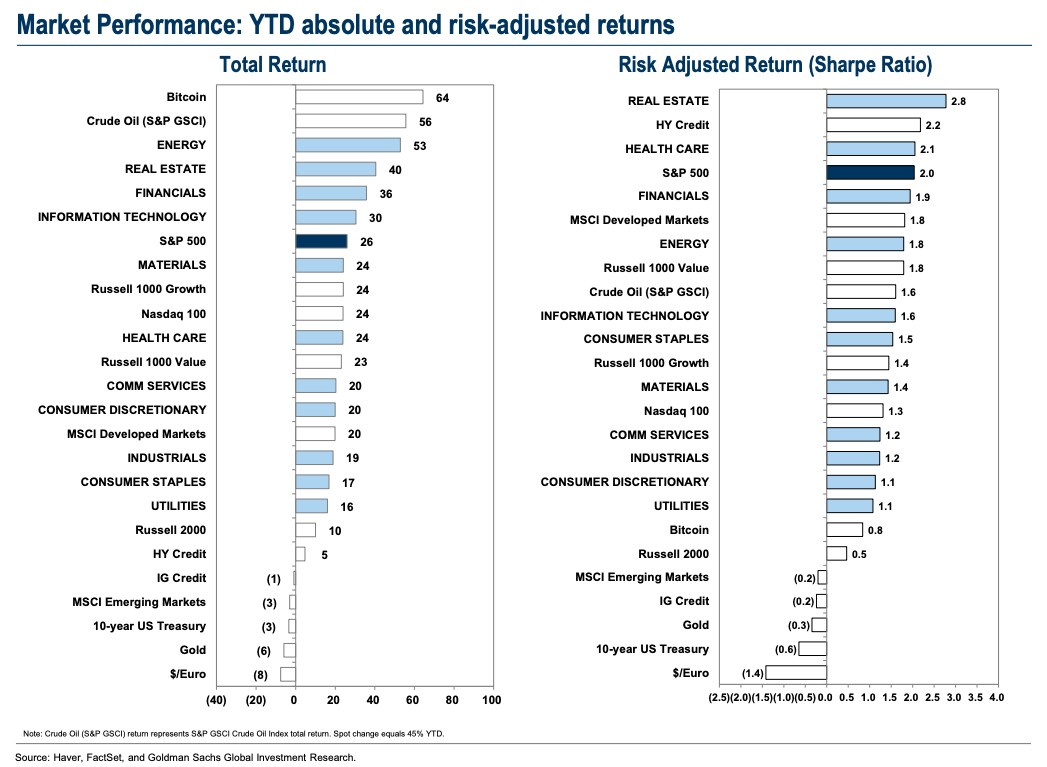

One statistic that isn’t a “since” or an “only” factoid is the S&P’s stupendous 2021 return. Over the past century, US equities have risen 20% during a calendar year about 25% of the time. The figure (below) shows you what’s worked this year.

For all the talk of cash being “trash,” you could’ve done worse. You could’ve owned gold. Factor in the cost of storing it (or the expense ratio associated with owning the paper version) and cash was probably a better bet, even adjusted for soaring inflation. After all, you can securely store a lot of cash in a small, inexpensive safe. If you’ve got a lot of gold, you need to find your own Erebor.

I suppose you could argue gold’s fantastic 2020 returns were the market anticipating 2021’s inflation, but there are surely some disillusioned bullion bulls out there. Inflation is running the highest in 40 years and gold is the worst-performing asset on the board. (Instead of adding to my existing gold position this year, I bought crypto. I had too much gold for my liking anyway.)

Speaking of inflation, BofA’s Michael Hartnett suggested it presages a recession. “Inflation always precedes recessions,” he wrote, in the latest edition of the bank’s popular weekly “Flow Show” series. “Whether driven by asset, housing, commodity, consumer or labor, inflation is like a very high body temperature and must be reduced via tightening or recession to return the body to normal and ensure future good health,” he added.

For what it’s worth, the odds of the S&P rising in 2022 are very, very low, if past is precedent. Just five times since 1927 has the benchmark notched gains in four consecutive years.

If stocks do fall next year, investors and PMs can take solace in having just enjoyed what, in risk-adjusted terms, was one of the best years ever.

“According to Benjamin Franklin, only death and taxes are for certain, but in retrospect, 2021 has been as near-certain a year as an equity investor could imagine,” Goldman’s David Kostin wrote Friday afternoon, adding that although “two weeks still remain, the S&P 500 has… posted a risk-adjusted return [that] ranks in the 79th%ile since 1987.”

Note that Bitcoin’s mammoth surge looks less impressive on a risk-adjusted basis.

Kostin underscored the notion that ambiguity reigns. “Macro uncertainty abounds as investors look to the new year, led by the path of the Omicron variant, geopolitical tensions and both monetary and fiscal policies.”

Hartnett’s view admits of less equivocation. “With just 6% of investors forecasting a recession in 2022, the risk that a ‘rates shock’ quickly morphs into a ‘recession scare’ is high,” he said. “We remain defensive and bearish until positioning shows full-blown capitulation and/or credit events/losses on Wall Street force central banks to announce a reversal of tightening.”

H-Man, this market has more diverse opinions about 2022 than Doans has pills.

High volatility suggests that it is prudent to consider lowering your risk, even if you are an irrelevant upper middle class owner of equities.

King Kong vs Godzilla … Bulletproof market vs Full blown capitulation … coming soon to 2022 … or 2023, … or 2024 …

I took the news that you were long crypto in stride, but learning that you’re long “shiny metal doorstops” (to quote a pundit who shall remain nameless) is giving me major cognitive dissonance.

I mean, you kinda have to have some gold. You can’t have a sizable portfolio and have no gold, where “no gold” means literally nothing allocated to it at all.

I’d like to push back on that. I’m not sure Gold improve any metrics in a portfolio… I think direct real estate exposure has, fairly correctly, become a substitute for both bonds and ‘safety’/inflation hedges (just don’t invest for cap gains, invest solely for the cash flows). I say ‘direct’ rather REITs b/c REITs tend to correlate with equity…

Now most people can’t have a diversified portfolio of direct real estate (too expensive even if you’re just doing resi. let alone if you add commercial/industrial assets) but if you have a sizeable portfolio to manage…