I have no idea why anyone takes the Fed’s semi-annual financial stability report seriously.

Mark Cranfield, a charmingly plainspoken member of Bloomberg’s live-blogger team, put it best early Tuesday in Asia when he told the network’s Hong Kong anchors that no matter how scrupulous (or not) the Fed is at identifying risks, they’re “not likely to do anything about it.”

That’s especially true of equities. Post-financial crisis, traders have learned to view the Fed as an ally. Note that an ally is something different from a co-conspirator. There’s no mystery around the dynamic and depending on how you define unscrupulous behavior, there’s no skulduggery either. The Fed and markets communicate in an open and transparent way, each weighing in on the “proper” course of policy, and considering market participants’ role as co-author of the script, it’s little wonder that the path of least resistance always ends up being a benign interpretation of the data and forward guidance that effectively underwrites carry trades and otherwise supports risk assets. It’s just that simple, and the longer it goes on, the harder it is to go back.

I did want to highlight one section of the November report, though. It was notable that the Fed flagged retail investors, the evolution of market structure and the interplay between social media and the gamification of trading.

“While the services offered on some of the most popular apps are similar to those provided by a traditional stockbroker, these apps make investing more accessible, in part by offering a wider range of products, including the opportunity to easily trade fractions of equity shares or crypto-assets,” the Fed wrote, adding that,

The apps also make trading more visually appealing. Many apps have color-coded graphical layouts that highlight stock movements, mark trading milestones, and have animations celebrating a user’s first stock purchase. With their ease of access and engaging graphics, such apps can make trading seem like a game, particularly for younger or less experienced investors. Consistent with this interface style, among users of trading apps, the average age of account holders is 30 years, and nearly half of them self-identify as first-time investors. The widespread use of large, open social media platforms has also shaped how some retail equity investors communicate about markets. Recent academic papers have shown that social media can increase the information flow to retail investors as well as the amount of “noise” in markets from retail investor trading. In addition, social media can contribute to an “echo chamber” in which retail investors find themselves communicating most frequently with others with similar interests and views, thereby reinforcing their views, even if these views are speculative or biased. More generally, social media platforms allow a single comment or post to reach millions of people and potentially affect market sentiment dramatically within a short period.

None of that is good. Sorry. Not Sorry.

I’ve been over this before, most thoroughly in “The ‘Revolution’ Robinhood And Reddit Are Looking For Happened Years Ago,” but to briefly reiterate: The “democratization” argument (and any attendant pretensions to populist appeal) is a red herring. Markets were over-democratized long before zero commissions and Robinhood. I’ll recycle some language from that linked article.

In August of 2019, assets in US index-based equity mutual funds and ETFs surpassed assets in active stock funds, a shift decades in the making. You can track any number of benchmarks and/or simple, safe strategies using exchange-traded products that cost basically nothing. That’s the democratization of markets. And you can reliably leverage it to outperform the “pros” over long periods, with the obligatory caveat that past performance is no guarantee of future results.

By contrast, Robinhood (and copycat models) is just the expansion of the casino for those inclined to treat markets as an avenue for gambling. Now, the casino is open to everyone at no cost to trade, unless of course you count the value of your order flow which, if you’re a retail investor, you probably didn’t even know had any value, which is why you didn’t ask any questions when brokers started telling you that you could trade for free.

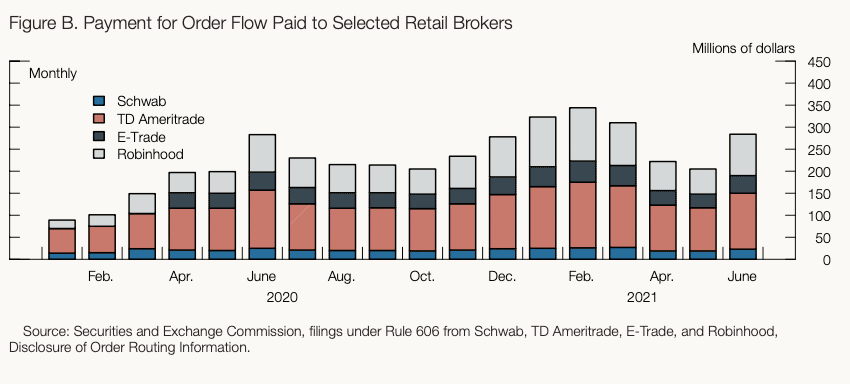

The figure (above) is from the Fed’s report. “Aggregate payment for order flow levels for the retail brokerage firms have recently fallen below the record highs from earlier in 2021, as have trading volumes [but] on a per-share basis, PFOF has continued to rise, which in part reflects a shift in the volumes mix toward options trades, where per-share PFOF is highest,” the Fed cautioned. The most recent leg up in the ongoing rally is being driven, in part anyway, by options.

For (dare I endeavor to put a number on it) millions of newly-minted retail day-traders, the idea that stocks might stop going up and not resume their ascent posthaste is merely theoretical. All they’ve ever known is gains. Many began trading in the months following the original COVID panic. Even the most conservative among these legions of greenhorns would have enjoyed some of the most spectacular returns in a century simply by buying SPY (figure below).

Plainly, that isn’t sustainable. And that’s coming from someone (me) who’s generally argued that due to a hodgepodge of factors, betting against equities continues to be a riskier gamble than riding the proverbial wave.

“Not that there could be any doubt that this is a speculator-driven environment, but the Fed’s inclusion of a special section on Retail speculators confirms it,” JonesTrading’s Mike O’Rourke wrote, of the stability report. “Considering this is an equity market that has gone straight up for 18 months, it makes one wonder how severe the losses would be from a three- to six-month pause, or dare I say it, an actual decline.”

The Fed alluded to that. “Younger stock investors tend to have more leveraged household balance sheets… leaving these investors potentially more vulnerable to large swings in stock prices, as they have a larger debt service burden,” the report went on to say, before noting that the vulnerability “is amplified, as investors are now increasingly using options [while] episodes of heightened risk appetite may continue to evolve with the interaction between social media and retail investors and may be difficult to predict.”

The figure (above) is old news, but it’s still a semblance of poignant.

Whether this is a systemic risk is debatable. The meme stock mania continues to this day and it’s helped resurrect entire companies that might otherwise have run completely out of capital. Retail investors are now acutely aware that through collective action, they have the capacity to shape their own financial future. And they’re becoming more sophisticated in that regard (e.g., “weaponizing” options dynamics).

But it’s important to note that real people have real problems. And when push comes to shove, those problems will take precedence. So, if stocks ever do stop rising and any accompanying shift in retail investor sentiment feeds on itself, engendering despondency and thereby making it more difficult for those still engaged to create critical mass on Reddit and social media, the ensuing lack of joie de vivre could become self-fulfilling. Especially when the bills are due and yesterday’s AMC moguls become today’s Harry Reynards.

As the Fed put it, “a potentially destabilizing outcome could emerge if elevated risk appetite among retail investors retreats rapidly to more moderate levels.”

I’d submit this isn’t a systemic risk despite the Fed’s obligatory mention of Wall Street’s “risk-management systems.” If they can shrug off Bill Hwang (figure below), a million Bill Johnsons shouldn’t be a problem.

The Fed wrote that “relevant financial institutions may not be calibrated for the increased volatility or financial losses that could result” from trends associated with retail investors, social media and the gamification of trading.

I’d wager Wall Street is probably “calibrated” for it and fully prepared to capitalize on it in true predatory fashion. If a few prime clients blow up or otherwise succumb to the marauding hordes, such is life.

The bigger issue for the Fed should probably be the extent to which the gamification of trading is imperiling the financial future of countless twenty- and thirtysomethings. (Of course, the Fed isn’t doing that demographic any favors by helping push up home prices to levels where making a downpayment is impossible for first-time buyers, but that’s a separate discussion.)

Let’s just be honest here: If you need an app styled after a pinball machine to pique your interest and otherwise facilitate your trading activity, it probably means you’re not sophisticated enough even to place a simple Schwab order. If that’s you, you shouldn’t be trading.

You can plausibly blame the Fed for making the casino more appealing by funding the equivalent of an open bar, but there has to be some accountability for the platforms that deliberately encourage risk-taking by people who can’t afford to lose the money.

Vegas was already open to everyone. Just ask E*Trade, which has been running aggressive ad campaigns targeted at would-be day-traders for as long as I can remember. But Robinhood (and its progeny) have effectively put “Clark Griswold Welcome!” on the marquee, surrounded by flashing, multi-colored Christmas lights.

And everyone knows what happens when you take Clark Griswold to a casino. Or put him around Christmas lights.

Teaching 18-year-olds to not be scared of debt by way of student loans may have some unintended consequences.

With apologies H, but the Fed’s view on this is comical at best. For ever, backroom deals and inside information sharing has enabled the “right people” to capitalize on information and coordinate trades. Hell Henry “Hank” Paulson told a bunch of his pals that he was going to force Fannie Mae into conservatorship days before he did so they could all short that behemoth. Now that average Joe’s are openly discussing and coordinating moves, suddenly it’s bad? Come on, it’s bad because the people doing these things aren’t over educated friends of Fed chairs.

As far as the gambling aspect of the current market goes, what the hell do you call buying up every CDO that came to market regardless of how crappy the debt was in them? The big banks gambled like there were no potential consequences with our entire economy and average Joe’s paid with half of their wealth. What price did the gamblers themselves pay? NADA, no jail time, bailouts and bonuses were their prize.

And obviously the final point is this, when this ridiculous Fed fueled bubble does finally pop and all these retail investors lose their entire life savings is the Fed going to do the above for them? Absolutely not! See, the Fed only helps people it knows and those people are the ones that are entitled to coordinated trades and gambling on terrible investments, not retail investors.

Co-conspirators is I agree a stretch but ally really should be given a little more weight here.

Yadda, yadda, yadda.

You’re just regurgitating every article written about the financial crisis over a dozen years.

And you didn’t address any of the points made in this article, including and especially the fact that retail investors are better served by index funds and institutions like Vanguard. Robinhood and platforms like it are, in my opinion, cancerous. Your Whataboutism doesn’t ameliorate that.

Additionally (and most importantly) I spend all day, everyday writing on behalf of, and advocating for, “Average Joe” when I most assuredly don’t have to.

I decided to dedicate my entire life to it starting a half-decade ago. So you can spare me the insinuations.

The idea that Reddit and Robinhood and “social trading” represent the “democratization” of finance is patent bulls–t.

Jack Bogle democratized investing. The rest of this is predatory. These platforms and the venues that pay to access their order flow are preying on retail investors, the VAST MAJORITY of whom will lose money day-trading. When it comes to options, the percentage of new, inexperienced market participants lured in who will lose everything they invest is near 100%.

And that’s the end of this story.

Yes, I am regurgitating every article written about the GFC written over a dozen years. That’s because the GFC SHOULD be remembered for what it was, a statement in support of big banks no matter how many skeletons are in their closet and how much damage they do to society.

I agree that Robin Hood and platforms like it are cancerous. But why is a cancerous financial entity suddenly of interest to the Fed? Is Wells Fargo not a cancerous financial entity? Have they not repeatedly found ways to rip off investors and customers alike? Yet they still exist, with very little regulation, able to continue scheming ways to rip people off. Why is Robin Hood different? Because it enables small time players to execute cancerous trades that have largely been reserved for bigger institutions.

I’m not insinuating that YOU are not for progressive reform, I’ve been a long time reader and I obviously know that you have been advocating for these types of policies for a while. I am merely ranting at the hypocrisy of the Fed for suddenly being concerned about dangers in the financial world because retail investors benefit from them.

I also am not advocating that Reddit and Robinhood are democratizing finance. What I am saying is they are enabling small investors to play the same game that big investors play all the time because they are able to leverage scale. Insider trading, coordinated trades, quid pro quo’s are all bad for markets. The problem isn’t that Reddit and Robinhood exist, the problem is that their mechanisms are not novel, they are just scaled to benefit investors who were left on the sidelines of these types of trades in the past.

Jack Bogle may have democratized investing but he also broke the markets. ETF’s are the polar opposite of intelligent investing and fundamental investors have paid the price since their rise. He is just as responsible for the current state of bubble finance as the Fed is.

“Jack Bogle may have democratized investing but he also broke the markets. ETF’s are the polar opposite of intelligent investing and fundamental investors have paid the price since their rise. He is just as responsible for the current state of bubble finance as the Fed is.”

Oh, ok. So Vanguard is bad now too. So that’s the Fed, Vanguard, ETFs, indexing, banks and then you admitted that Robinhood and platforms like it are cancerous.

So who’s good in your book? Crypto? Where there’s zero accountability, zero oversight, zero intrinsic value and, as far as you know, the entire thing is a Ponzi scheme run by a handful of people who could (very well might one day) crash the entire $3 trillion edifice overnight.

What a joke.

lol Jeez H, why are you so defensive this morning?? Did I say Crypto? No, I didn’t mention Crypto. Now you’re putting words into MY mouth.

A market is supposed to trade something of value. The market itself is not supposed to be the thing that you trade! May as well set up a fund for the US Economy while we’re at it! Hey let’s run a CPI fund and then trade the volume of that too! Do you honestly think all of these investment vehicles make any economic sense? The point of investing is to support something that should make an economic profit. Now we just invest in things that go up and down in numbers and hope we can capitalize on those numbers at the right time. Isn’t the entire thing gambling?

My point with the Fed is this, they are supposed to be a government entity that supports the economy of the entire country. They do not. As you have illustrated numerous times, the beneficiaries of Fed policies for the past 40 years have been the top 1%. Executive wages have grown by leaps and bounds while middle and lower class wages have actually fallen. When the 1% gamble with the entire economy and lose, the lower and middle classes pay the price. The Fed doesn’t work for taxpayers, it works for those who pay no taxes. Why do we continue to believe in this group to successfully navigate our society off of the course it has been on?

Like outsized valuations for TSLA, NVDA, and BTC, the meme stock craze, CB support for pandemic-crippled economies, and yes, even Trumpism, this too shall pass.

The question in my mind is if dumb money will ever be considered too big to fail. Will the fed ride to the rescue in a downturn driven by retail speculators blowing up? If not, why not?

As much as this irks folks, there’s a difference between Wall Street facilitating the “American dream” of homeownership by ensuring that everyone with pulse could buy a mini-mansion they knew they couldn’t afford, and a million people buying shares of a left-for-dead physical video game retailer.

Anybody commenting on this article should watch this clip and then watch it five more times: https://www.youtube.com/watch?v=2f2kGHcdJYU

That’s reality. Right there.

Again: Sorry. Not sorry.

The truth hurts.

I’ve watched the provided clip the requisite 6 times in order to credential my comment. Aside from not getting my 12 minutes back, I’m left with a bitter taste. The tone of your comment, perhaps in shades of your “repulsion economy” piece, also seems designed to elicit anger.

As a counterpoint to your “truth” I’d offer that the top holdings of accounts on a well known and gamified trading platform include: apple, Microsoft, Ford, American Airlines, dismey, and Tesla. While AMC theatres is in the top 10 game stop appears MUCH further down the list.

Options are actively traded in all of those holdings.

Anecdotally I have friends who, to my alarm, have taken to options selling strategies in names such as Peloton, activision/blizzard, and Alcoa.

To confine this phenomenon to GameStop or hertz I think misses the point.

Yeah, great quote from a great movie. If people want their big houses and they fancy cars they need the bankers. \Why do they need the bankers? Because the powers that be decided that bankers should benefit in every scenario of American finance. Why not just distribute 10 million dollar checks to everyone directly? Well then the bankers wouldn’t have control anymore! It would be mass chaos right? Maybe, but I wouldn’t call the current situation exactly a semblance of order. What I see going on in the markets has looked a hell of a lot like chaos for a long time. Managed chaos? If you say so. Managed implies a proactive approach and I haven’t seen anything but reactionary policies my entire life.

No, you need a banker because you don’t have $400,000 to buy a house in cash. Just like you don’t have $40,000 to buy a car in cash.

And you can’t send everyone $10 million checks. That would be $10 million for 330 million people.

We don’t know what the limit is in terms of printing dollars and hyperinflation, and God knows I’m a staunch advocate for redistribution and money-printing, but I can absolutely assure you that sending $10 million to 330 million people would result in total chaos and outright economic collapse within 24 hours.

I agree that before the information age banks were needed. Technologies exist today that can easily eliminate them. While crypto is a 3T dollar sham, the underlying technology of crypto (blockchain), was designed to eliminate the need for banks. An unimpeachable ledger is able to resolve chain of custody without the need for people in the middle to get paid. Could the Fed stand up its own blockchain, pay a ton of IT people to maintain it, and eliminate the bank’s advantage. Absolutely.

I said 10 Million because I have the pen, obviously that would be mass chaos, but you do see my point right? Why do we need banks to control how the government supports the economy? If you want spending to increase, give money to people who spend it. If you want to grow small business, give money to small business applicants. If you want to eliminate homelessness setup housing grants. If you want to improve education then create more easily obtained scholarships. Banks do not need to control the outcomes of ANY of this.

Now this is a good comment.

Incidentally, the provided clip isn’t reality, it’s a movie.

While this may not be reality, it’s certainly closer.

https://m.youtube.com/watch?v=3r76KkcJaTE

Oh it’s a movie? I wasn’t aware. I thought there was a camera in someone’s DB9.

The difference between me and some of you folks is that I’m not so lost in my aversion to an unfair system that I can’t engage with reality.

If I was, virtually nobody would read this site. 75% of readers are here for market commentary. They’re not here to listen to rants about how unfair it all is.

I’m happy to oblige the 25% of you who are here for the philosophical / existential / deep socioeconomic commentary, which is why nearly every, single “Month’s Best” article is dedicated to that kind of analysis.

But most people are here to stay abreast of markets. Maybe one day I’ll split the site into two separate portals.

The overarching point is that some you of guys and gals seem so disillusioned that the only thing you can relate to is cynicism and hatred towards every facet of what you’re begrudgingly compelled to accept as daily life in a hyper-capitalist society.

It ends up manifesting in a steadfast refusal to admit that anyone other than a familiar list of villains is to blame for anything. It’s all Janet Yellen’s fault. It’s all Dick Fuld’s fault. And so on, and so forth.

The world’s a lot more complicated than folks are willing to admit. When you try to congeal everything and assign blame to a handful of people for all of society’s multifarious ills, you end up with autocratic charlatans peddling quick fixes occupying high office. Then you end up with dictatorships.

While I admit to being in the disillusioned camp, I also don’t support Autocratic leadership of any kind. In my opinion if markets were truly democratized there wouldn’t be a ruling class of Billionaires presiding over them. While monetary policy may not be autocratically led it certainly does look closer to an oligarchy. Monetary policy is controlled by former and soon to be big bankers. The revolving door between the two certainly explains why policy seems to benefit them first and everyone else maybe. How about putting an economist social worker in charge of the Fed? I wonder how policy would look then?

All of that said, I appreciate reading both types of content that you create.

Yes I watched the clip three times and now I might have to watch the whole movie again.

In theory, If we eventually become fully automated, with robots doing all the work, then we will literally be at the mercy of those at the top that push the buttons. Humans will be relegated to the status of high-priced cattle.

Right now, presently, we’re only 75% automated and thus only 75% at the mercy of those at the top.

Yuk. Dystopian thoughts. Is that what we’re coming to?

I have no monetary debt. I am not a conventional thinker. The Fed will absolutely start buying equities ( ETF’s) to save Americans (and themselves) from America.

My finger is always poised over the sell button.

Thanks for the movie recommendation.

This is what I learned from February, 2020:

In the future, if the stock market ever goes into a free fall, sell everything quickly.

As soon as the Fed starts whispering (I will be listening) about buying equities, go back in, 100%.

I got the sell side right last time, but waited longer than I should have to get back in.

Otherwise, I will just hold. But it is hard to just sit there snd watch the account balances go down.

Exactly the same take I had. The Fed IS the market now. If they sell, we sell, if they buy, we buy. Now can we call the S&P 500 socialism?

Astute observation. Capitalism has become socialism.

Those at the very top are the ultimate welfare queens. Pampered, privileged, expecting everything to be delivered, and adding no value to anyone.

One way to avoid the difficulty associated with watching prices fall is to ignore the general change and focus on income. At he height of the COVID downdraft last year I was down 8% or so, but more importantly my current income rose and continues to grow today. I don’t buy common stocks anymore because actually they serve no function for me. S&P dividends are less than 2% right now. Even my Vanguard TIPS fund is earning close to 5%. Anyway, everything recovered by June so nothing actually happened.

Brilliant strategy. Yes this is the right approach.

I feel bad for all the retail investors who will eventually get sent to the school of hard knocks to learn the downside of speculative trading/investing. It is bound to happen – it always has. I feel worse for the segment of the population who has been badly affected by the pandemic (maybe even died or been seriously injured for life), and have lost so much financially and emotionally. Kids have been badly affected socially and academically- and are absolutely blameless. Lets hope the Democrats pass some additional help for those affected and those who are otherwise in need. It won’t be enough, but it will help if some of it gets through Congress. If that happens, I guess when Kevin McCarthy becomes Speaker we can survive his BS.

OK, OK. I’ll ‘fess up. I AM RESPONSIBLE for the retail mania.

We always need to blame someone so l will take responsibility on this one.

The comments reinforce the notion that you have to play the cards you were dealt, not the ones that you wish you had been dealt.