Table-pounding pundits and agonizing analysts found themselves in a familiar position on Friday afternoon: Staring down another sizable weekly gain for equities, which continued to confound calls for an imminent pullback.

The lazy thesis behind such calls can be roughly summarized as follows: “Because gravity.”

We use the term gravity in a figurative sense. Multiples are unsustainably high, therefore stocks must succumb eventually. And so on.

The irony is always the same. Gravity, in a more literal sense of the term, is part and parcel of why stocks can’t pull back.

I reiterate this at (maddeningly) regular intervals, but there’s something about the deterministic nature of it that makes it unpalatable for the mainstream financial media, and likely for many analysts too. Of what use are the narratives journalists spin and the textbooks most analysts still consult if outcomes are, to a certain extent anyway, predetermined?

I suppose Friday is as good a time as any for another reminder.

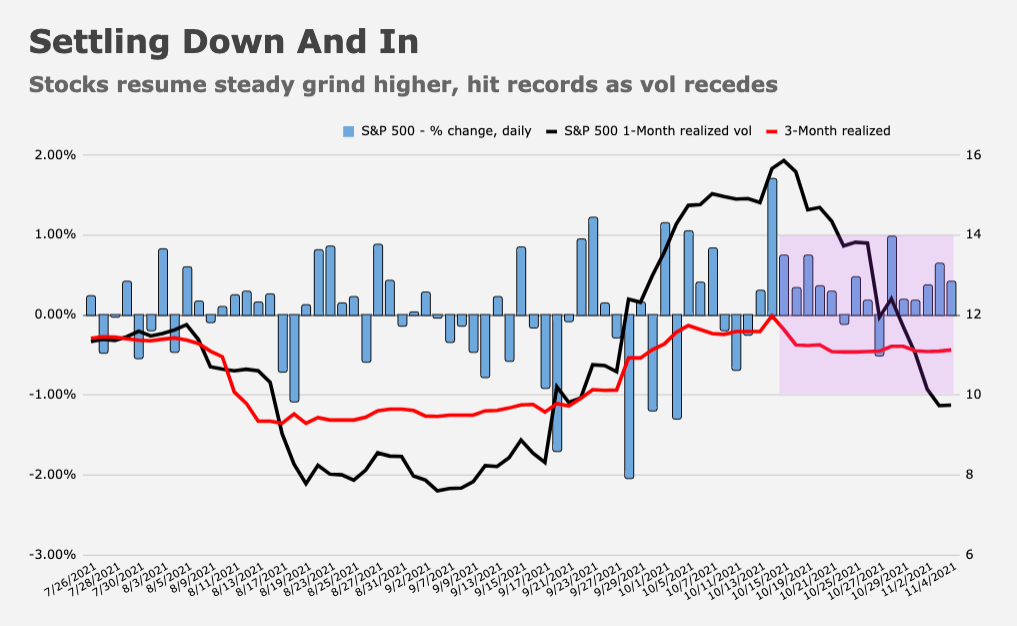

“The SPX / SPY index Vol story for weeks has been one of massive overwriting and options selling, which of course is then stuffing Dealers and the market on stabilizing ‘long Gamma’,” Nomura’s Charlie McElligott wrote, in his latest.

That’s a lot of insulation. And it’s a vol-suppressant. Exposure is dialed up and down, vol-dependent. It’s a self-fulfilling prophecy.

Vol has reset lower, “collapsing under the weight of its own implied daily variance which can’t be met when ‘pinned’ from so much Gamma, in turn spurring massive buying and re-allocat[ing] thereafter from systematic vol target and risk control types,” McElligott went on to say.

He estimated the likely vol control re-allocation over the past month at almost $58 billion in US equity futures.

CTAs, meanwhile, likely added somewhere close to $50 billion of exposure across global equities over the same period, as signals flipped back to “long.”

It helps that central banks worked this week to dial back the market’s aggressive rate hike pricing. Real yields were back near the lows in the US. There’s nowhere to go but stocks. And people know it. Global equities took in another $26 billion over the latest weekly reporting period.

Remember how, a few weeks back, there was chatter about inflows “rolling over” after a single, large weekly outflow? Well, consider that “LOLed,” for lack of a more poignant way to put it.

The four-week average is now back above $22 billion, and the YTD haul is approaching $870 billion (figure above).

There’s some interesting nuance. US equities are seeing a bit of “spot up, VIX up,” a dynamic that’s amenable to ominous headlines.

It can be ominous, but what’s important is what’s driving it. McElligott on Friday pointed to buying and selling of calls and puts in Tesla on Wednesday. Specifically, he detailed the knock-on effect of 185k January 2024 options.

“Those trades bot an ENORMOUS amount of long-dated two-year Vega, so the iVol on TSLA Jan2024 1400 line went from 50% to 61% by late Thursday, while TLSA 60-day ATM iVol went from ~50% to 70% in the past week,” he wrote, adding that “because of the magnitude of this move and the impact that TSLA and other mega-cap ‘weaponized Gamma’ names are having on Index per their explosion higher in market cap, we’ve seen broad Nasdaq Index / QQQ iVol reset higher across the entirety of the surface [and] it also impacted SPX iVol because of the significance of mega-cap growth” in the index.

One could editorialize around that all day (it speaks to pretty much every modern market dynamic discussed in these pages dating back a half-decade), but there are two simple takeaways. The first is just that right-tail events can push up implied too.

The second is that the tail is wagging the dog even harder than ever. As Charlie put it, “the insidious impact of the ‘weaponized Gamma’ dynamics is again showing us what a dysfunctional mess market structure has become [as] spot Equities are left as a derivative of the Options market and its flows.”

You must be logged in to post a comment.