On so many levels, the ongoing surge in equities (and particularly US equities) seems patently absurd.

Even as melt-ups go, the S&P’s ascent to new peaks felt dubious, propelled as it was in part by another options frenzy and readily apparent signs of speculative froth.

“Markets over the past week are evidencing a scramble for upside (created by single-name Growth stocks like TSLA), as the persistent ‘wall of worry’ of the past year and a half is again being hurdled and leading us to fresh index all-time highs,” Nomura’s Charlie McElligott wrote Tuesday, adding that “it seems ‘peak FOMO’ is permeating speculative assets.”

Read more: Speculative Assets In ‘Peak FOMO,’ McElligott Says

As is always the case during melt-ups (a nebulous term in its own right, even as it somehow seems less ambiguous when compared to the new vernacular, replete as it is with acronyms and pop culture jargon), the list of superlatives is virtually endless.

“Over the past 12 months, the S&P 500 printed new all-time highs 75 times,” Goldman’s Christian Mueller-Glissmann wrote.

That’s the second most in nearly a hundred years. If you’re wondering what it looks like on a chart, you’re in luck (figure below, from Goldman).

The current pace was only surpassed once in history — in the mid-90s.

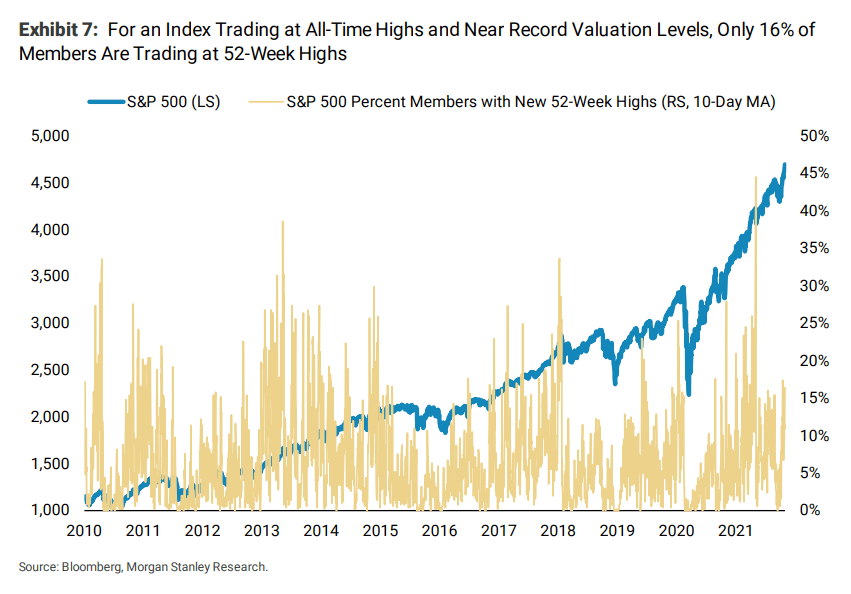

Even a quick glance under the hood suggests the latest leg up rests on a shaky foundation. “Despite the fact that the S&P continues to make all-time highs and is trading near record valuation levels, only 16% of members are at 52-week highs,” Morgan Stanley’s Mike Wilson remarked earlier this week.

That’s nowhere near levels seen earlier in 2021. For example, the figure was 45% in May (figure below).

As Wilson went on to say — and this is tautological — that’s “further evidence that the recent rally is quite narrow in terms of breadth and that there continues to be high dispersion under the surface.”

All of that said, is it really so absurd when you step back and take stock (no pun intended) of the balance of news? Perhaps not.

In the same note briefly cited above, Goldman’s Mueller-Glissmann recapped recent events. “Macro surprises have turned positive in DM countries, a balanced FOMC taper announcement and a dovish BoE helped dispel some concerns of hawkish policy surprises [and] positive news about the efficacy of PFE’s and MRK’s antiviral drugs also contributed to the risk-on sentiment,” he said, adding that earnings season in the US was “exceptional.”

Recall that not only did corporate profits grow far more than expected (figure above), the outperformance to consensus was driven by margin beats, a huge relief for investors at a time when profitability is being squeezed on all sides.

The above is a bit perfunctory, but it’s worth at least considering the fact that there are fundamental reasons for stocks to be higher. If robust earnings and game-changing COVID pills don’t do it for you, then just have a look at real yields.

As Goldman put it, “elevated valuations might become a speed limit for returns over the long-term [but] in the near-term, low and anchored real rates and volatility coupled with the pressure for higher equity allocations help explain” elevated valuations.

I had almost forgotten about fundamentals! LOL