If you needed yet another piece of incremental evidence to support any iteration of the “peak growth” narrative you may be harboring, one bank’s quadrant work showed the economy transitioned to a “slowdown” phase on October 15.

In the US, growth concerns are proliferating due in part to what now seems like intractable Democratic infighting.

The divide between moderates and Progressives around the proper scope for Joe Biden’s fiscal agenda undermined consumer psychology in October, the University of Michigan’s sentiment survey suggested (figure below).

Between ambiguity around the future of the White House’s stimulus plan, a severe slowdown in China and, now, the threat of imminent tightening from central bankers who perversely risk hurting consumers by choking off growth while trying to protect them from surging prices, economic angst is increasing.

In a Tuesday note, Nomura’s Charlie McElligott flagged what he described as “a critical phase shift occurring in real-time.”

“By the end of last week, we moved into the ‘Slowdown’ phase for the first time since June 2018, and out of the legacy ‘Expansion’ phase entered into on March 18,” he wrote, referring to the bank’s quadrant framework.

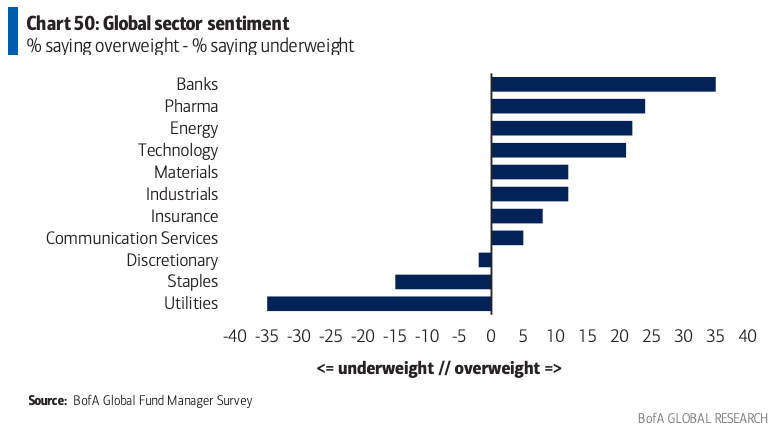

Also Tuesday, the October vintage of BofA’s Global Fund Manager survey showed expectations for global growth, profits and margins all declined, with the growth outlook turning negative for the first time in 18 months.

What does the “phase shift” in Nomura’s model entail going forward?

Well, that’s hard to say. McElligott’s penchant for granularity was on full display via backtests of various equities factors for one- and three-month forward returns during a transition from “expansion” to “slowdown.”

He called the results “nuanced” and somewhat counterintuitive. “You actually see ‘Value’ (both Cyclical and Defensive Value) work relative to ‘Growth’ and other duration-proxy factors,” he remarked.

BofA’s October survey suggested “investors pour[ed] into cyclicals on inflation concerns,” the bank’s Michael Hartnett said, noting that FMS investors are “rotating out of utilities, staples, and discretionary and into banks, pharma, and energy stocks.”

“Investors got more positive on interest rate hike sensitive banks and less optimistic on tech [which is] now a slight UW versus history and still believed to be overvalued,” Hartnett continued.

The big-picture takeaway is just that Tuesday offered additional quantitative and qualitative evidence to corroborate the notion that economic momentum is on the wane.

Nomura’s econ team has a weekly GDP tracker which Charlie noted also “show[s] a significant deceleration in growth from the ‘sugar highs.'”

He added an important caveat. “Within the backtest time horizon to 2000, we have never seen a supply chain-induced inflation spasm quite like this.”

When you consider the unique macro circumstances with the counterintuitive equities forward performance backtests, you’re left to ponder the potential for “more factor whipsaw volatility in coming months,” McElligott wrote. “Stay tuned.”

You must be logged in to post a comment.