“We have an energy crisis, supply chain issues, higher inflation, signs of weaker growth and lots of talk about stagflation,” Deutsche Bank’s Jim Reid said Monday.

Suddenly, stocks are having trouble climbing the proverbial “wall of worry.” It was just a few weeks ago when market participants were derisively lamenting equities’ apparent obliviousness to a growing list of macro headwinds.

“Historically, market participants might call an ascent in the face of headwinds ‘climbing a wall of worry’ [but] this is not the case here,” JonesTrading’s Mike O’Rourke said, on September 12. “For it to be such a climber, the market would need to have at least mildly reacted to the negatives to acknowledge they exist,” he added. “This has been a worry-free wall.”

Not so much anymore, though. At the least, tech stocks have “acknowledged” that rising bond yields pose a threat. The Nasdaq 100 was on track for its third decline of 2% or more in the space of a month (figure below), for example.

Amazon turned negative for 2021 amid the selloff.

Some of Monday’s weakness was attributed to Nancy Pelosi’s forced decision to push back the deadline for passing the bipartisan infrastructure bill. Although a compromise between Progressives and moderate Democrats still seemed highly likely, last week’s party infighting was further evidence that America is becoming ungovernable.

On Monday, Joe Biden and Mitch McConnell blamed each other for the debt ceiling standoff.

“Republicans’ position is simple. We have no list of demands,” McConnell told Biden. “For two and a half months, we have simply warned that since your party wishes to govern alone, it must handle the debt limit alone as well.”

That is precisely the dynamic I bemoaned in “Maybe America Wasn’t Such A Good Idea After All.” Republicans aren’t attempting to extract concessions in the debt ceiling standoff. They’re just refusing to engage out of sheer spite.

Incredibly, Biden refused to rule out a technical US default. “That’s up to Mitch McConnell,” Biden said. “I can’t believe that that will be the end result because the consequence is so dire,” he added. “But can I guarantee it? If I could, I would.”

Not to put too fine a point on it, but that’s the wrong answer. (As Ernie Hudson’s Winston Zeddemore told Dan Aykroyd’s Ray Stantz, “Ray, when someone asks you if you’re a god, you say ‘Yes!'”)

Under no circumstances should the President of the United States suggest, even for a second, that he (or, one day, she) might allow the country to default.

Biden made things worse. Accidentally. “A meteor is headed to crash into our economy,” he declared.

This is, frankly, too stupid to believe. We’ve been here before, yes. But this time, it feels even stupider than usual. Both sides are right and wrong simultaneously. Democrats could end this charade if they wanted to, but so could Republicans. That neither is willing to do so is yet another testament to the notion that the only thing voters can be certain of when it comes to Congress is that with few exceptions, lawmakers would sooner drive the country off a cliff than make concessions.

It’s at least worth mentioning that there are actions the Fed could take (alongside Treasury) to avert a total catastrophe in the event of a default. Specifically, there are nine possible actions divided into three categories. TD’s US rates team summarized them as follows:

Category 1: Policies that fall within the existing authorization of the desk

Action 1: Outright purchases: This would happen if the Fed determined that there was a need to increase its support of market functioning by removing securities with delayed payments from the market.

Action 2: Securities lending: Acceptance of securities with delayed coupon payments as collateral in securities lending activity.

Action 3: Rollovers of maturing securities: While this was not a big issue in 2011 or 2013, this is a larger issue now given the Fed’s sharply higher Treasury holdings. There are about $90bn of Treasury coupon securities maturing from October 18-November 15 on the Fed’s balance sheet and about $74bn of bills maturing as well.

Action 4: Repos to keep the Fed funds rate in its target range: Injection of reserves in case effective federal funds rate (EFFR) went above 25bp, with delayed payment Treasuries eligible as collateral.

Action 5: Discount window lending: Discount window lending against delayed payment or impaired Treasuries. These actions essentially clarify that Fed operations would treat defaulted Treasuries in the same manner as non-defaulted ones, but with defaulted securities valued at current market prices.

Category 2: Addressing strains on money markets

Action 6: RRPs to Address Negative Treasury Bill and Repo Rates: Conducting RRPs under which the Fed would provide unblemished Treasury collateral to the market. Note that the overnight RRP facility is already in place and could fulfill this role today. However, only approved counterparties can transact in the RRP facility.

Action 7: RPs to Address Pressures in the Treasury Repo Market: Conducting repo operations if repo rates rose substantially even if EFFR was relatively unaffected. Note that the FIMA Repo and Standing Repo Facilities already exist and could fulfill this role today. However, one needs to be an approved counterparty to transact and there are limits in place which may have to be modified ($500bn for SRF, for example).

Category 3: Outright purchases or coupon swaps

Action 8: Purchase Operations to Remove Defaulted Treasury Securities from the Market: This would require the Fed to run operations to purchase particular CUSIPs. Note that this would increase the Fed’s balance sheet, which would currently contradict the messaging on tapering.

Action 9: Outright CUSIP Swaps to Remove Defaulted Treasury Securities from the Market: This would be balance sheet neutral and may be easier today given the tapering message. However, the NY Fed would likely be selling securities with longer average maturities than those of the securities it would be purchasing.

“There was unanimous support in 2013 for Category 1 actions and many wanted to provide the Chair with discretion on Category 2 actions,” TD’s Priya Misra wrote, adding that “there was more debate on Category 3 and then Governor Powell referred to them as ‘loathsome’ [although] in the ensuing discussion, Powell admitted that there may be a case for Category 3 items in a ‘catastrophe’ scenario.”

Yes, in a “catastrophe scenario.” Like the one Biden not-so-delicately posited on Monday.

I hesitated (again) to dedicate space to this because I’d like to think Congress isn’t so totally lost in the fog of partisan war that they’d chance a default. If nothing else, the list of Fed measures (above) is worth enumerating for posterity because absent legislation that does away with this farce once and for all, this will come up again.

Market angst was exacerbated to start the week by OPEC+’s decision not to increase production beyond next month’s scheduled hike. That pushed crude prices to the highest since 2014, thereby stoking more inflation concerns and raising the odds of a full-on energy crisis. 10-year breakevens hit a seven-week high.

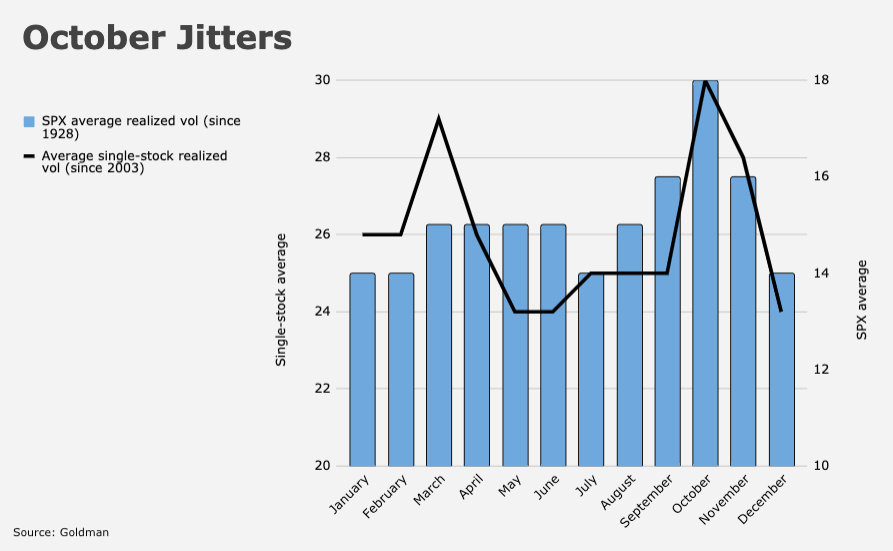

Those hoping the stars will align for an equities rebound coming off September’s selloff should note that there is a celestial map, if you will. But October tends to be more volatile (figure below).

I spoke over the weekend about a “macro mess” and the potential for an accident (or an “event,” as BofA’s Michael Hartnett put it). Monday certainly felt messy.

In a separate note, BofA noted that September didn’t just mark the worst month for the S&P since the COVID scare, it was also a month during which “all major asset classes fell except cash.”

Like many of her peers, the bank’s Savita Subramanian was effectively forced to raise her year-end forecast for the S&P last month. It felt like a begrudging mark-to-market exercise. Fast forward four weeks and the index sat at ~4,300, a mere 50 points above Subramanian’s new target.

Trump couldn’t rule out nuking Germany. Times have changed. Politicians believe confidence in the US is unshakable and needs no nurturing. So far they are right. They will keep pushing the limits until something breaks. This is probably not the event though.

Biden must stop making off-the-cuff remarks that are blurted out with little thought. He’s the freaking President of the United States, not D***** T****. He’s hurting himself and his cause.

And the democratic party, generally, needs to get real and put aside any grace for McConnell and all the self-immolating warlocks and witches that remain to inhabit the vestiges of the republican party. With each day, in the hope of redemption, their actions and words hurt themselves. (The Orange one will return! He comes forth as we speak!)

And democrats must learn how to call a spade a spade, and call out and name the destructive actions of their twisted republican “friends.”

As for the matter at hand, I’ve heard scuttlebutt that Treasury, under the constitution, has the ability to mint a coin in any denomination to solve the problem. Is that not actually an option?

Time for Janet to mint the $5 trillion coin and tell Mitch and his followers to go ____ yourselves.

Actually she has about 2 weeks before she has to do it….

H-Man, this whole environment looks more like a cell block riot while we wait for the survivors to emerge.

The market feels like yet another monster movie where we think the villain is mortally wounded and yet it coils and strikes one more time. Maybe overly dramatic but then, who hasn’t suspended belief that this high wire act w/ no net is the new normal?

I keep hoping Biden will understand that he is a war time president and start acting like it.

Don’t kid yourself. For all of the Congressional moaning about the debt ceiling, they like the drama. It’s one of the only times individual lawmakers can get press time for a couple of weeks. ‘Look at me, your hardworking rep fighting for you against your foes’.

If Congress as a group didn’t really need the platform to beat their chests, they would have ended the idiocy of the debt ceiling long ago. The rest of the world can’t believe we have such a ridiculous thing – deciding if we’ll pay for what we’ve already bought. Congress will only show they can solve real problems when they get rid of the debt ceiling nonsense once and for all. Until then they are just incompetent slackers (not to put too fine a point on it).

You make some very good points.

Thinking about this circus of clowns a bit more, this really has everything to do with rigging the 2022 vote. The Neo-Confederate Nazi Party (fka the GOP) has jammed illegal voter suppression legislation down the throats of American voters in 19 states (I believe that is the count). In the next few weeks, the district lines for 2022 will be released. Moscow Mitch is riding out that clock with the Debt Ceiling as a way to delay the vote on the various voting rights bills. Without the voting right protections in place the legal framework to challenge the gerrymandered districts it will have the effect of making it much harder to challenge the districts in court. Mitch believes there will not be enough time to challenges the districts in time for the 2022 election.

That means in approx 2 weeks we can expect 10-12 “middle of the road” Rs to get flexible and support suspending/moving the debt ceiling. Of course, Mitch will be pulling the strings behind the scenes. It will end up being a non-event.

Given the clause in the Constitution that says, basically, that US shall not be questioned, I don’t see how Congress even has the power to mess with the debt limit.

I found this statement in an abstract of Duke U. Law Journal:

“under a departmentalist understanding of executive power, a conclusion of this nature would be the basis for the president to ignore the debt limit when congressional actions create unconstitutional doubt about the validity of the public debt.”

https://dlj.law.duke.edu/article/the-debt-limit-and-the-constitution-how-the-fourteenth-amendment-forbids-fiscal-obstructionism/

If McConnell thinks that Democrats should govern alone, then I guess they will have to. Bye-bye filibuster. Hello 5 new supreme Court justices.