At some point, it had to happen.

After months spent watching paint dry, investors were treated to some September fireworks as US equities finally snapped out of an eerie summer lull.

One of the defining features of stocks’ slow grind higher into last month’s selloff was an uncomfortable juxtaposition between extremes on various crash metrics and rock-bottom realized vol. Eventually, that required “a ‘true-up’ reconciliation,” as Nomura’s Charlie McElligott put it Friday.

It was, of course, no coincidence that the movement started in and around-OpEx, when markets lost the vaunted gamma “pin.” The notion that there’s a “window for movement” and/or that the distribution of outcomes is likely to be wider post-expiry, has been so well socialized that some appear to be front-running it.

Whatever the case, the “vol expansion” window, as McElligott calls it, opened and spot did indeed start to move (figure below). A hodgepodge of macro catalysts, including the Evergrande drama, the September Fed meeting and various manifestations of DC dysfunction, sufficed to “explain” the action (because we always need a narrative).

As McElligott wrote Friday, recapping weeks of notes that preceded September’s swoon, we were bound to “see an opportunity to release from the ‘long Gamma’ chokehold created from options overwriting and strangle-selling, and pivot to actual price discovery and larger trading ranges thereafter, which would then see realized vol ‘true up’ to ‘stressed’ implied vols.”

That “truing up” process triggered a mechanical de-allocation from the vol control universe, where positioning was extremely loaded. The latent down-trade then collided with other accelerant flows, including dealer hedging.

“Let’s look at just the past three sessions, where we see the now obvious dealer extreme ‘short Gamma’ hedging flows into EU and US cash closes as spot keeps suffering under de-allocation / net-down / gross-down pressure, which has been [exacerbated] by the Equities market seeing another classic late-day ‘rug pull’ in the form of the lost corporate buyback bid’ in the final 20 minutes of the day,” McElligott went on to say.

Obviously, the global bond selloff didn’t help matters, especially to the extent it undermined secular growth favorites in mega-cap tech to the detriment of the “broad” (a misnomer) market.

The good news is, it was a cathartic release of sorts.

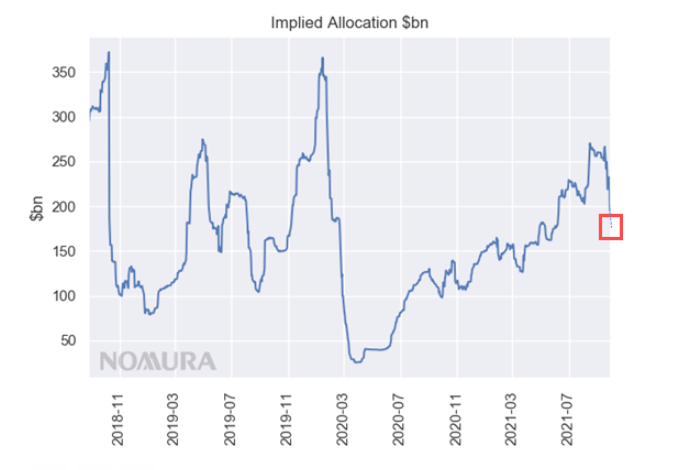

“The only thing that cleanses ‘crash-y’ vol markets and thus arrests spot Equities from moving lower is an actual drawdown in spot, which then resets these self-fulfilling extremes implied by stressed metrics,” Charlie said, before quantifying the scope of vol control de-leveraging. Over the past two weeks, the move up in realized vol (figure above) triggered a $73 billion de-allocation on Nomura’s estimates (figure below).

Speaking to the notion that this was a good thing, Nomura’s model shows vol control’s overall allocation to equities is now in just the 56th%ile, all the way down from the 90th%ile. McElligott also noted that other banks’ prime data suggests Long/Short funds purged their net exposure. The upshot: Positioning is cleaner.

That doesn’t mean nothing (else) bad can happen. It just means various extremes are now less extreme, and things feel less ominous. At least at the margins.

What happens next? Well, it all depends on whether spot can settle. And no, that’s not a trivial observation. If stocks can settle back into a benign range, the cycle can start over.

“The big picture good news is that once Vol squeezes and stocks sell off, it takes sustained selling and persistent big swings to keep Vols supported higher,” Charlie remarked on Friday, before detailing what happens if the market can’t keep printing daily changes in excess of, say, 1.5%:

When Vols reset lower, there are all sorts of virtuous cycle benefits. It accelerates client hedge monetization of downside (creates Delta to BUY), while dictating a mechanical “Vanna” support from Dealer hedge flows / create Delta to BUY as customer Puts go OTM and implied Vols soften (Vanna is your second-order Greek which measures the sensitivity of the Dealer’s Delta to changes in implied Volatility)…all of which can allow for spot Equities to ratchet higher in positive feedback loop

And very rationally, when notionals and VaR come down on the buyside (de-grossing / de-netting), clients will simply need LESS downside crash / tail…and this can further see Vols reset lower.

That said, we’re not out of the woods. Certainly not on the domestic political front and likely not on the macro front, either. Indeed, we’re still not entirely clear of the mechanical flows risk, something McElligott made abundantly clear.

Ultimately, though, Charlie’s 30,000-foot assessment as of Friday afternoon was that the market is “in the late stages of the selloff / de-risking.” He sees “incremental pressure on Vols in coming days if we can clear the accelerant flow risks from Dealer ‘short Gamma’ and CTA deleveraging triggers still being in play.”

All of this comes with the caveat that US lawmakers could always spoil the party by stumbling into a crisis. But when is that ever not a risk?

Sigh, those pesky lawmakers. How could they spoil Christmas? Let us discount the ways.

Infrastructure (physical) bill. I think investors’ expectations are low. If there is no bill, some subsectors would get hit, but we’re probably talking a mid-single digit pct of SP500.

Infrastructure (social) bill. Do investors care about this? It has already shrunk from $3.5TR to $1.5TR – maybe The Squad doesn’t accept that, but Manchin and his ilk hold the cards. A third of the loaf, or no loaf? I’m not sure investors, in the aggregate, care all that much.

Tax increases. These have been whittled down to 25% corporate, 39% top marginal individual, some modest increase in cap gains, and I’m not sure what else. Investors won’t mind if that erodes further.

Debt ceiling increase. Ok, this is a “have to have”. And a buying oppty if things look shaky.

Fed Chair. Investors probably want Powell back, simply because uncertainty = bad. Warren’s attacks are probably a gift to his chances.

Hardline Policy vs China (Biden). Everyone already sees the next Cold War emerging. Short of active shooting, how to be unfavorably surprised? China can certainly roil the markets further, but not clear it needs US help to do so.

Drug pricing. Sector specific risk, and that sector has already been performing blah-ish. Healthcare P/Es, for those with E, don’t discount much growth. The group without E is quite a laggard as well.

Crypto regulation. Something that will greatly upset a rather small percent of investors.

What am I missing?

Don’t seem to be missing much. I, for one, would love to see the tax increase proposals slip some more and the whole shebang be put off until the new year when the election cycle will put more pressure on making the whole mess disappear. Meanwhile, I’ll get my booster and my flu shot and venture out in the actual world a bit more.

Jyl, thanks for your comment! Perhaps the biggest risk right now is coming from inflationary pressures that could force the fed to raise rates unexpectedly and sharply:

– climate change is pushing the cost of food up

– re-openning activity, supply chain disruptions are pushing the price of commodities up

– pandemic fear, overall healthy family finances is pushing the price of labor up

– past bankruptcy of shale oil producers, low water levels at hydroelectric plants are pushing energy prices up

– most central banks printed money during the pandemic, and all that cash is going everywhere except savings accounts, pushing the price of everything up

The pressures may all be temporary, but central banks around the world are being tested in their resolve to stomach inflation overshoots.

If I were the fed, I would not alarm anyone until it’s time to stop the music. In the background I would prepare a team to pick up the pieces. Tapering will cause rate increases. The fact the central bank is telling people otherwise implies they’re leaning too much on social psychology (they’re bluffing).

IMO the biggest risk is central banks over reacting to non-inflationary price increases. The central banks have near zero impact on current price increases. The global over reaction of monetary policy could (maybe is) set(ting) us up for a deflationary death spiral in 2-5 years.

What is actually needed is global coordination to resolve the supply chain disfunction. Free market capitalism has failed to meet the moment and the collective of global supply chain players are doing very little to mitigate the issues.

The global supply chain crisis is being treated like an unavoidable and pre-ordained economic inconvenience. It is far worse and should be addressed as the crisis it is before the roots of the next global war are grown as happened in 1920-30’s.

I hope, and will continue investing as if, what you’re saying is true. Thanks for the perspective!

Thanks to H I’ve started reading more about MMT. At the very least, it’s time for serious discussions by those in charge as to its workability. It never ceases to amaze how a world trying to embrace change can imbed outdated concepts without a thought. Unfortunately, the chances of serious discussions about central banking happening in the current environment are close to nil. I would add to that the question of how much climate change has (and will) put downward pressure on financial conditions is barely being considered.

Longer term I see markets stagnating at best. Global negative headwinds are great and global governing systems are not up to the task. Humans, as a species, have finally outrun our ability to adapt to change. We’re lost in the wilderness and are out of matches.