It was just — let me check the watch I’m not wearing — 24 hours ago when financial media outlets were busy claiming that retail dip buyers and other reliable sources of reflexive, instinctual equity demand, had gone missing.

Fast forward from Tuesday’s selloff to Wednesday’s fledgling rebound and Bloomberg declared that “the crowd of dip buyers returned… amid speculation that the biggest selloff since May had gone too far.” The same linked article cited an analyst who said “dip buyers are out in force boosting stocks.”

I’ll just put this out there: Journalists and analysts with no access to actual trades make this up as they go along. It’s pure fiction. If it’s accurate, it’s only by accident. “Any similarity to actual persons, living or dead, or actual events, is purely coincidental,” as the standard TV and film disclaimer goes.

You really need to be connected to real prices, or know someone who is, if you’re going to make claims about what is and isn’t driving the price action.

Cue Nomura’s Charlie McElligott (someone who is connected to such things), who on Wednesday delivered a characteristically granular postmortem on Tuesday’s rates-inspired rout. The main points will be familiar to anyone who’s been a reader since… well, since at least yesterday.

“With QQQ (Nasdaq) options as the ‘delta-one’ extension of the move in Rates / Duration, QQQ Gamma per 1% move was ~-$1.0B (0.4%ile) and peak ‘short Gamma’ at $365, while Net Delta was ~-$30B (0.2%ile) end of day from prior -$8.7B,” he wrote.

The visuals (above) show “monster flows,” as Charlie put it.

As you can imagine, the spike in realized vol is playing havoc to the extent it’s likely prompting de-leveraging from the vol control universe. The shaded area (in the simple figure below) gives you a sense of things.

“With rVol spasming, the Vol Control / Target Risk space was again sent reeling,” McElligott said.

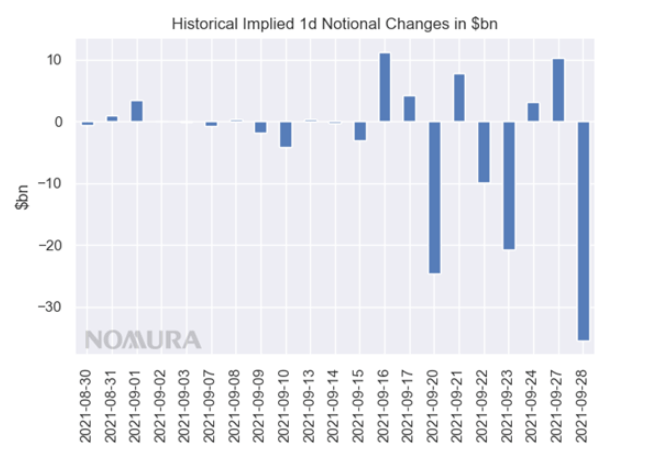

The bank estimated “a rollicking” (his word) $35.4 billion de-allocation Tuesday, a 0.8%ile one-day change (figure below).

That’s what happens when months of accumulation due to suppressed realized vol collides with a sudden drawdown. If you can’t extrapolate from the visual, the estimated sale from the vol control universe over the past week on Nomura’s model is more than $52 billion.

Recall the chart (below). Midway through August, swings (a misnomer in this context) on the S&P were averaging just 0.5%. That pushed down realized vol, dictating ongoing exposure adds, ultimately setting the stage for a large de-allocation on any big move in spot — a move like the one seen on Tuesday.

One more time: Stability breeds instability. In a kind of metaphysical sense, yes, but also mechanically thanks to modern market structure.

Also on Tuesday, leveraged ETF rebalancing likely translated into more than $7 billion in selling. Those types of amplifier flows are another argument for banning the products. (That’s my ad hoc editorializing, by the way — Charlie didn’t say anything of the sort.)

The saving grace is that spot is well above CTA trigger levels for both the S&P and the Nasdaq 100, according to Nomura. So, at least that accelerant flow isn’t in play. Yet.

You must be logged in to post a comment.