Somebody bought the dip.

Global equity funds took in more than $51 billion over the last week, a period which coincided with what counts as a “selloff” these days in US stocks.

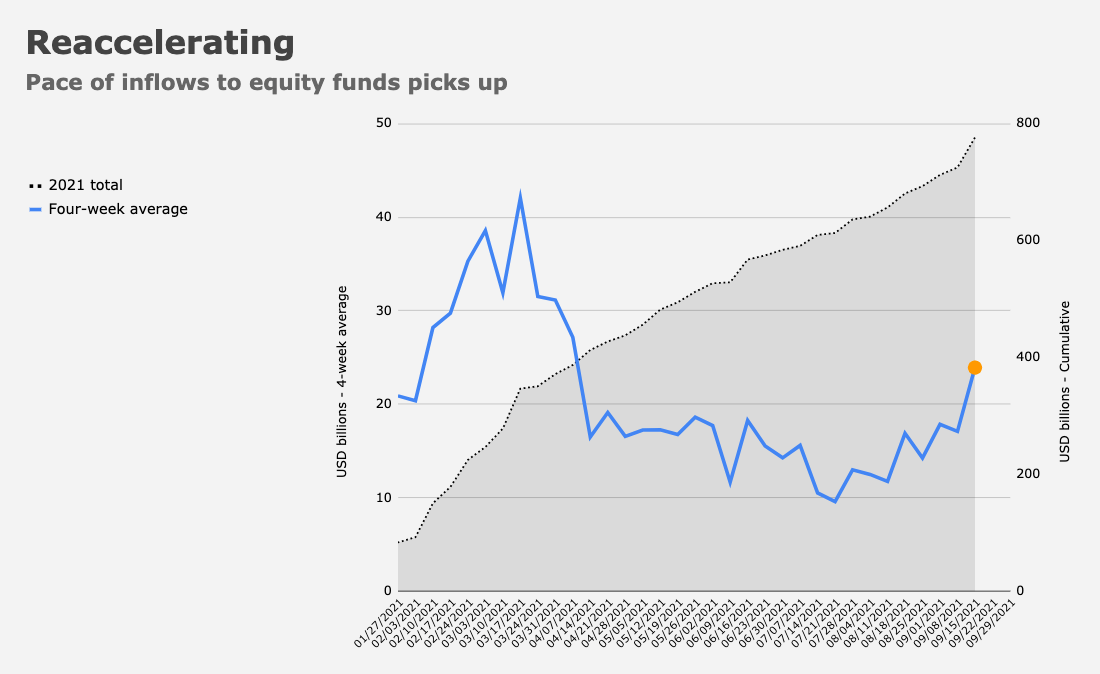

It was the largest weekly inflow since March (figure below). The YTD haul is now $776 billion.

It was a “monster reallocation from cash to stocks,” BofA’s Michael Hartnett said, citing the receding threat of tax redistribution and expectations that the Fed will “remain Wall Street friendly.”

Democratic infighting and a watered-down tax proposal suggest the White House is unlikely to get everything it wants from a Congress that’s divided not just along party lines, but also within the two parties.

Joe Biden on Thursday appealed to lawmakers and, more importantly, to the public. I suggested his remarks likely fell on deaf, apathetic ears.

In any event, the pace of equity inflows, which had been decelerating, is now back above $20 billion per week (figure below).

Inflows are annualizing more than $1 trillion.

The breakdown showed US equity funds took in almost $46 billion, the most in six months. US large cap funds took in the most ever, at $28.3 billion.

ICI’s data showed total money market fund assets fell by nearly $40 billion over the same period (figure below).

It was the largest outflow of 2021.

I suppose I could conjure a list of more nuanced explanations if I were so inclined, but for our purposes here, I’m not — inclined, I mean.

There’s $4.5 trillion sitting mostly idle in money market funds. For a dozen years, it’s paid (handsomely) to reengage on drawdowns. Over a decade, that muscle memory evolved. The “BTD” impulse has optimized around itself. Every nascent pullback from record highs is seen as an opportunity. And every instance of benchmarks hitting new records within days of a shallow dip is “proof” of the strategy’s viability.

And so it was that a derisive meme about retail bagholders metamorphosed into an infallible, self-fulfilling prophecy.

With a little help from the benefactors with the printing presses, of course.

Personally I have been a seller the last week or so. Until this Tapering question is answered I am being a lot more cautious.

H-Man, speaking of those benefactors, on some strange whim, I meandered over to some Fed site that shows the monthly buying of treasuries. I was trying to figure out what they were buying —– the short stuff, the belly or long bonds. The numbers were numbing. Which leads me to wonder, who will replace those benefactors when they hit the road?

Well, I guess they won’t be hitting the road anytime soon.

If there is one thing I’ve learned lurking around these pages in the past couple of years it’s that these very benefactors are not going to let markets go on cold turkey, liquidity-wise.

Considering that even “thinking about thinking about tapering” can cause a minor sell-off there is exactly zero chance for them “hitting the road”, if that means anything resemblang a return to the status quo pre-Covid. Not to mention any return to the status quo pre-GFC. The most one could reasonably expect is some gradual (read: glacial) reduction of additional monthly purchases in the hope of one far day being able to raise interest rates by a whopping 0.25 percent.