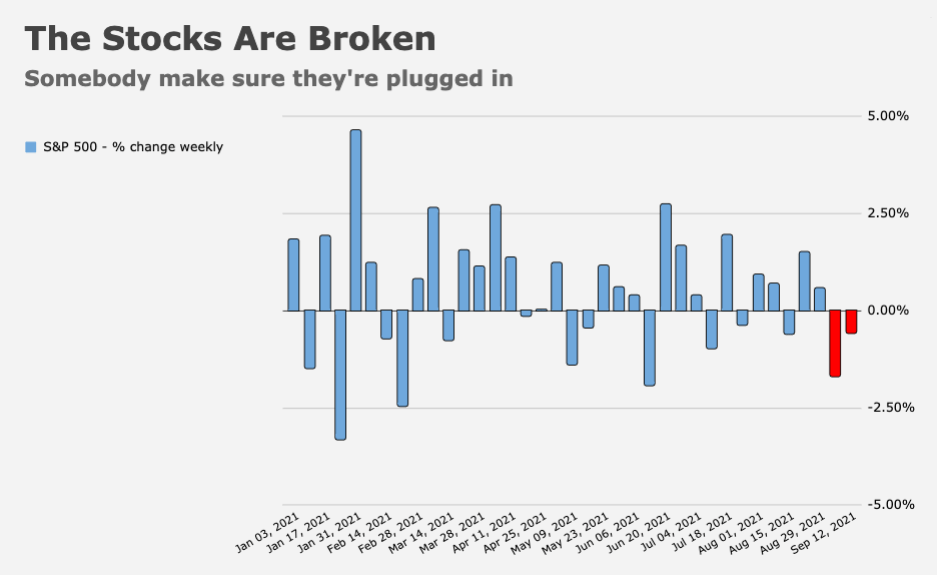

Thanks to the worst session for the S&P in a month, US equities logged a second consecutive weekly decline.

It was the first back-to-back weekly loss for the world’s risk asset proxy par excellence since May.

What you see in the simple figure (below) is illegal in 14 states. That’s a joke. I’m not sure if it’s funny or not. By Friday evening, I’m never sure of very much.

Big-cap US tech suffered its worst day in months. Small-caps managed to eke out a minuscule gain on the week.

Sentiment is deteriorating. Among market participants, yes. But especially among consumers. The preliminary read on the University of Michigan’s gauge showed no improvement from August, when the headline index plunge to a decade low. The sour read on consumer perceptions made for a rather stark juxtaposition with robust retail sales data.

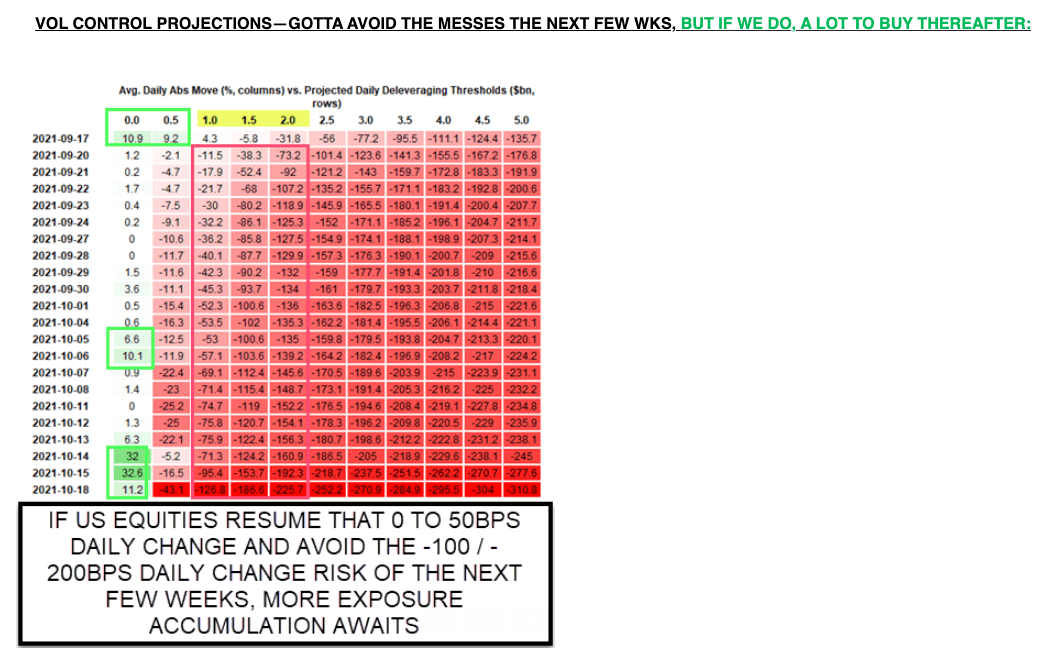

Next week is key, Nomura’s Charlie McElligott reiterated, in a Friday afternoon note. “Dealers have been relentlessly stuffed with short-dated options gamma from overwriters and strangle-seller flows, which meant more ‘pinning’ as dealers have to dynamically hedge… which acts as the insulation keep[ing] markets in [a] chokehold,” he said, adding that dealers have now “lost a lot of the ‘long gamma’ they were sitting on.”

That leaves the market free to move, so to speak. The door is open to a wider distribution of outcomes coming out of options expiration, and it would open wider still in the event spot managed to move below 4,390, where dealer gamma would flip short, according to Nomura (figure below).

The vol control universe has the potential to be a key player going forward. This is a point McElligott’s reiterated time and again of late.

Thanks to what feels like an eternity of small daily moves and compressed realized vol (figure below), vol control strats built up their exposure to the tune of $135 billion over the past six months on Nomura’s model.

Very low realized vol suggests heightened sensitivity, making even a modest down day potentially perilous considering loaded positioning.

“If the ‘vol expansion window’ were to see any follow through next week with the significant ‘gamma unclench’ and ‘delta de-risk,’ then even a -1.5% day say, mid-week, could generate a shock de-allocation thereafter of -$80 billion to -$90 billion, due to this low absolute rVol dynamic in conjunction with the ‘impulse’ positioning build of recent months,” McElligott said Friday.

The good news is (and this is communicated in Charlie’s annotations on the table, below), if equities can make it past the initial “unclench” and attendant window for movement, the market could find itself right back in the virtuous cycle.

The avoidance of any “accidents” that might trigger systematic deleveraging would again tempt vol-sellers, thereby reestablishing the “pin” and insulating spot from large daily swings.

That, in turn, would set the stage for vol control to add exposure, “at first slowly… but then hypothetically exploding higher in standard lagging fashion, as trailing realized volatility averages lower again,” Charlie went on to write.

The key, then, is making it through the next several sessions without some manner of mishap the starts tipping dominoes.

Thankfully, there are no major events scheduled next week. That’s another joke. But, again, it’s Friday evening. And by the end of the week, I’m never sure what’s funny and what isn’t.

You must be logged in to post a comment.