On Thursday afternoon, while wailing Afghans and shell-shocked military personnel were bagging up bodies and sorting through the scattered, bloodied belongings of several dozen people blown apart by a suicide bomber at Kabul’s international airport, American traders and investors were busy parsing the utterances of three Fed officials.

“Oh, to be dealt such a hand in life,” is what some newly handless Afghan amputee would say, through burned lips quivering beneath layers of bandages, if you told her how stressed you were watching equity benchmarks drop a few tenths of a percent on the prospect that the men and women who conjure the world’s reserve currency might decide to create a few billion less US dollars each month starting sometime later this year.

As a reminder, America spends more US dollars each month buying bonds from itself than the country spent training and equipping Afghanistan’s defunct military. Funny how QE money is never described as “taxpayer dollars,” while politicians describe every cent spent on foreign wars as though it were extracted directly from your bank account. Think on that over the weekend.

In the course of documenting the taper talk that inspired Wall Street’s shallow Thursday swoon, I wrote that,

While it’s customary for everyone to weigh in during Jackson Hole, and while acknowledging that the opinion of non-voters matters little as long as Powell, Clarida and Williams are on the same page, this is overcommunication. Bullard’s comments were frivolous, Kaplan’s were confusing and George was par for the course. The only thing that came out of the whole cacophony was weakness in equities which will promptly reverse Friday if Powell leans dovish, as expected.

Fast forward to Friday and guess what? The weakness in equities promptly reversed as Powell stuck to the script, almost literally in the sense that his Jackson Hole address was just paraphrased excerpts from the July FOMC minutes.

Stocks ended up at new record highs. The S&P logged its best week in six (simple figure, below).

Not to put too fine a point on it, but that’s why I adopted an acerbic tone on Thursday while recapping remarks from Bullard, Kaplan and George. The interviews were pointless, as was Friday morning’s mind-numbing chitchat.

Powell can hold the hawkish banter up as a testament both to healthy dissent and some officials’ concerns about the side effects of the current policy stance for inflation and financial stability. But other than that, it’s just idle chatter.

The bottom line is that traders spent the past 48 hours relentlessly parsing different versions of the following general assessment: At some point over the next few months, we’re going to decide on a tentative schedule for reducing the pace of monthly money creation, contingent on the next two jobs reports and assuming the plague doesn’t keep getting worse. (Imagine a world where the July Fed statement just said that.)

Treasurys rose Friday, led by the belly. 10s ended around 1.30% (figure below). Breakevens widened.

Powell, Bloomberg’s Edward Bolingbroke wrote, “failed to strike the hawkish tone of multiple officials leading into Jackson Hole.”

Ok, sure. But let’s not kid ourselves. He was never going to say anything other than what he said. Powell isn’t a legendary orator. And that’s just fine when what you need is someone to read a summary of last month’s meeting minutes from a teleprompter while staring blankly at a sparse YouTube audience with a bookcase for a backdrop. (“I’m very important. I have many leather-bound books.”)

The minutes suggested consensus should pull forward their expectations for a taper timeline unveil to November or December. Powell simply reiterated that.

“Powell has made it clear that the FOMC will announce tapering soon – if the data continues to support the policy shift an official communication will be in the offing at the Nov/Dec meeting,” BMO’s Ian Lyngen and Ben Jeffery said, adding that “it’s difficult to envision the move on September 22 if for no other reason than the uncertainty introduced by the Delta variant.” Although the Fed “appears content with the assumption that the current wave of the coronavirus won’t have a material impact on the recovery, it’s an acknowledged risk at this stage,” they went on to say, calling that “a fact that will increase scrutiny of the economic data during the coming months.”

“The Fed chair did not provide any major new signal,” TD said, rather bluntly. “A QE tapering announcement is likely ‘this year,’ but most likely not as soon as September,” the bank’s Jim O’Sullivan and Priya Misra wrote, adding that “there was no new information on the pace of tapering once it starts [and Powell] also dovishly provided numerous reasons to believe that the recent strength in inflation will not be sustained.”

Some folks are still hanging on, though. Take Jeffery Elswick, director of fixed income at Frost Investment Advisors, who spoke to Bloomberg Friday. Jeff still thinks the taper unveil is coming next month. “I would fully expect they’ll formally start slowly cutting asset purchases in October,” Elswick said.

I’m sure Jeff’s a nice enough guy, and I have no idea how long he’s been doing this, but I can say with absolute certainty that Powell’s remarks on Friday didn’t point in the direction of a September unveil. That doesn’t mean it can’t or won’t happen. But to the extent anyone thought they heard that from Powell on Friday, those folks aren’t very adept at Fed tasseography.

Somebody called Mike hit the nail on the head. “Investors are breathing a sigh of relief as Powell suggests a kinder, gentler Fed tightening,” he told Bloomberg, for the same linked article. He based that assessment on “the equity move.” (Sharp guy, that Mike.)

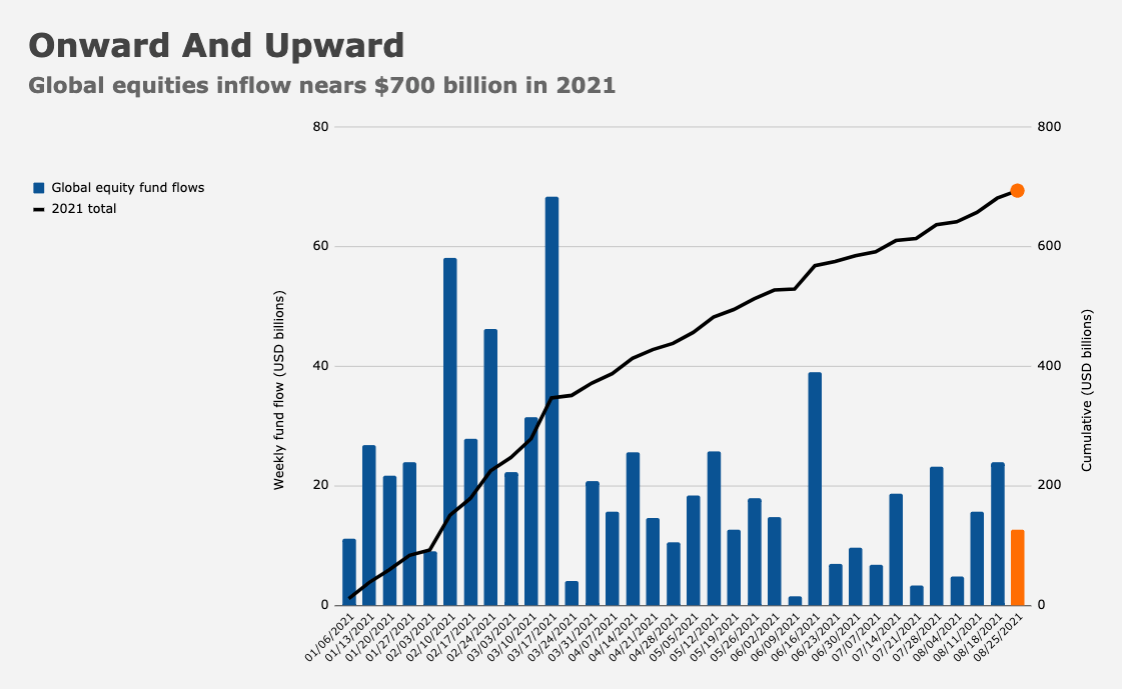

For what it’s worth, global equity funds took in another $12.6 billion during the latest weekly reporting period (figure below).

That brought the YTD haul to $693 billion.

Because I can’t immediately conjure a more effective Friday evening adieu, I’ll just leave you with a “by the numbers” summary from BofA’s Michael Hartnett. It seems particularly apt following Powell’s taper slow-walk:

COVID-19 pandemic by the numbers: 5.1 billion vaccinations, 214 million cases, 4.5 million deaths. The policy reaction: $32 trillion of monetary and fiscal stimulus. The Wall Street reaction: Global stock market capitalization up $57 trillion in 18 months. Despite >5bn vaccines, societies & economies remain hostage to the pandemic, allowing Wall Street to discount endless stimulus to the benefit of asset prices. The “end” of the pandemic will be very negative for Wall Street, but few think it “ends” soon.

When I was looking at paint swatches to repaint my office (which I call “the library” because I am an ass) I stopped the moment I saw Rich Mahogany. Now anytime I show a new person into the library, I take a deep inhale and announce, “Smells like rich mahogany.”

Your intro is brilliant, sir.

I try

H-Man, you spilled some good digital ink, close to the best but not the best you have inked. Tasseography stunned me until the Google search told me it was “tea leaves”. I was relieved to know it wasn’t a secret formula used by the Fed.

Same story, different day, but you tell it so well. Thanks

H- you might want to reconsider overpaying by 20% for that second home.

You might really enjoy it and you certainly have earned it. Can’t take it with us.

“Can’t take it with us”… reminds me of the closing lines from one of my best articles ever:

https://heisenbergreport.com/wp-content/uploads/2021/08/SixthPorscheExcerpt.png

Bravo sir! Bravo… you hit the nail on the head with the 3 non-voting stooges.