“Our view, negative returns for stocks and credit in the second half,” BofA’s Michael Hartnett reiterated, in the latest edition of the bank’s weekly “Flow Show” series.

This was a good week for those inclined to suggest the “house of cards” (as equities are often characterized) is poised to collapse. The rally ran up against a veritable laundry list of terrifying headlines.

Of course, critics have spent the last dozen years calling stocks a wobbly Jenga tower — a castle in the sky, built on cumulus clouds of nebulous policymaker promises, as I put it recently.

The problem with those kinds of pseudo-predictions is that past a certain point, it’s impossible for honest people to take them seriously. And not because they have no merit. They may have tons of merit. The issue is that anyone who rode the liquidity wave via something as simple as a low-cost index fund logged returns so stupendous that it would take a wipeout larger than that seen during the Great Depression to erase the gains.

Read more: Somebody Has To Be Wrong

I’m intimately familiar with this dynamic, by the way. I could tell you quite a few stories, one of which is a real “humdinger” (to channel Jeremy Grantham). But the simplest example is my ongoing aversion to Bitcoin.

Eventually, I’ll be right. It’s not so much that Bitcoin is worthless (it most assuredly is, but so is the dollar, so that’s not the real problem). The issue is that it doesn’t really exist. Not even in the context of other things that only exist in our minds, like stocks, bonds and corporations. Bitcoin, as I once put it, “is nothing.”

But here’s the key: That doesn’t matter if it goes from (I don’t know) $150 to $60,000, allowing a hypothetical HODLer to cash out with enough “real” money to buy an island, twenty Italian sports cars and six yachts. I think it’s fair to say the chances of Bitcoin falling below $1,000 are far greater than the chances the S&P trades back to its 2009 lows, but conceptually, it’s the same argument — claiming to be “right” about the price of assets (real or imaginary) when they eventually crash makes little sense if investors enjoyed a decade (or decades, plural) of gains, with ample opportunities to lock them in.

It’s with that in mind (i.e., with that caveat clearly enunciated) that I’ll confess to being increasingly sympathetic to the “cracks are emerging” narrative. That (“Cracks Emerging”) was the title of Friday’s daily from JonesTrading’s Mike O’Rourke, who noted that,

There are numerous reasons for soft pockets to emerge in the US equity market. The “three peaks in growth” for earnings, the economy and stimulus are primary. Then there’s the persistence of inflation and supply chain challenges. The Delta variant and pandemic uncertainty. Extended unemployment benefits are expiring. The expectation of a monetary policy adjustment is now joining the list. The most predominant factor since the start of July has been China. It’s becoming clear that the overnight news out of [Beijing] remains persistently negative.

Admittedly, it’s difficult to look past all of that. It has a “death by a thousand cuts” feel to it, and that was on display this week.

And yet, “Pavlov lives,” as I’m fond of putting it. Global equities took in nearly $24 billion over the latest weekly reporting period. It was the largest haul since the week of June 16 (figure below).

The YTD inflow is now $681 billion.

BofA’s Hartnett cited RBNZ. As late as Monday, a rate hike in New Zealand was a foregone conclusion. It was aborted 48 hours later after the country went back into lockdown following a handful of new COVID cases.

“Investors have zero fear of central banks,” Hartnett said. “RBNZ balked at raising rates despite house prices up 30%.”

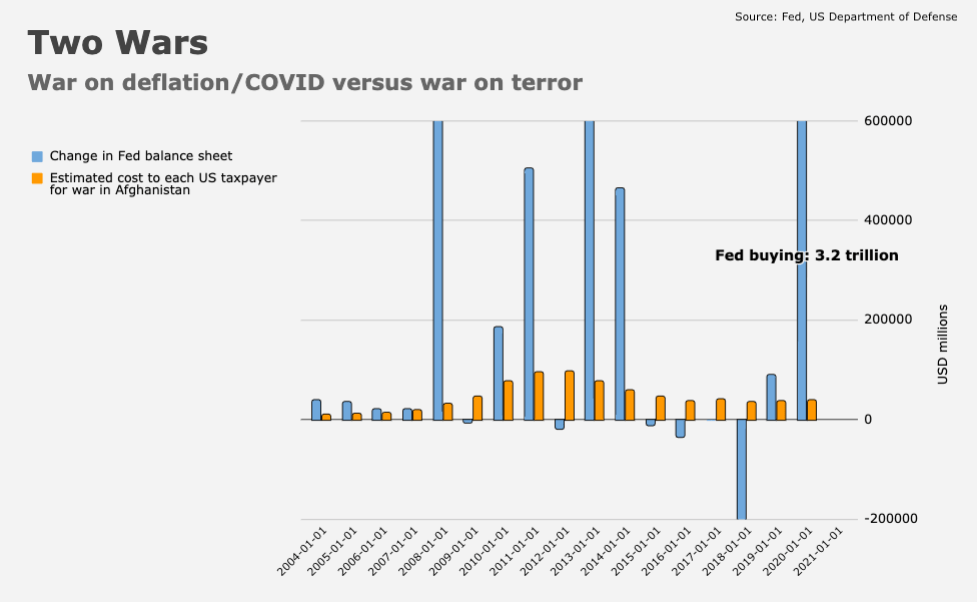

He also noted that “the Fed has bought $4 trillion in bonds over the past 18 months,” a figure that’s twice the amount the US spent on the war in Afghanistan over two decades.

The figure (above) might fairly be described as a “chart crime” (of possibly epic proportions), but it gets the point across. If you’re wondering, it’s derived from DOD comptroller estimates of direct war-fighting costs and the annual, end-of-year change in the Fed’s balance sheet.

“Global central banks have spent $834 million every hour buying bonds since COVID and the US government is spending $875 million every hour in 2021,” Hartnett went on to say. “Little wonder everyone believes in TINA and BTD.”

Stonks go up

Simplistically, if you think the primary and proximate cause of the current fear and weakness is Delta, and you think this Delta surge will peak and subside like the previous surges, then you’ll BTD when you think “peak Delta” is starting to peek over the near-term horizon.

With new case curves starting to round over in some of the worst hit states (TX LA CA etc) and hinting at rounding for the US as a whole, something is peeking.

True, all the other risks, dislocations, excesses still remain. We’re feeling our way from early stage to mid cycle. A big slug of fiscal stimulus will be withdrawn in mere weeks, and monetary stimulus will start easing off in mere months.

So you might well BTD less or differently than before, but some sort of BTD makes sense.