Perhaps unsurprisingly, China’s export growth decelerated in July, data out Saturday showed.

The spread of the Delta variant globally and associated containment measures are expected to weigh on external demand. Throw in a challenging comp and the numbers are likely to betray a slowdown. Indeed, export order components of recent PMIs printed in contraction territory.

It’s thus no surprise that exports grew “just” 19.3% last month (figure below). The market wanted 20%. The range of estimates from 20 economists was 15.4% to 30.7%.

Imports were solid, even as the 28.1% increase was well below the 33% YoY jump economists expected. The bottom of the range was 25%.

The numbers left a July trade surplus of $56.58 billion, near the middle of the range, and slightly higher than the median estimate.

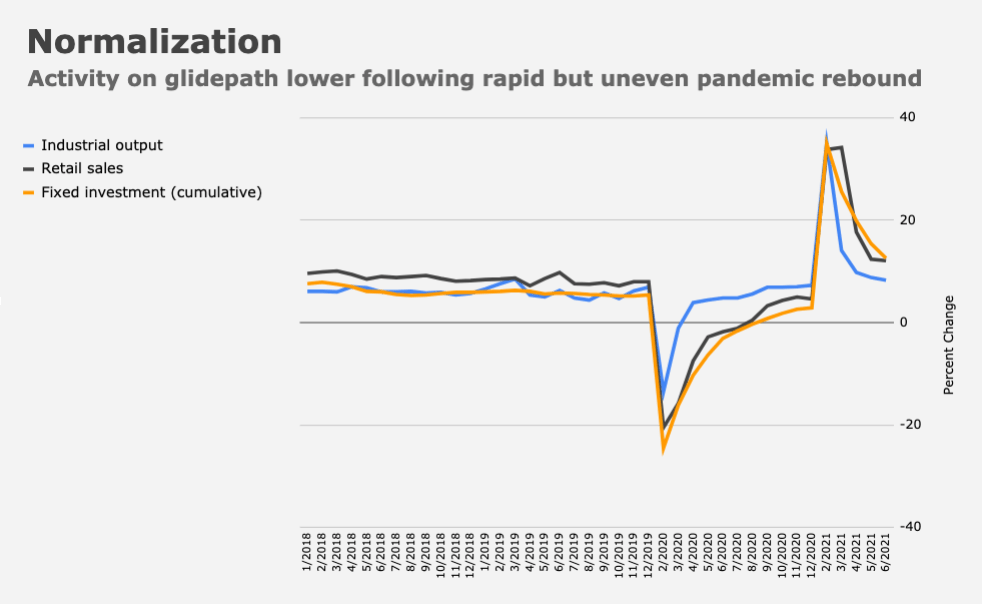

By this time last year, the world’s second-largest economy was well on the way to putting a pandemic that began on its soil in the rearview mirror, even as consumption lagged the rebound in factory output. Retail sales and imports eventually closed the gap (figure below), suggesting domestic demand was at least a semblance of firm considering the circumstances. But the recovery remained somewhat uneven.

China, like so many other countries, is dealing with a surge in new virus cases. “Surge” is a relative term. Questionable tallies, opaque reporting and the Party’s draconian “zero tolerance” COVID policy combine to keep the absolute numbers (very) low compared to other nations.

Officials and policymakers have telegraphed muted expectations for growth going forward. Last month’s RRR cut conveyed what some took to be a sense of urgency. The Politburo readout described an “even more complicated and grim” external environment and characterized the domestic economy as “not yet solid.” The Party vowed “enhanced cross-cyclical macro adjustments.”

Many analysts expect more easing in the second half, although as ever, it’s a juggling act for Beijing. Cutting rates isn’t exactly consistent with de-leveraging and otherwise guarding against speculative excess. The loan prime rate (which effectively replaced the “old” benchmark lending rate two years ago) hasn’t been lowered in 15 months (figure below).

Ostensibly, there’s plenty of scope to ease. The sheer number of levers China can pull in that regard is as dizzying as the tightrope act policymakers are perpetually forced to walk. Competing economic priorities collide at virtually every turn, and I’ve long described the absence of a major blowup as a “small miracle.”

“Exports and the COVID outbreak are the main sources of uncertainty in China for the next few months,” one analyst said Saturday.

“We expect a broad-based moderation in China’s activity in July due to local COVID outbreaks and policymakers’ deleveraging initiatives,” SocGen’s Wei Yao and Michelle Lam wrote, in a Friday note. “The global recovery should keep exports supported for now,” they added, but flagged “tepid consumer demand” and a likely continuation of “the deceleration in non-financial credit growth.” The bank cited local COVID outbreaks in warning of “downside risks” to Q3 GDP.

And yet the CNY to USD conversion has been really tricky these past 18 months.

“complicated and grim” No S___.

We may have to start shipping to (horrors!) Africa.

I can’t wait for this pandemic to be tamed.