“Cautious.”

That’s how one popular strategist is feeling right now, as traders turn the page on a remarkable first quarter (and not just for markets).

Rates, regulation and redistribution will be key themes in the second half, BofA’s Michael Hartnett said, in the latest edition of his popular weekly “Flow Show” series. That’s a familiar refrain from Hartnett.

The “three Rs,” as it were, “mean we are cautious on asset returns in 2021,” he wrote, adding that “SPX 3,400 [is] more likely than 4,400 in the next six months.”

That sounds like an innocent enough suggestion. A ~13% decline might fairly (indeed, accurately) be called “pedestrian” in the context of the historic rally from the March 2020 pandemic lows.

And yet, like Ron Burgundy, a decline from Friday’s levels to 3,400 would seem like “kind of a big deal,” especially given renewed faith in the notion that markets can only go higher (a hallmark of melt-ups).

So, what would it take to get stocks sustainably to new highs in the second quarter? Well, for Hartnett, it “would require lower-than-expected inflation given booming growth [is] now super-consensus.” “Oil never lies,” he remarked.

Next, he ran through some numbers which, while familiar, don’t seem to be losing their capacity to elicit at small eyebrow raise: “Oil +51% past nine months, copper +87% YoY, food prices +27% past nine months, lumber +212% YoY, US house prices +19% YoY, digital art in $69 million NFT sale and shipping freight rates +297% Y/Y.”

There’s some inflation. Let’s hope it’s “transitory.”

I jest at Fed officials’ expense. And yet, you’d be disingenuous to deny that at least some of the price pressures manifesting in, for example, record highs on PMI input price gauges and lumber going parabolic, aren’t the result of temporary distortions created by pandemic dynamics from supply chain shocks to froth in the US housing market.

What should probably concern folks, though, is the rise in global food prices. It feels like I highlight the chart (below) at least three times per week, but Hartnett used it in his latest, so here it is again.

That’s a recipe (no pun intended) for problems in developing and frontier economies, and it could be a figurative and literal death sentence in extremely poor countries. The read-through is potential societal unrest. Not in the developed world, but elsewhere.

In any event, I’ve been over that on too many occasions to count so I won’t pound the (dinner) table on it further — or at least not until in manifests in an uprising in some country Americans couldn’t identify on an unmarked map if their lives depended on it.

On the flows side of things, it’s notable that the latest weekly reporting period showed $45.6 billion into cash. That was the largest inflow since April of last year, when the scent of panic was still thick in the pathogen-laden air. ICI’s data showed a $62 billion inflow in the week to March 24 (figure below).

Global equities took in just $4.1 billion last week, on EPFR’s data. That was the weakest inflow since December.

US equity funds saw outflows of $9.7 billion, the largest exodus in 13 weeks.

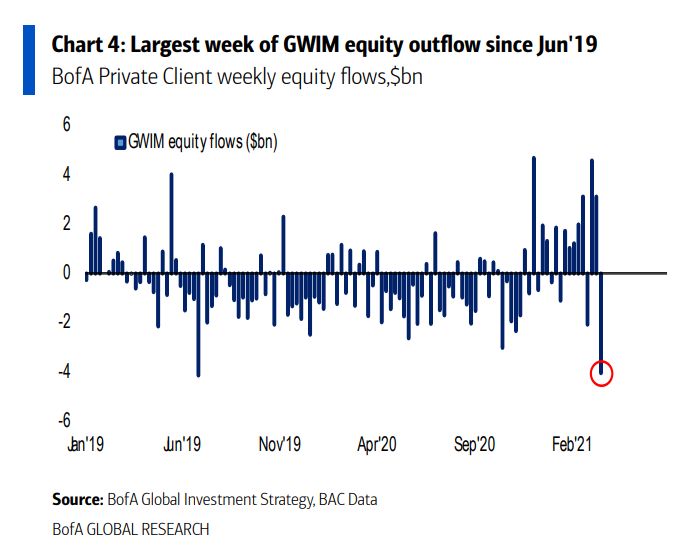

Meanwhile, BofA private client flows showed the biggest equity outflow since June of 2019.

Maybe they’re “rebalancing.”

Many investors, and banks’ private clients are probably well represented, have gotten used to investing in a particular group of equities: big US tech, QQQ, SPY. That type of equity might have been 40-50% of a typical private client portfolio circa 2019.

Those investors, and their wealth managers, have limited appetite for cyclicals, value, small cap, international. The managers’ allocation guidelines, imposed by the bank’s CIO, will only “permit” 10-20% in those secondary equity classes.

If your wealth management advisor thinks big tech-QQQ-SPY are looking toppy – not an unreasonable view, I think – and peels 10-15% of portfolio weight out of that stuff, he or she is not going to put it all into cycl-sml-intl, because that stuff “can’t” be 20-35% of the portfolio. Ergo, net outflow from equity.

Tax considerations will also drive flows. With higher taxes on the higher-income looking more likely in the coming year, private clients will be motivated to realize gains at today’s capital gains rates.

I haven’t seen data, but I’d suspect those private client portfolios are shifting into cash, short duration fixed, tax advantaged munis, private equity funds, and the like.

“With higher taxes on the higher-income looking more likely in the coming year, private clients will be motivated to realize gains at today’s capital gains rates.”

Well put, JYL.

But that’s just a silly focus on real life. What’s the matter with you??

All we should care about is what vol levels are dropping out if the monthly vol history!

I wonder how soon this nonsense will follow “Unconstrained Bond Funds” (remember them?? It was not all that long ago…) and factor ETFs into the dustbin of Wall Street history, where they belong.

This was really informative, thank you Sir.

The other thing I will add – from the vantage of 16 years on the institutional buyside then 5 in the private client side before what I’m up to now – is that private clients and the wealth management organizations that serve, if one can generalize, tend to be risk averse, focused on absolute returns, and rather lagging.

If you track the BofA Fund Manager Survey, it is a good reflection of mainstream portfolio manager views, and thus tends to be a couple to a few months “behind” the start of market shifts. The bulk of private client portfolio allocation decisions are not any “earlier” than the FMS.

This is just a generalization, of course.

“or at least not until in manifests in an uprising in some country Americans couldn’t identify on an unmarked map if their lives depended on it.”

Honduras, Guatemala, El Salvador. It is already manifesting there. Americans do care greatly about these places, even if they can’t identify them on a map, because immigration from these places is a huge political issue.

Is that monthly or quarterly “rebalancing”, it’s all so confusing.