Jerome Powell’s uncharacteristically deft navigation of treacherous waters around the March FOMC meeting provided a spark for risk globally on Thursday, but consternation began to creep in as yields moved higher.

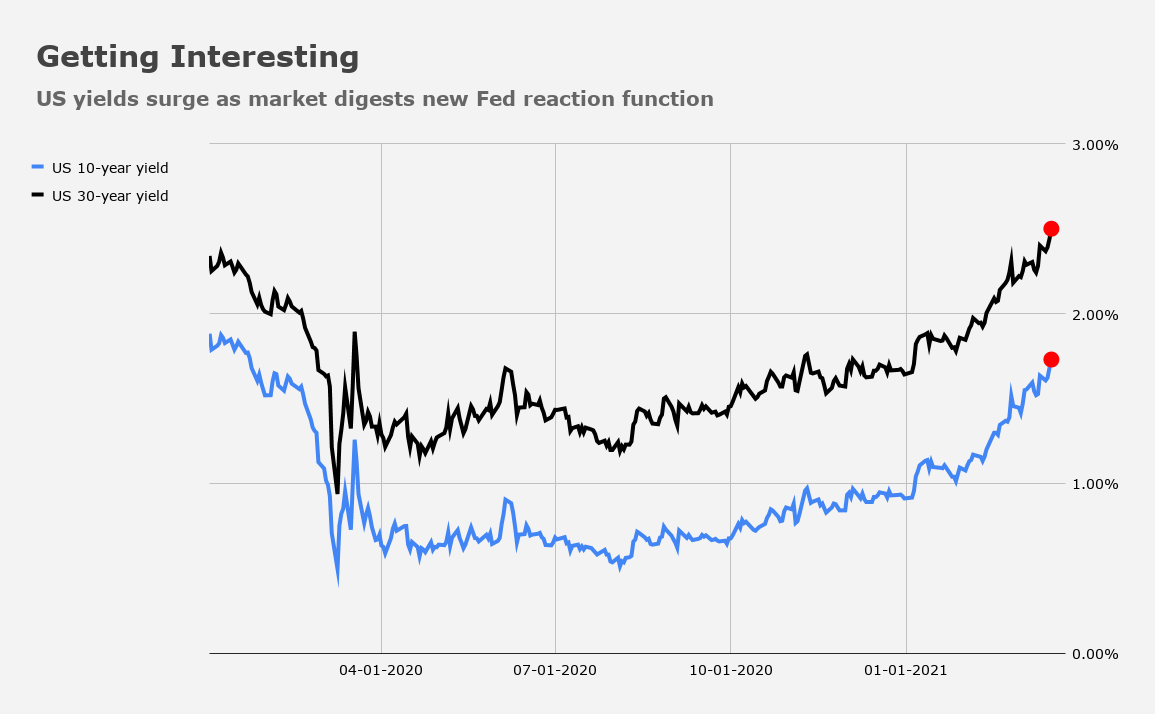

Treasurys led losses for global bonds as the US 10-year pushed through 1.70% and the 30-year through 2.50%, taking bunds and gilts along for the ride. The market met “the new Fed” (as some were characterizing the situation) on Wednesday, where that means the Committee’s “show me” attitude towards inflation effectively gave the green light for traders to push bear steepeners.

The Fed generally disavowed the notion that hikes will be any semblance of preemptive, even as a few dots shifted higher versus December. Powell repeatedly emphasized that the Fed wants to see actual, realized inflation move higher, and generally refused to engage in any kind of speculation about how far long-end yields would need to rise to prompt intervention. That, along with the upgraded macro forecasts, was just “asking for it” (if you will) vis-à-vis steepeners.

Treasurys were heavy in Asian trading as a hot employment report Down Under weighed. Losses extended on reports the BoJ will widen the band for JGB yields and then accelerated as London got going. “There was a sharp fixed income selloff on the European open,” AxiCorp’s Stephen Innes remarked, adding that “the dollar gained as a result.”

That weighed on US equity futures, especially the Nasdaq. Stocks were pleased with Powell on Wednesday, but remember: It’s all about how “orderly” any extension of the selloff at the long-end turns out to be. A disorderly move would cause consternation.

The UST-bund spread widened out to 200bps, the most in at least a year. Transatlantic divergence is likely to be a theme going forward, as Europe struggles with vaccine rollout and Christine Lagarde increases the pace of purchases under the ECB’s pandemic emergency program.

The question now is whether the good vibes engendered by Powell’s surprisingly (accidentally?) adept inauguration of the Fed’s “new” decision calculus will fade on concerns that the bear steepening impulse might take on a life of its own. The Fed could push back, verbally, but it’s a long time between now and the next SEP meeting, leaving plenty of scope for the market to push the issue.

Some are fairly sanguine. “Yesterday, Jay Powell said, in effect, that the Fed has no intention of preemptively tightening policy in order to make sure inflationary pressures can’t build. They’ll act when they’ve got the economy back to maximum employment, or when they can see the whites of the eyes of the inflation beast,” SocGen’s Kit Juckes said Thursday, adding that “childhood fairy tales warn that this is risky, but I think Powell is a breath of fresh air.”

For Juckes, like Janet Yellen, “the benefits of trying to get discouraged workers back into the US labor force, outweigh the inflation risks.”