Traders and investors (and those are two distinct types of market participants, as I’m fond of reminding folks on occasion) can expect to endure another week of incessant speculation about the path of bond yields and the evolution of Fed policy.

Joe Biden’s stimulus plan is in the homestretch, and when considered with an upbeat jobs report and sharply higher oil prices, the inflation warnings will be ubiquitous.

As a kind of tangential aside, Brent crude is now above fiscal breakevens for some Middle East producers (figure below). OPEC’s decision to keep the market on a tight leash until the recovery is assured, served to bolster prices further last week.

Higher crude prices add fuel to the reflation trade and have helped energy shares in the US play catch up with pandemic winners, most notably tech.

Of course, oil’s rise coincided with a rebound in those “other” breakevens, as inflation expectations firmed. That drove the rise in yields for the better part of the equity rally, but more recently, surging real yields have raised concerns about a possible de-rating in expensive corners of the market seen vulnerable in a pro-growth macro regime.

Note that even after the Nasdaq’s brush with a technical correction last week, shares are still very expensive (figure below).

That suggests there’s room for further multiple compression in the event yields keep rising.

Traders will be keen to see how supply is digested in the days ahead. Recall that a disastrous seven-year sale on February 25 was a kind of “last straw” for the market. That debacle caused considerable consternation and will cast a shadow.

“3-year, 10-year, and 30-year auctions will be closely watched as litmus tests for potential market dysfunction,” TD’s Priya Misra said. “Overall there is $2.7 trillion in net coupon supply slated for FY2021, compared with $1.3 trillion in FY2020,” she added. “This should put upward pressure on term premium.”

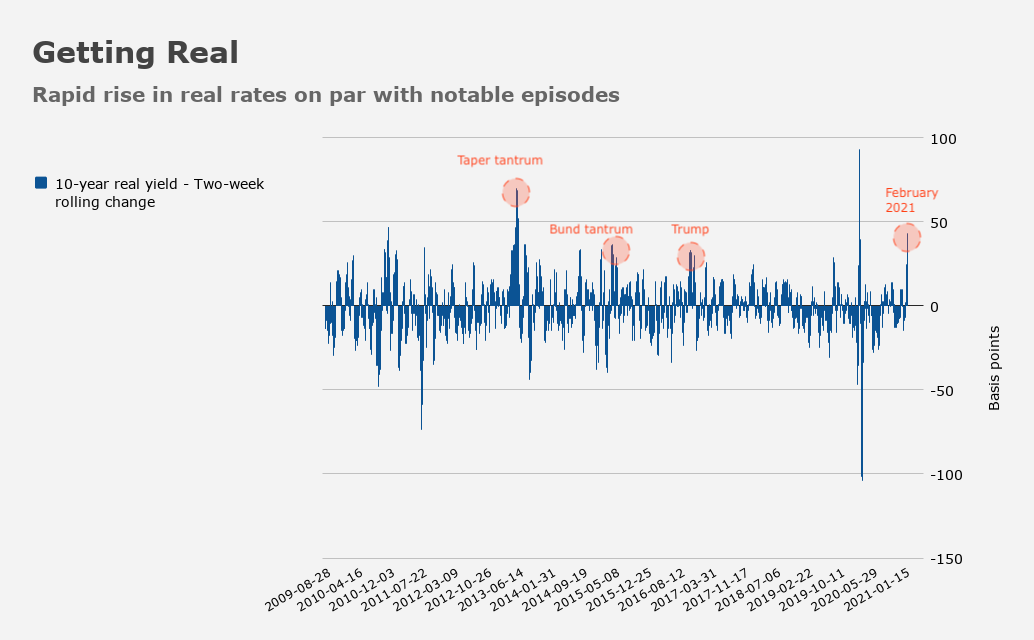

TD lifted their 10-year yield forecast to 1.75% in the near-term. “Given that real rates are still low on a historical basis and Powell didn’t seem to push back against the move, we expect real rates to continue to rise,” Misra went on to say, late last week. Her forecast sees 10-year reals jumping all the way to -25bp by the end of this year.

If that were to pan out, the fate of equities would hinge on the pace. A gradual grind higher predicated on improving growth expectations and, crucially, buffered by Fedspeak that underscores the “patient” narrative, could be digested with relative alacrity. But as we saw over the past several weeks, rapid moves higher can be highly destabilizing.

“10-year real yields neared -60bp in the wake of the jobs report – nearly 50bp higher over the course of the last four weeks and more than sufficient to bring into question risk asset valuations,” BMO’s Ian Lyngen and Ben Jeffery said. “By erasing the year-to-date gains in domestic equites, investors are voting with their feet as the expression goes.”

Indeed they are. Were it not for a somewhat manic Friday rally, US stocks would have suffered significant weekly declines.

CPI is on deck this week. With the market on edge and the Fed in the quiet period, a “hot” print could cause a stir with no opportunity for officials to push back. Not that they would anyway.

As alluded to above, there’s $62 billion in supply coming up between 10s and 30s, and another $58 billion in a three-year sale on Tuesday. “It’s a tail as old as bonds (see what we did there?),” BMOs Lyngen wrote Friday.

If you don’t get the joke, that’s ok. You’ll understand it well enough if the market ends up choking on any of this week’s supply. “Given the uninspired takedown of the seven-year auction, the phrase ‘proceed with caution’ is especially apropos,” Lyngen added, in the same note.

Seems to me that the parameters of the oscillations of life – politics, investing, pandemics, computing , oil prices, social media influence and cryptocurrencies to name a few – are increasing in amplitude and decreasing in period. Is much of this volatility due to the injection of liquidity by central banks? Are subdued interest rates the only thing keeping it all from exploding.

Good comment. There have been several articles in these pages regarding this question, often referencing Alexandr Kocic. The main takeaway, if I remember correctly, was that CBs actions dampened market volatility, but with nowhere else to “go”, it showed up elsewhere, e.g. in politics. And politics have been volatile indeed in the last couple if years. So maybe, with the reutrn of sanity we are seeing a reversal of this trend.

As for your second remarks, probably “yes”.

return of sanity to the white house

There may be sanity in the white house but there are still trolls under the bridge.

With no news from Powell on whether the SLR relief will be extended at the end of the March I think we are in for a choppy week. At the same time the US Treasury is reducing its outstanding treasury bill position by $922bn by the end of March, resulting in a further injection of liquidity. Interesting times and it would be interesting to hear Heisenberg’s views.

ManofLourdes, you’re right, there are (still too many) trolls under bridges, yet the removal of the biggest troll of all did reduce political vol by a lot.