Traders will stare down a deluge of data and a bevy of Fed speakers in the first week of March, as the market ponders what’s next after what Goldman on Friday evening called “a bond vigilante attack.”

The February jobs report may underscore the lack of momentum in the labor market as Democrats push to pass Joe Biden’s stimulus plan before key benefits lapse in mid-March. Senate Democrats had some ideas about how to maneuver around an unfavorable parliamentarian ruling on the minimum wage hike, but it seems unlikely they’ll find a workable “solution” that allows for the swift passage of the overall relief package.

January’s jobs report was, of course, a disappointment. Consensus is looking for around 150,000 on the headline for February. As Bloomberg wrote, “private payrolls will be watched closely after pandemic-related restrictions eased in many states in recent weeks, likely allowing for increased hiring at service businesses like restaurants.” The figure (below) is a simple “you are here” visual for the labor market.

Leisure and hospitality, you’re reminded, shed another 61,000 positions in January. Downward revisions to December’s already poor numbers for the sector showed losses that month were larger than previously reported, at -536,000.

The scales on the visual (below) have been adjusted to “trim” the anomalous losses and gains in and around the first lockdowns last year. The point is to show that while myriad data suggests the US recovery is proceeding apace, the labor market remains hobbled, and especially services sector employment.

The bottom line is that until services sector jobs return, the economy as a whole will find it difficult to sustain a recovery, stimulus sugar highs notwithstanding.

The relevance of the jobs data for the bond selloff is questionable. For one thing, we’ll have several sessions of price action to digest before we even get the jobs report. In addition, BMO’s Ian Lyngen and Ben Jeffery note that “the price action itself has become the event and as such, attention will remain on the feedback between higher rates and equity valuations.”

“At the moment, stocks appear wary, although content to hold off any larger correction for the time being,” they added.

Last Thursday’s fireworks included one of the largest single-day jumps in five-year yields in decades, as the market repriced the Fed.

Speaking of the Fed, officials will be… well, they’ll be speaking. And that includes Jerome Powell, who will join a “Conversation on the US Economy” at a virtual Wall Street Journal jobs summit on Thursday. Monetary policymakers around the world pushed back last week in both word and deed as rates spiked. Traders will be keen on any similar pushback from Fed officials this week.

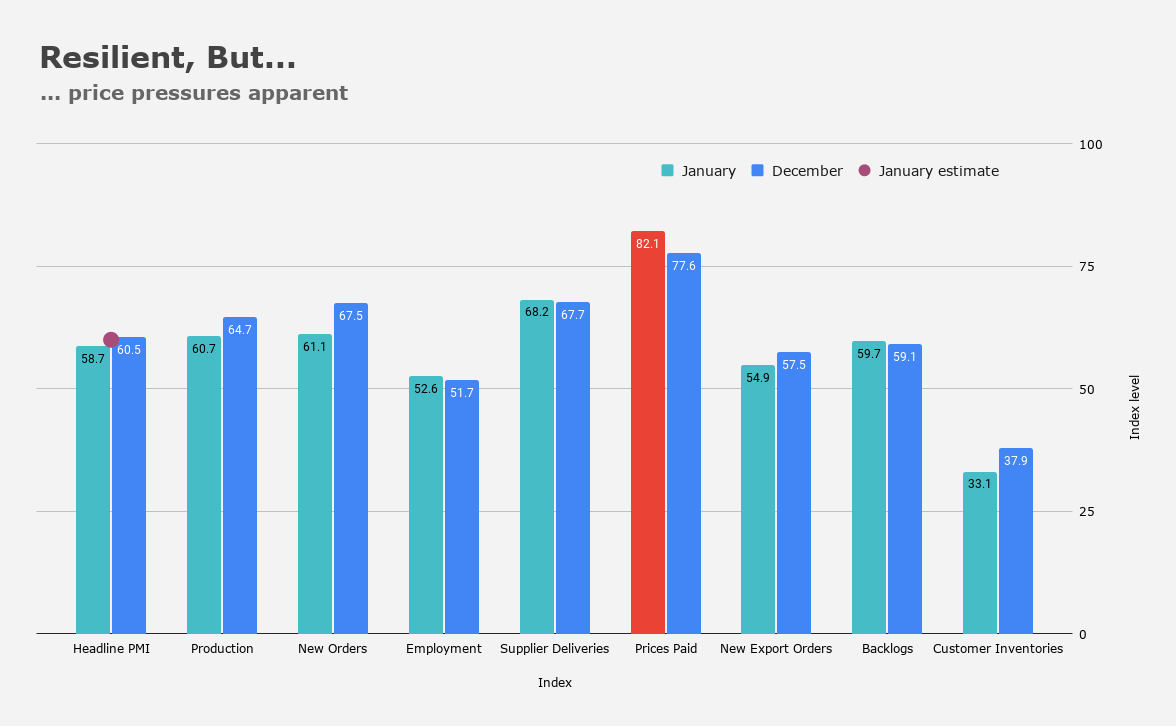

Also on the docket: ISM manufacturing and services. The focus there will be on price pressures. Recent PMIs indicate sharply higher input prices and varying degrees of pass-through to end consumers.

Some of the pressure is expected to abate as supply chain disruptions ease, but record prints on PMI price subcomponents are feeding inflation fears. That dynamic will likely be on display with the February ISM vintages.

In the January manufacturing survey, the prices paid gauge printed the highest in nearly a decade (figure above), while the customer inventories index hit the lowest since 2009.

For market participants, everything in the new week will be viewed through the lens of the backup in rates.

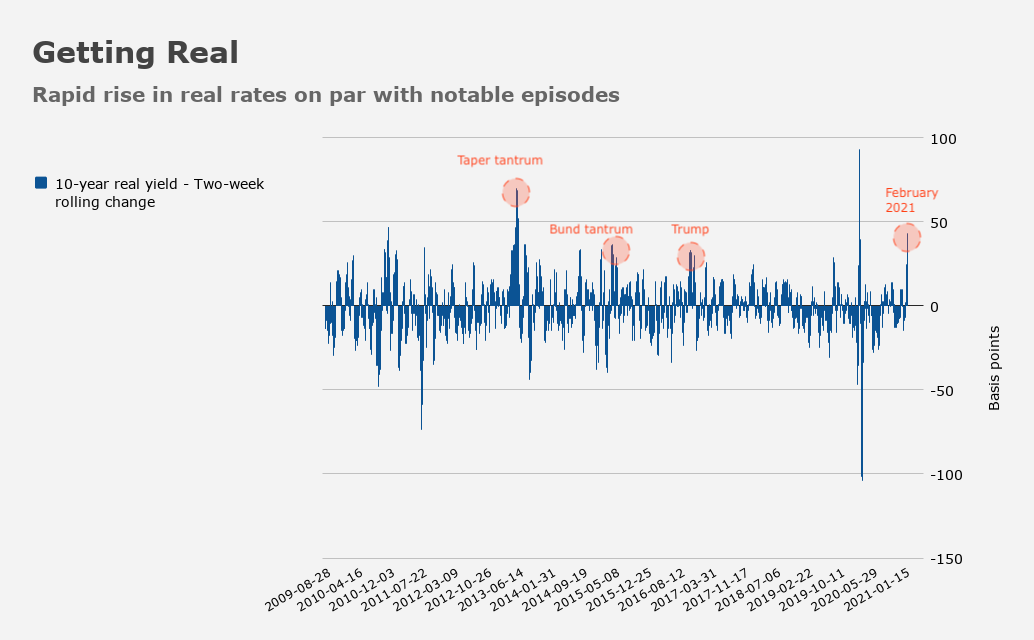

Remember, it’s not just the level of nominals that matters. It’s the rapidity of the move and the character of the selloff. As Goldman’s credit team noted, “the velocity of the monthly move in real yields [was] on par with recent spike episodes [including] the post-2016 election reflation theme return, the 2015 ‘Bund tantrum,’ and the 2013 ‘Taper tantrum.'”

As the bank’s Lotfi Karoui went on to say, “it also mark[ed] the first time since the beginning of the selloff that higher yields hurt risk appetite.”

Ominous? Maybe. As one former president would say, “We’ll see what happens.”