For as long as I can remember (which, admittedly, isn’t usually very long given that prior to 2016, I had an expensive Balvenie habit), one bank has consistently warned that a two-standard deviation move in US bond yields will cause indigestion for equities if it plays out over a short enough timeframe.

That bank is Goldman. Whenever bonds look poised to sell off materially, the bank tends to remind investors that it’s not necessarily the size of the move that matters, as much as it is the rapidity.

Given recent events, it’s no surprise that the bank is now reiterating the point. The market just witnessed a global bond tantrum, which culminated in Thursday’s fireworks stateside. 10-year US yields rose some 50bps over the past month. That’s a large move in a short period of time.

One “problem” for risk assets is that the bond selloff is now being led by real yields. While reals are miles below levels that prompted the mini-bear market in late 2018 (indeed, except for the 30-year, they’re still deeply negative), the swiftness with which they’ve recently risen is potentially destabilizing, something Goldman’s David Kostin acknowledged in a Friday evening note.

“While rising breakeven inflation has driven most of the rise in yields during the past six months, the last two weeks have been characterized by a 40bp jump in real yields,” he wrote, adding that “conceptually, and historically, equities digest rising inflation expectations more easily than rising real yields.”

And it’s not just equities. Gold is struggling, Bitcoin fell nearly 20% last week (figure below), and you can expect emerging markets to have problems too in the event US real rates continue to push higher.

If you’re wondering whether the backup in rates has forced Goldman to reassess their constructive outlook for stocks, it hasn’t, especially not if what you’re asking about is the level of rates (as opposed to the rapidity of rate rise).

“Investors ask whether the level of rates is becoming a threat to equity valuations [and] our answer is an emphatic ‘no’,” Kostin said Friday.

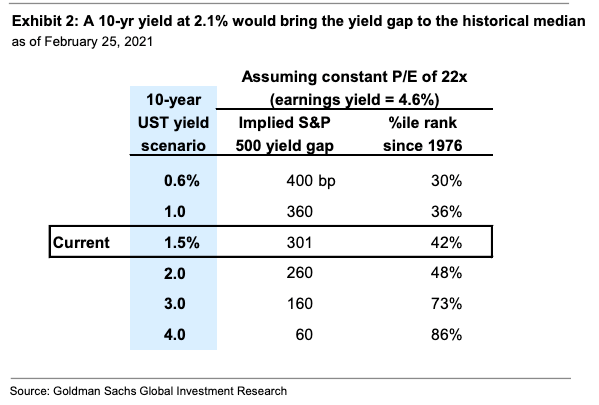

Although the S&P does trade with a forward multiple that ranks in the 99th percentile (exceeded only during the dot-com boom), Kostin said the equity risk premium implied by the bank’s DDM model ranks in just the 28th percentile, which he noted is “70bp above the historical average.” Along the same lines, the spread between the index’s forward EPS yield and 10-year Treasury yields is only in the 42nd percentile, even after the recent bond rout.

The takeaway, from Kostin, is that “keeping the current P/E constant, the 10-year yield would have to reach 2.1% to bring the yield gap to the historical median of 250bp.”

Additionally, Goldman reminded investors that their (upbeat) forecast for US equities already had higher rates baked in. Better growth would generally be consistent with higher bond yields, and also with the bank’s forecasts, which, as a reminder, call for S&P EPS to be 10% higher than pre-pandemic levels in 2021. Kostin’s target remains 4,300 for the index.

Goldman of course acknowledges that sharply higher yields can drive dispersion and otherwise shake things up below the index level. Secular growth favorites and anything that’s benefited from the long-running “duration infatuation” in rates is suddenly under siege. While things will probably be less acute going forward, Kostin wrote that “investors must balance the appeal of promising businesses with the risk that rates rise further and the recent rotation continues.” That’s just a nice way of saying that while your favorite big-cap tech companies are probably still great investments over the longer-term, in an environment characterized by hot economic growth and rising rates, they may fall out of favor.

Coming full circle, the bank reiterated that rapid rate rise is usually a problem, all constructive commentary notwithstanding.

“The recent change in yields has reached a magnitude that is usually a headwind for stocks,” Kostin said, adding that equities typically fall 1% during months when nominal rates jump by more than two standard deviations. When real yields rise by a comparable magnitude, stocks tend to fall 5%.

I always appreciate a post that confirms my investment situation.

I fall into the “unsophisticated investor” group- but I continue to learn and love reading that “investment people way smarter than me” see things the way I do (haha)