Don’t count the “bubble” burst just yet.

While some recent evidence (both anecdotal and otherwise) suggests rising prices are beginning to curtail demand in the flaming-hot US housing market, it may be too early to call the top.

New home sales in January rose 4.3% to a 923,000 annual rate. That was far better than consensus expected. The market was looking for 856,000. The range, from more than five-dozen economists, was 750,000 to 940,000.

Prices were sharply higher versus 2020. The median new home price ($346,400) rose more than 5% from January of last year, even as prices dropped from December. The average selling price was nearly $409,000.

More than a fifth of new homes sold last month cost more than a half-million dollars. That was a 16% jump from the prior month.

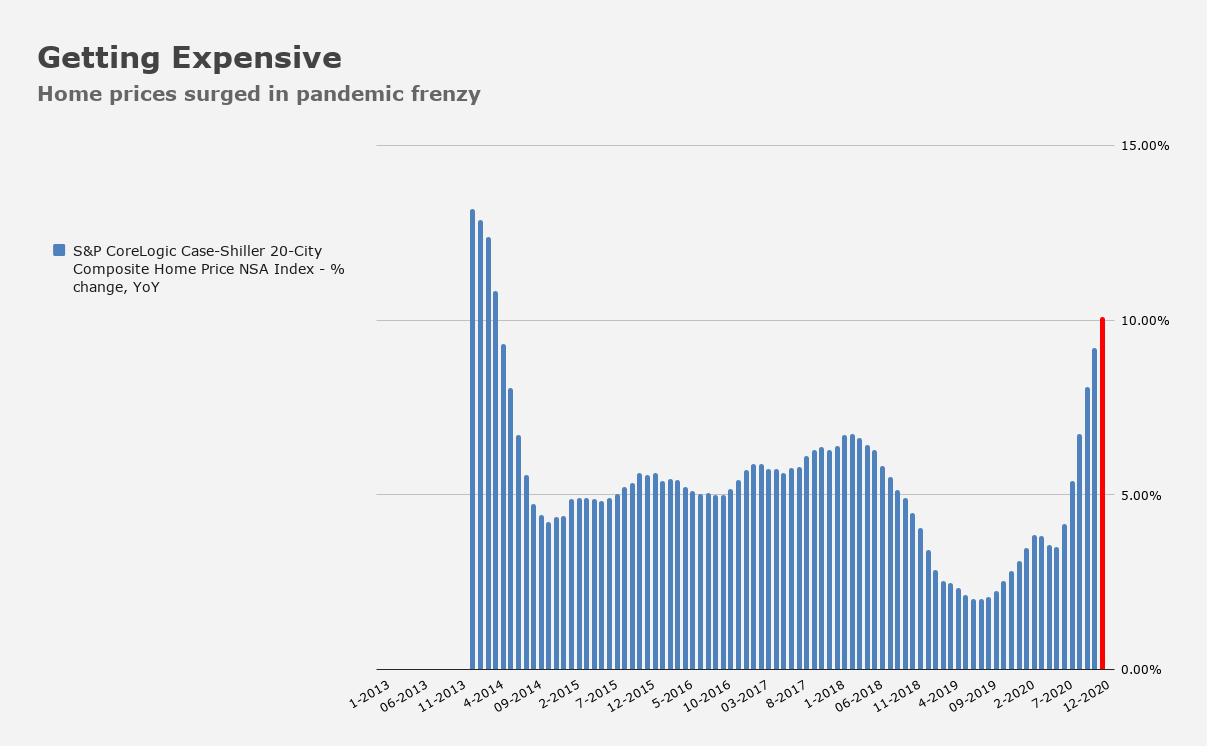

Data out earlier this week showed property values rose more than 10% in December from the previous year.

The jump in the S&P CoreLogic Case-Shiller index was another “since 2014” moment.

Meanwhile, weekly mortgage applications dropped 11%, in part due to Texas effects, if you will. “The severe winter weather in Texas affected many households and lenders, causing more than a 40% drop in both purchase and refinance applications in the state last week,” Joel Kan, MBA’s Associate Vice President of Economic and Industry Forecasting, remarked on Wednesday.

As for the rest of the country, activity is generally strong, even as the MBA noted that “mortgage rates have increased in six of the last eight weeks.” Borrowing costs plunged last year amid the Fed’s pandemic response, helping to keep the market affordable even as prices surged.

In the color accompanying the weekly mortgage apps data, the MBA said the average loan size of purchase applications rose to $418,000. That is, of course, in part due to low inventory, and it’s also a record.

Toll Brothers (which enjoyed last year’s boom in high-end properties) said Tuesday that net signed contract value was $2.51 billion in the first quarter. That was up 68% YoY. Contracted homes rose 59%.

CEO Douglas Yearley, who late last year called the US housing market “the strongest I have seen in my 30 years at [the company],” still sounded confident. “The housing market remains very strong, driven by a tight supply of new and existing homes for sale, favorable demographic trends, low mortgage rates, and a heightened appreciation for home ownership, especially among our customers,” he said Tuesday.

The company’s guidance shows it expects deliveries of between 10,000 and 10,400 homes this year with an average price of between $790,000 and $810,000.

I wonder if there is a gene that could help predict if, later in life, one is so inclined to be comfortable with debt. Kind of like the gene for myopia.

If so, this is perhaps among the best times in history for those genetically pre-disposed to be debtors. Brilliant for those taking out a 3.68% 30-year on a Toll Brothers in some desolate ex-urb in the flats, outside some over-heating, Sunbelt city. Much more so if the over-expected hyperinflation materializes. Those with the vision purchase the option for the second, 3-ton air conditioner.

It’s interesting to run across pandemic friendly trends & imminent return to normal stories, sort of like spring fever. Who can blame Pollyanna for tuning out where we all were a year ago!

Today, we still have tons of people infected and spreading Covid at a rate not too different than a year ago — before 500,000+ deaths. Vaccinating a small percent of our population at this point isn’t a great success story, but it’s hopeful. Disturbingly, for many months, it’s been suggested that far, far less PCR testing is being done — basically because it’s too expensive for all the hospitals, labs and medical folks that aren’t reimbursed (at profitable rates). Thus, we basically have inaccurate sketchy virus data in most of our communities. Sadly, the virus is adapting rapidly — while humans play profit games — not to mention the inability to sequence unfolding genetic threats. It also probably doesn’t help that our herd is in denial and burned out from 12 months of chaos. Who’s to say how Covid will play out in the next year …

In terms of future inflation, GDP, asset bubbles and home values spiking — we still haven’t seen too much economic damage from a year ago. We’ve watched the Fed buying time, investing in denial and laying the groundwork for optimism, and so far, most everyone is positive. Stocks up, homes up, all is well! That’s fine, hopefully people will have a reasonable path forward.

Nonetheless, risk and volatility are very much in play, even as the all clear flags are flapping in the wind.

Here’s a FRED chart looking at assets and liabilities — and just a dumb reminder that the massive elephant in the room (under the rug) is still very much in the room:

https://fred.stlouisfed.org/graph/?g=BlzW

Toll Brothers is raking in the money in my area. You can’t find a new home for under 6 figures and and homes that are over 40 years old and only 1200-1300 square feet sell for $500,000 and up. That makes it hard for the average person to get out of what was their starter home. (“.Average” meaning those who make under a combined income of $120,000). Those who make less don’t stand a chance of getting into a single family home. Condos are expensive as well when you include monthly condo dues into the mix