Rising yields caused further consternation in equities to start the new week, as bonds extended this year’s rout.

At one juncture, the US 5s30s pushed near 158bps, the steepest since October of 2014. 10-year yields touched 1.39% before pulling back.

Some worry that the growth and inflation expectations now built into bonds and curves have overshot economic reality. That just underscores the risk to equities, especially with some parts of the market trading at extreme valuations.

Commodities are front and center. Goldman lifted their target on Brent to $70 in the second quarter and $75 in the third. Investors, the bank said, will use crude to help reposition themselves for a reflationary environment defined by additional stimulus and higher inflation. JPMorgan recently made similar comments in calling for a commodity “supercycle.”

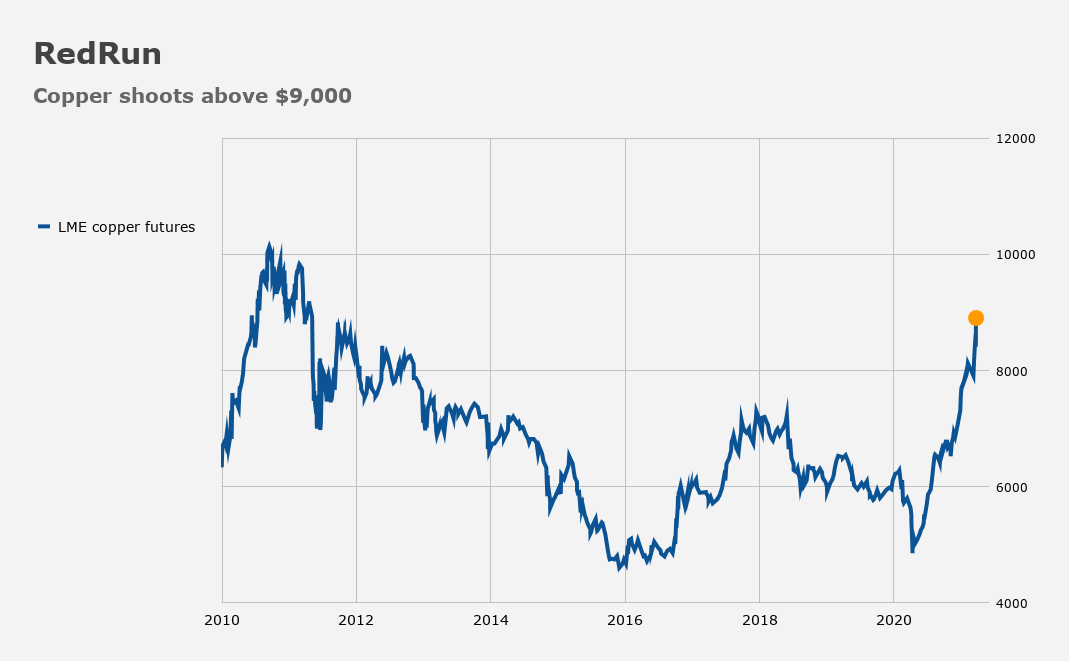

Copper, meanwhile, pushed above $9,000. It’s tracking for an eleventh consecutive monthly gain. That would be a record.

While the reflationary vibes are clear, what’s less so is whether equities are prepared to cope with the increasingly assertive “tone” of the narrative. It’s the same question over and over again. Can stocks, accustomed to years of falling yields, flatter curves, subdued growth, and “slow-flation,” perform in an environment where none of those assumptions hold?

Of course, as alluded to above, this is all rather extended, even considering the market’s penchant for pulling forward expected future outcomes. The virus is on the back foot, but challenges remain and I should parrot the usual caveats about slack in the labor market and pervasive output gaps. While supply chain constraints, pent-up demand, and fiscal stimulus may well cause an “overshoot” in the near-term, the longer-term outlook for the reflation story is less clear.

In Australia, the RBA was forced to defend its three-year yield target Monday. The central bank waded back into the market to the tune of AUD1 billion as yields pushed higher on the back of the global reflationary impulse.

“Everything on the screens suggests taper tantrum fears are building, and investor reaction is understandable, even if inflation is still a 2022 issue,” AxiCorp’s Stephen Innes said Monday.

Emerging market equities could well take a hit in the event US yields continue to press higher. Chinese stocks tumbled by the most since last summer to kick off the new week, although I’d caution that there are always idiosyncratic factors to take account of in China, so it’s perilous to implicitly attribute one day of price action in mainland markets to any broader narrative.

The bottom line is this: To the extent rising yields represent a positive outlook for the global economy, there’s palpable consternation that we’re close to “too much of a good thing” territory in the near-term, and that some reflation respite is in order.

“The benign view is that we get a big enough yield rise (nominal or real, who cares?) to stop the general risk rally for a bit and as the bond market rallies in reaction and with a super-dovish Fed as backstop and vaccines to look forward to, risk assets recover, bond yields settle into new ranges and the dollar’s fall can resume,” SocGen’s Kit Juckes remarked, summing things up.

“The alternative view is that the market becomes convinced both that higher inflation is coming and that the Fed is going to have to hurt the global economy to get it under control,” he added.

The blind seer from O Brother, Where Art Thou?

“You seek a great fortune, you who are now in chains. You will find a fortune, though it will not be the one you seek. But first… first you must travel a long and difficult road, a road fraught with peril. Mm-hmm. You shall see thangs, wonderful to tell.

You shall be on the 99th floor of a building in flames, all of you attempting to occupy an elevator down to the first floor at the same time, ha. And, oh, so many startlements.

I cannot tell you how long this road shall be, but fear not the obstacles in your path, for fate has vouchsafed your reward. Though the road may wind, yea, your hearts grow weary, still shall ye follow them down that shaft, even unto your salvation.”

Wow, all the way to 1.39%, the world will surely end soon. What is it with this? Have we completely forgotten actual “high” rates? My first mortgage was at 7.5% in 1970. My bonds were paying 7-9% for virtually the whole 1970s decade, much more for what I bought on 65% margin. If our current markets are heaven then how can 15bp blow them up? Come on, man!