Point, counterpoint, I suppose.

The reflation narrative is making a comeback after taking a brief hiatus, but some think that narrative may be detached from reality.

One of those people is SocGen’s Albert Edwards who, on Thursday, expounded a bit on the topic. “Much of the equity and commodity world has raced higher on the back of the reflation trade,” he said. “The unusually deep inversion of the breakeven curve tells us the trade may have gone too far and is about to unwind.”

He cited a number of additional data points and visuals in the course of making the case, including a disconnect between PMIs and consumer confidence. The visual (below) is a kind of 30,000-foot view of the reflation zeitgeist.

As far as factors that could spoil the party, Edwards mentions a decelerating Chinese credit impulse.

That’s important. As most macro observers are acutely aware, China’s credit cycle at times feels disconcertingly synonymous with the global economic cycle. That’s a kind of chicken-egg dilemma, and sometimes folks take it a bit too far, but there’s a lot of truth in it.

“China has been one of the few economic bright spots in a COVID-hit world,” Edwards wrote, adding that “historically, a downturn in China’s credit impulse is bad for cyclicals and commodities.”

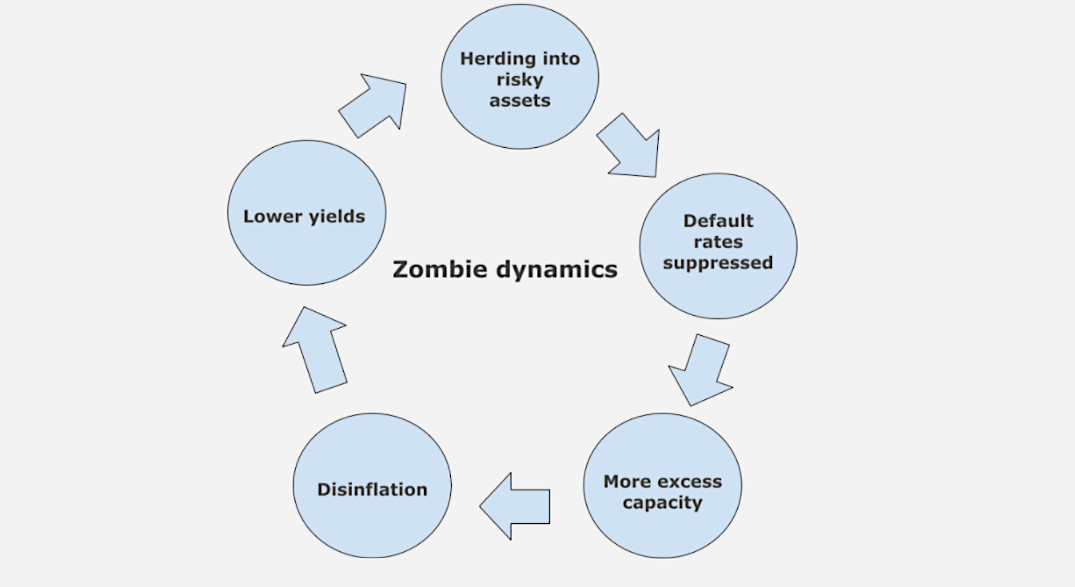

Meanwhile, the zombies are still roaming. Indeed, they’ve proliferated in a world where earnings have collapsed but access to capital markets has remained wide open thanks to central bank backstops. The figure (below) uses a Bloomberg proxy, but you can obviously show the same dynamic any number of ways.

Even as bankruptcies in the US surged to the highest in more than a decade last year, policy support prevented the kind of credit apocalypse that might have otherwise unfolded. In addition, the hunt for yield engendered by the same monetary accommodation drove investors out the risk curve and down the quality ladder, thereby forestalling “creative destruction.”

I’d remind you that “creative destruction” is a fun euphemism for this: “The kind of chaos nobody living in an advanced economy is actually prepared for, no matter what they say on Twitter.” I vastly prefer the phrase: “Preventing the purging of misallocated capital.”

Do yourself a favor and use that in place of “creative destruction.” You can always make a plausible argument for the purging of misallocated capital, assuming you can prove it’s “misallocated.” “Creative destruction” takes you into the philosophical realm, where you probably don’t want to go.

“Transfers to firms, together with credit guarantees and funding-for-lending programs, have prevented bankruptcies that might otherwise have occurred but also [kept] some unviable firms afloat, which could put a drag on overall productivity in the future,” the IMF said, in the Fund’s latest World Economic Outlook, which revealed that a staff analysis of more than a dozen advanced economies from 1990 through 2020 showed bankruptcies falling during the pandemic recession. I used the chart (below) last month, but I’ll present it again here.

Obviously, that’s anomalous. Whether it’s desirable or not is in some sense a normative question.

The IMF wrote that “if policy support is withdrawn before the recovery takes firm root, bankruptcies of viable but illiquid firms could mount, leading to further employment and income losses.” Edwards on Thursday pointed to the deflationary implications, calling it “why we are currently overrun with these deflation-inducing and productivity-stifling ‘Zombie’ companies.” The figure (below) is adapted from a Matt King slide deck, although it’s been so long, I couldn’t put a date on it.

Coming full circle, professional trader Kevin Muir drew a distinction between “reflation” and “inflation” in his latest note to subscribers on Wednesday evening.

“‘Reflation’ is not the same thing as ‘inflation,'” he said, adding that,

‘Reflation’ is easy to rein in. All you need is to withdraw the stimulus. The natural state is for prices to drop without external forces being applied. Inflation, not so easy. Once it starts, it’s harder to stop. We haven’t had traditional inflation in a long time. I know there are lots of prices that have risen quite a lot over the past couple of decades, so I’m not arguing the current inflation rates represent true levels of price rises. The hedonic adjustments definitely have a way of keeping reported inflation much lower than it “feels” in real life. However, inflation represents an across-the-board rising of prices. That’s a lot different than economically-sensitive commodities responding to “reflationary” stimulus.

Kevin noted that from where he’s sitting, it doesn’t appear that markets are actually pricing in “inflation.” Rather, they’re just riding the reflationary narrative for a trade.

“The two-year inflation swap has rebounded from 0.00% to 2.25%, but look at the 30-year swap,” he said. “It’s sitting just slightly above the two-year at 2.35%.”

Muir contends that folks simply don’t believe that real inflation is likely to be “a thing” (so to speak) anytime soon.

“If the market was concerned about long-term inflation, this curve would be steep,” he said. “Instead, it’s flat.”

I looked up COPX and XME when reading the last article. Look a little toppy. Wouldn’t be the worse thing in the world if they come down to meet their 200 DMA in late March/early April.

The bankruptcies goes against any realistic expectation. Of course, there is an explanation it would seem. Some commentators a few months ago were talking about how it would be a good time for some government entities to try the re-organization route. That doesn’t seem to be happening. So, we have to expect bailouts instead, I guess.

Still in the deflation camp myself.

Commercial real estate bankruptcies could become a thing soon. Second- or third-order effect if commercial real estate doesn’t get bailed out is that it’ll help the big, downtown cores recover via cheaper rents. If not the next big thing, then maybe more bailouts on the way for this sector (and cities) and downtown rents stay high…and buildings vacant. Do zombie buildings walk?

Deflation camper here … my prepandemic recollection was that corporate debt was already at record highs all the way back then, now dramatically higher, same for public debt, add in the accelerated utilization and influence of the pandemic tech interventions that will remain ingrained in our new realities, sprinkle in devastating employment numbers, mix in a little urban to unprepared suburban exits…hard to see inflation for at least a couple of years…

I have been reading Albert Edwards since he and James Montier were at DrKB, putting out some of the most thought provoking pieces on the Street. That’s 20+ years ago now. I love reading his stuff. That said, this is a guy whose timing can be off by years. Decades, even.

The proposed slow ramp up of the minimum wage to $15/hour by 2023 could put a floor on the post-reflation deflation. If Democrats do assert their mandate, I could see voters demanding more inflation-inducing government action.

So these zombie companies have about four years to out-earn their interest. What’s a good way to hedge this risk?

GDX could be one component.

Not a gold bug, but in the current environment with policy “normalization” being far away and more stimulus (better: much needed help) coming it’s hard to see how gold miners should not profit.

Even IF inflation should return, gold as the classic inflation hedge stands to gain.

The most obvious hurdle, of course, would be (rapidly) rising interest rates to fight that same inflation, but currently that seems out of question, given the propensity of CBs to “look through” inflation overshoots.