“[The] outlook remains positive – buy the dip,” reads the first line of the latest note from JPMorgan’s Marko Kolanovic, out Wednesday.

Last year was an interesting one for Marko, who wasn’t shy about weighing in during the early days of the crisis. He wasn’t bashful in the lead-up to the elections either.

I’m just going to repeat (verbatim) what I said last month, while summarizing Kolanovic’s 2021 outlook, and that’s the following. Whatever you want to say about his analysis in 2020, one thing you can’t say is that he was wrong about the direction of risk assets. If Marko’s job is to correctly predict the direction of markets, he got it right. In the weeks after US equities abruptly plunged into a bear market during the March panic, Kolanovic called for a swift rebound in stocks to record highs. Subsequently, he made similar calls, and stocks kept climbing. In November, his longstanding prediction of a dramatic rotation in favor of pro-cyclical laggards played out in dramatic fashion, and only began to wane last week.

In his latest, Kolanovic took note of recent market developments, including the over-the-top (to put it generously) frenzy catalyzed by the Reddit crowd’s grudge against a handful of shorts and more generalized pronouncements that the broader market is in a “bubble.”

“We have seen a number of strategists calling for a market correction or indicating equities are in a bubble,” Marko said. “In the last few days, we have witnessed turmoil related to trading activity in small highly shorted stocks.”

Yes, indeed we have witnessed that. But, for Kolanovic, it’s best to stay focused on a trio of factors which, for him, argue that the outlook for equities remains “firmly positive.” Those factors are low positioning, the expected improvement in the pandemic as vaccines are rolled out (and herd immunity achieved), and the likely durability of monetary and fiscal support.

“Any market pullback, such as one driven by repositioning by a segment of the long-short community (and related to stocks of insignificant size), is a buying opportunity, in our view,” he said Wednesday.

The reference to “repositioning” is to the dynamics discussed here Wednesday morning, and Marko’s allusion to things “of insignificant size” is reminiscent of Goldman’s recent contention that while pockets of “unsustainable excess” exist, they generally don’t pose a high “systemic risk to the broader market given their modest share of market cap,” to quote the bank’s David Kostin.

Crucially, Kolanovic wrote Wednesday that “equity positioning is in the 30th percentile relative to the past 15 years, both for systematic and discretionary managers.” The reason, he said, is “simple.” To wit, from Marko:

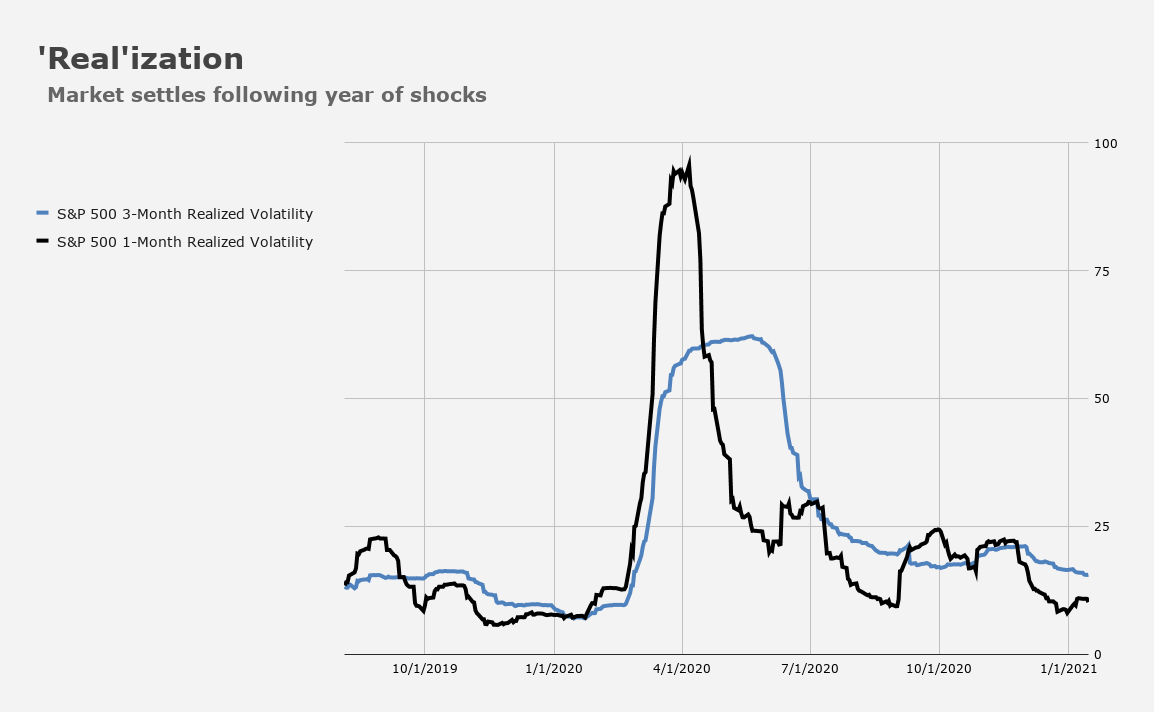

Market expectations of volatility and tail risk are still very high (e.g., as indicated by VIX, variance convexity, etc.), and historically that has been the main impediment for institutional buying of equities. Figure 1, below, shows the equity beta of global hedge funds as well as our model for equity exposure (percentile) of systematic investors – they are largely following (inverse) volatility, and currently there are no signs of exuberance in institutional equity positioning.

He sees the VIX falling into the mid-to-high teens, which should mechanically drive re-leveraging from the current 30th percentile to the 60th.

Kolanovic also flagged a near record spread between realized vol and the VIX. Realized, you’ll recall, has steadily moved lower, helping to catalyze re-risking from vol-sensitive investor cohorts.

As far as COVID is concerned, Kolanovic says we’re almost out of the proverbial woods. It is, of course, true that the past several months have been tragic, especially for western economies. And there are concerns about vaccine-resistant strains, which Moderna is hoping to address quickly.

But, there’s a light at the end of the tunnel, according to JPMorgan. “Given the estimation of natural immunity (cumulative cases), current pace of vaccination, as well as other considerations, we expect the pandemic to effectively end in Q2,” Kolanovic wrote Wednesday, noting that obviously, this would have meaningful implications for growth expectations. He cited the possibility of “significant” outperformance in equities versus bonds, as well as a prospective acceleration of the cyclical value over growth trade and what he called “a new commodity bull market.”

When it comes to central banks, there’s nothing particularly complex about the narrative — they’re accommodative and that’s generally bullish. When you throw in the likelihood of more fiscal support, the combined effect for financial assets is substantial. Just ask 2020 (and note that many see last year’s commodity rout ending emphatically in 2021 as the reflationary vibes become entrenched).

Marko does delve into a couple of risk scenarios, which I’ll touch on later. I think it’s appropriate to give them due consideration via a dedicated article, separate from his base case.

What, in essence, is that base case? Well, in case you couldn’t surmise it from everything said above, Kolanovic writes that,

The monetary and fiscal backdrop of 2021, along with the strong recovery from COVID-19 and relatively low positioning in risky assets, should be positive for stocks and commodities and negative for bonds. We believe Inflation will be an investment theme, reinforcing bonds to equities flows, and a continuation of the rally in value stocks and commodities, and steepening of the yield curve. Short-term turmoil, such as the one this week, are opportunities to rotate from bonds to equities.

I’ll leave that to stand on its own merit.

You must be logged in to post a comment.