The US corporate bond market remains robust coming off a banner 2020.

Last year, both investment grade and high yield supply hit records, as management teams took advantage of extremely favorable market conditions created by the Fed’s unprecedented backstop for corporate credit.

Borrowing costs for corporate America fell to record lows despite a raging pandemic that triggered the most large bankruptcies since the financial crisis.

Generally speaking, analysts expected supply to abate in 2021 because… well, because last year’s issuance was so vigorous that it was difficult to imagine how this year could top it.

But things are off to a quick start. In fact, junk sales are on the verge of topping their all-time January record, set “way” back in 2020.

Junk supply sat near $35 billion headed into Friday. In January of last year, issuance totaled $37 billion.

There’s no mystery here. It’s the hunt for yield driving demand and the assumption that, political bickering over the Fed’s lending powers aside, this is one genie that isn’t going back in the bottle.

That is: You can shutter the Fed’s facilities if you like, but the market understandably thinks this horse has left the barn. If the corporate bond market were to come under siege again due to some extremely exigent circumstances (e.g., a new, vaccine-resistant strain of the virus), investors think the Fed will be there, come hell or high moral hazard.

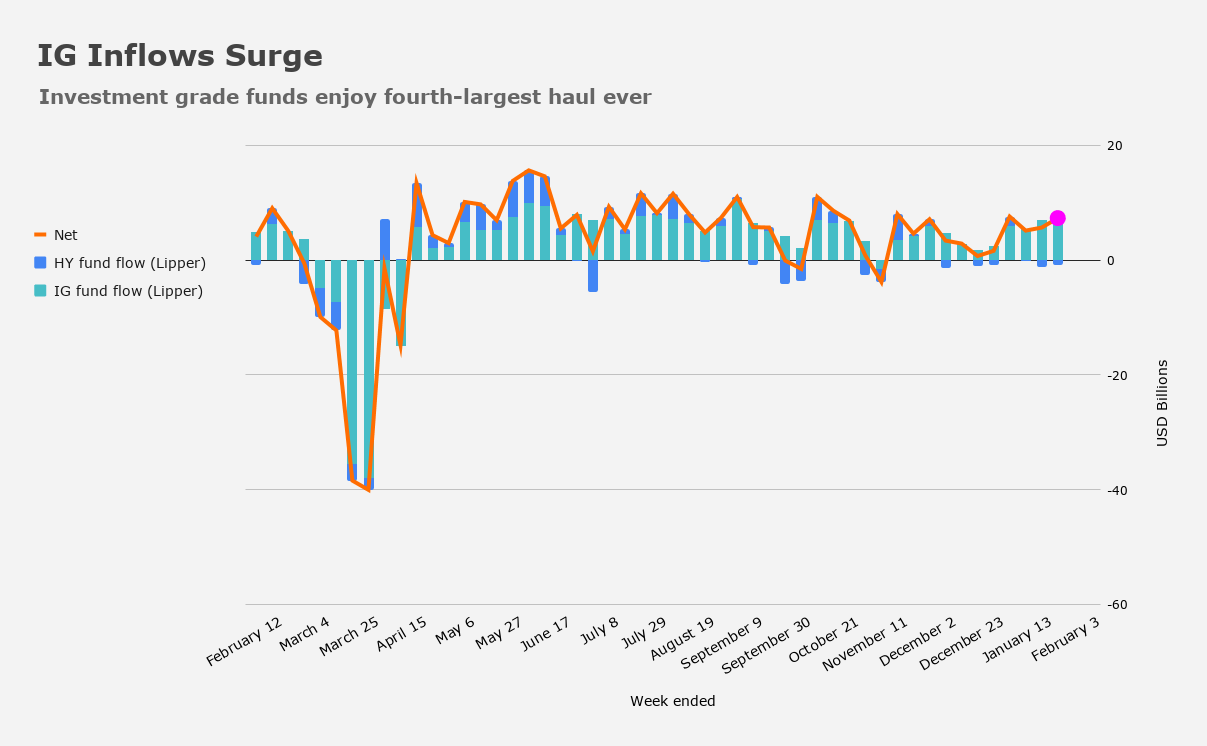

Although high yield funds are seeing small outflows in the new year, investment grade funds took in $8.25 billion in the week ended January 20. It was the fourth-largest haul ever.

Investment grade borrowers have tapped the market for more than $100 billion in January.

There are some signs of reticence, though. “While US investment grade borrowers are still paying flat to minimal new issue concessions, new deals were less than 1.7 times covered Thursday, signaling that investors’ bid for new issues may be deteriorating at current levels,” Bloomberg wrote late last week. A separate account noted that fresh high-grade bonds weren’t performing particularly well in the secondary market as risk premiums widened “on about half of new sales.”

In any event, the overarching point is that we’re still in a reach-for-yield environment, where the prospect of structural economic damage from the pandemic and more bankruptcies hasn’t proven sufficient to stop, for example, CCC yields from hitting new record lows last Thursday.