For those making $60,000 or more, the recovery is complete.

That’s one takeaway from data gathered by the Harvard-based Opportunity Insights Economic Tracker, which, as the project’s website explains, “combines anonymized data from leading private companies to provide a real-time picture of indicators such as employment rates, consumer spending, and job postings across counties, industries, and income groups.”

As of midway through December, employment for the highest income cohort was actually up (albeit only slightly) from mid-January 2020, just before the first case of COVID-19 was identified in the US.

Even during the worst days of the nationwide lockdown, employment for those earning $60,000 or more never fell more than 13%, according to this data. The low point was on April 16, when employment was lower by 12.8%. Within a month, it had recovered to just a 5% decline. By June 16 (so, two months from the trough), employment for those making $60,000 or more had almost fully recovered.

As the figure shows, the juxtaposition with lower-income Americans could scarcely be more stark. During the darkest days of the first pandemic lockdowns, employment for those making $27,000 or less was down by nearly 40%.

The recovery for the poor (and, let’s face it, if you’re making less than $27,000 per year, you’re poor — the only possible exception would be situations where two or more people are cohabitating and sharing expenses), the recovery stopped in July. And that’s unfortunate because it was at the end of July when benefits under the first massive federal relief package began to lapse.

More disconcerting still, the blue line in the figure (above) shows that the situation began to deteriorate anew for lower-income Americans after Thanksgiving. There were matching declines for middle- and higher-income earners, but they bounced back. Through December 13, the same recovery was not evident for the lower-income cohort. (The data after October 22 appears to be provisional — it’s shown with a dashed-line in the original. Opportunity Insights includes this note: “The series is based on data from Paychex and Intuit, worker-level data on employment and earnings from Earnin, and timesheet data from Kronos.)

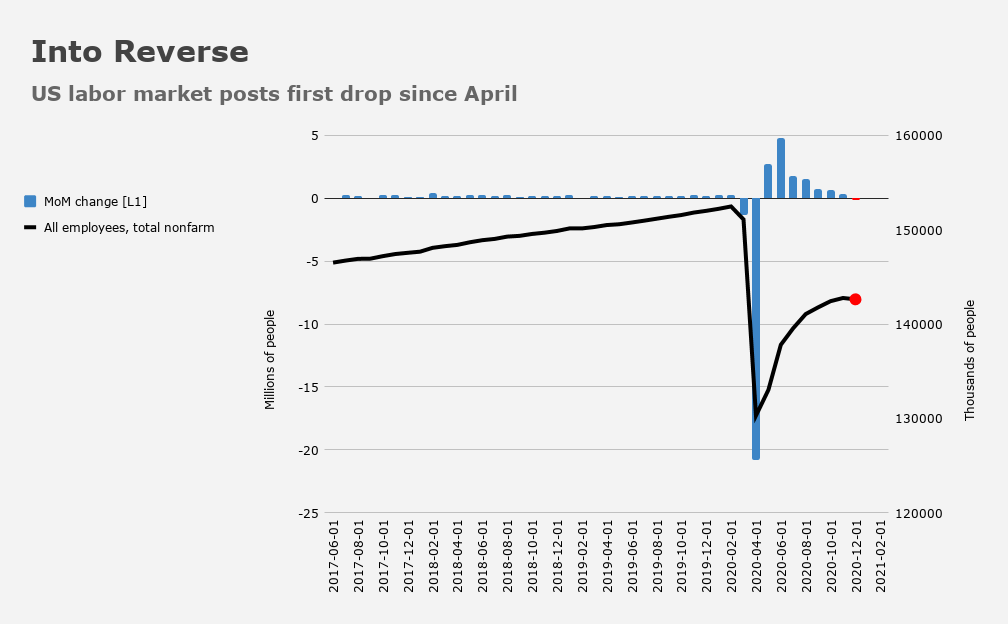

Of course, this is hardly surprising. After all, nearly a half million leisure and hospitality workers lost their jobs in the December NFP period.

I’d also note that, in the Opportunity Insights data, the trajectory of the recovery flatlined for low-wage workers long before nonfarm payrolls posted the first monthly decline of the COVID era. It wasn’t until last month that the headline NFP print turned negative. But the improvement for lower-income Americans stopped four months previous, according to the data cited above.

It’s now painfully obvious (and “painfully” can be taken literally for many Americans) that overt, direct efforts must be made to ameliorate the situation described above.

I’ve talked at length about the extent to which the largest economy on Earth operates on borrowed time. It’s a Ponzi scheme, of sorts. As Deutsche Bank’s Aleksandar Kocic put it in April, “the truth is simple.”

What is the “truth”? Well, as Kocic explained at the time, “a surprisingly large segment of the population is practically one paycheck away from some kind of insolvency.”

“In the absence of a major disruption, the system is capable of moving along by collecting small installments of rent (‘clipping the coupons’) from a large segment of the population,” he said. “However, if an exogenous shock disrupts the fragile order of these cashflows, there is a chain reaction of collective insolvency ready to sink the entire system.”

The renewed downturn in leisure and hospitality employment last month and subsequent drop in retail sales was yet another testament to how fragile that system really is, something I elaborated on in “Here’s The Real Problem With December’s Jobs Report” and also in “America’s Economic Model Is Unsustainable. Empower The 4.”

I never tire of quoting myself. I’ve been humbled and had more Icarus moments in my life than most men, but a small fraction of my old arrogance remains, and manifests harmlessly these days in my penchant for citing my own writing. With that in mind, the following description and accompanying pseudo-prediction is, in my opinion, especially poignant:

A disproportionate amount of economic activity is accounted for by consumption that takes place at restaurants and retail stores. The people doing the eating and the shopping are, by and large, not making much more than the people serving the food and stocking the shelves, precisely because they are the same people (in an economic sense).

How is that sustainable? It’s circular to the point of absurdity. The people providing the services for meager wages are in most cases the same people consuming them when they’re not providing them.

This is why supply-side economics doesn’t work. Handing out tax breaks to the rich can’t possibly make an impact because the rich aren’t generally participating in this not-at-all virtuous loop, unless it’s to pay nearly as much for one Starbucks drink as the barista “crafting” it makes in an hour.

If you think any of that is going to change just because America (narrowly) decided to cancel “Celebrity Apprentice: White House Edition,” you’re wrong. The next four years will witness a return to sanity and, hopefully, a restoration of civility, but for everyday people, the economic reality will be the same as it ever was, if not worse depending on how efficient the COVID-19 vaccine rollout goes.

I hope I’m wrong. The problem, though, is that even if I’m only partially correct in my assessment of where we’ll be in four years, the electorate will be just as vulnerable to dangerous narratives as it was in 2016.

America needs heavy-handed federal intervention to close the wealth gap and ease the socioeconomic tension.

Before you shout “socialism!” or “communist!” know this, dear reader: The dynamics are exponential, not linear.

That means that even if you consider yourself “rich” currently, you will find yourself falling further and further behind those richer than you. And they will find themselves falling further behind those richer than them.

This isn’t “healthy” capitalism or some kind of virtuous “meritocracy.” Rather, it’s a perpetual motion machine of inequality creation.

It makes gods of a few (e.g., Jeff Bezos and Elon Musk) and renders everyone else a pauper. If not in the sense that you’re starving (as so many Americans are), at least in a relative sense.

Let me put this in terms that my affluent readers can understand. When you go to trade in your mid-sized luxury sedan in five years, you may discover that an E-Class is going to cost you nearly as much as an S-Class would have run you previously. And it won’t be because of “regular” old “inflation.” It’ll be because you’re getting priced down the Mercedes line as a result of the dynamics described above. Before you know it, you’ll face the “terrifying” prospect of being a C-Class driver.

Amen!

It’s all relative and when the bottom drops out it sucks everyone down.

Sorry, I would have left a comment sooner but not for being so deep into Deaths of Despair. I was at the chapter sub-header “One Escalator Becomes Two Escalators, One of Which Stopped.”

Regardless of the class, be it the status-rich S-, or the menial E- or C-, much less the Sun City rich A-Class, it won’t be safe to cruise around at night unless one is tooling about in a leafy suburb of Charles Murray’s Coming Apart. Barring resolute, legislative (and fiscal!) action to pivot hard toward addressing some serious problems, it will hardly safe at night for any of us to be out, leafy suburbs or not.

Some of us thought we’d grow old and die before the husk of a broken America would befall us. We are not so fortunate. It is now ours to have to deal with. Decades in the making. None are so ignorant to say they didn’t see this coming.

Rich time to take some profits. The next air pocket in the markets seems like it’ll be a great buying opportunity.

Let me put this in terms that my affluent readers can understand. When you go to trade in your mid-sized luxury sedan in five years, you may discover that an E-Class is going to cost you nearly as much as an S-Class would have run you previously. And it won’t be because of “regular” old “inflation.” It’ll be because you’re getting priced down the Mercedes line as a result of the dynamics described above. Before you know it, you’ll face the “terrifying” prospect of being a C-Class driver.

Actually, I’d like to understand that a lot more. How is it that Jeff Bezos sucking up all the money makes it harder for me to afford what my wife mistakenly call a ‘middle class lifestyle’ (family sized apartment in the center of a big city, a nice car, a second home in the countryside etc)?

You are not wrong, H. Those people at the bottom aren’t moving up these days, if they are moving at all. My cleaning lady has been out of work for six months, has five in her household including an infirmed brother who needs home care. She has health issues, only bare Medicaid and a meager bit of gig income. She faces eviction monthly. This is not right.

I don’t really sense inflation day to day, much the same as one doesn’t see a child change on a day-to-day basis. I do remember when my wife and I were just married and moving into our first apartment we went to the grocery and bought everything we needed to stock up and start out life for $75. That was good because my wife was only making $400/month and I was making $200 as a grad assistant. Fast forward 15 years, we both worked full time and we built our “dream house” during the early 80s recession. When we moved in we had $5k in the bank, a $75k mortgage, maybe $50k in house equity and the start bare start of our retirement funding. We could afford life then but we really needed to both work. Fast forward again to a few years ago. My late wife was then in a care facility slowly dying from Azlhemer’s at a cost per year of twice the best salary she ever earned in 30 years as a college instructor. Something had sure changed.

I saw someone ask in a blog comment how rich do you have to be to be rich? By some measures I can count myself in that group. I live the way I want and can’t spend all my income. Some say rich means you can buy anything you want, when you want. I can’t really do that though I did write a check for the house I live in and the car I drive. This house cost more roughly three times what our dream house cost in the early 80s. A while back I asked my private banker how much I would need in my relationship with the bank to get any regular attention. He said 10 mil would be an OK start but realistically to get serious attention I would probably need $50 mil. So if you want your banker to think you are rich something like 40 or 50 million would be rich enough for the local yokels but you still probably get much respect form the actual big boys. Funny thing is back when my wife and I were making $600-700 a month we could afford to live quite comfortably, go out, eat steak when we cared to, and even buy nice furniture, some of which I still have. So inflation and “rich” are relative terms to a great extent. I will say our first car was the original Cougar and it cost us about $2500 new. My current car is a luxury SUV, best car I’ve ever owned, and it cost 25 times as much as that first one. That really does feel like inflation. On the other hand my current computer is at least 100 times more powerful than my first one and cost about half as much so…