Name something more potentially dangerous than “a large, fundamentals-agnostic, owner of equities.”

Go ahead, I’ll wait.

I’m just kidding. There are certainly more dangerous things in the world than systematic investor cohorts, but over the past several years, market participants have become apprised of the extent to which volatility-sensitive strategies controlling hundreds of billions in AUM can wreak havoc when something goes awry.

As Nomura’s Charlie McElligott is fond of reminding folks, “volatility is your exposure toggle.” During tumultuous periods, spikes in volatility dictate unemotional, mechanical de-leveraging from a hodgepodge of investor types. That automatic (or semi-automatic) reduction in exposure can (and will) drive volatility higher still, especially considering the tendency for market depth to deteriorate during a panic. That’s the dreaded “liquidity-volatility-flows” feedback loop, and it’s a fixture of modern markets.

In a note out this week, Goldman’s Rocky Fishman took a look at the impact of managed vol funds during the pandemic.

“Among systematic macro investors, managed vol funds are large,” Fishman wrote. His analysis took account of some $200 billion in AUM, for example.

Underscoring the dynamics mentioned above (and documented in these pages ad nauseam over the past several years), Fishman wrote that this universe of investors is important to take account of because “vol itself is the key input to their asset allocation decisions.”

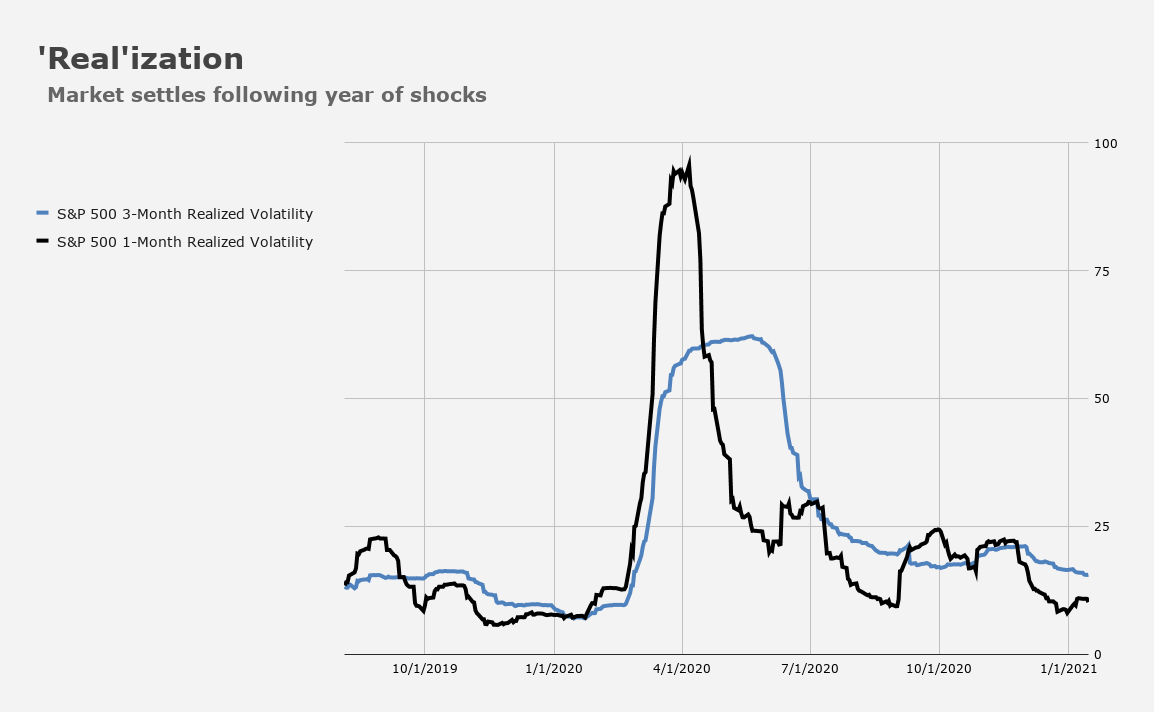

On his estimates, managed vol funds shed more than $60 billion of equity risk during the most acute months of the panic, reducing their exposure from 75% to just 33% in a single quarter.

That likely accelerated the rout, driving up volatility further and thus necessitating more selling, in a highly absurd carousel made worse by lackluster liquidity. Remember: Market depth never recovered from the shock of February 2018, when the VIX ETN complex imploded.

The key point — and this cannot be emphasized enough — is that this was mechanical. “The funds did not generally sell equities in the pandemic’s first months because of worries about the economic impact of the coronavirus spread,” Fishman wrote. “They sold aggressively because equity market volatility was rising.”

And therein lies the problem for the “rest of us,” so to speak. Once things get moving in the wrong direction, it’s a domino effect. Volatility rises; vol-sensitive strats dial down their exposure; prices drop through key levels, triggering selling by other breeds of systematic investors; market depth deteriorates; volatility rises further; and around we go.

Fishman emphasized that these funds are not a monolith.

While “every fund” in Goldman’s sample trimmed equity holdings over the course of Q1 2020, Fishman noted that “the cuts went beyond what share prices erosion would have created.” He also documented some of the differences across funds in the sample.

“Most funds created or added to short futures positions, some funds had already returned to full equity allocations at the end of Q2 impl[ying] they have high volatility targets [while] some funds were continuing to de-allocate during Q2 [suggesting] the duration of high volatility potentially led some funds to continue de-risking,” he remarked.

The figure (above, from Goldman) suggests heterogeneity among funds, even as the overarching message (that vol is the toggle) is constant.

That point (heterogeneity within funds that are nevertheless amenable to group treatment) underscores the somewhat elusive nature of what, exactly, they’re “managing” and “targeting.” This isn’t a new revelation, but it’s worth reiterating. As Fishman put it, “the question of what ‘vol’ (implied vs realized, near-term vs long-term, US vs global) the funds are managing itself has various answers that vary from fund to fund.”

As you can see from both figures above, funds have re-allocated — and fast. That probably accelerated the speed of stocks’ recovery.

“Even with vol quite high in September, the drop from the peak was enough for managed vol funds to return to 62% long equities at the end of Q3, helping to fuel the strong global equity rally,” Fishman said.

It doesn’t take a leap of logic to surmise that whatever gas was left in the tank in terms of re-allocating was at least partially used up in Q4, considering the steady grind lower in realized, even as implied remained elevated versus where it arguably “should” be.

Indeed, the latent bid from vol-sensitive strategies as realized moved lower (especially following the election) was part of several year-end melt-up calls, some of which ultimately proved correct.

The key takeaway from Goldman’s postmortem (and, unfortunately, “postmortem” can be taken both figuratively and literally in the context of 2020), is that the self-feeding loop discussed so often in these pages long before the pandemic, is a crucial component of markets with the potential to drive outcomes in true “tail wagging the dog” fashion.

Fishman didn’t mince words in that regard, although he didn’t strike an alarmist tone either.

“A byproduct of managed volatility funds’ use of market volatility as an input… is that it helps drive faster changes in equity market conditions than shifting fundamentals alone would indicate, in our view,” he said, in the same note, adding that “like option-driven flows (gamma), and levered and inverse ETFs, the presence of a large base of managed volatility funds creates a self-reinforcing loop in volatility that has the potential to alter the path of equity markets.”

Again: The tail often wags the dog. And that dynamic becomes especially acute when a tail risk comes calling.

So maybe fear itself isn’t the only thing to fear, but it’s one of the big ones.

This was quite enlightening. Thx H