One of the many unfortunate side effects of this week’s drama on Capitol Hill was the extent to which it effectively relegated the results of the Georgia runoffs to somewhere below the bottom of the fold.

And that’s really saying something. After all, the runoffs flipped the Senate, resulting in a unified Democratic Washington. At the same time, those elections were historic in their own right. Raphael Warnock became the first African American senator from the state, and Jon Ossoff the youngest senator elected in some four decades.

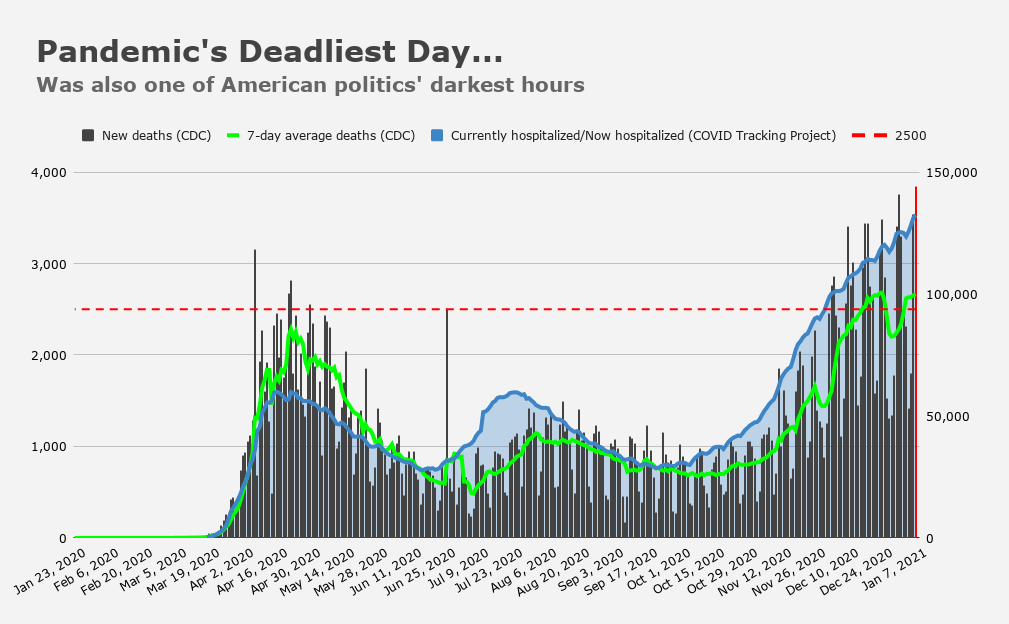

In other words: On any other day, Georgia’s Senate races would have dominated the headlines. But not on a day that featured the first armed insurrection against the US government in 160 years.

Markets being markets, equities and rates took the opposite approach of the media. Asset prices focused on the read-through from the runoffs, and the verdict was clear: Yields needed to reset higher and stocks will enjoy whatever benefits can be expected to accrue from a unified Congress receptive to policy coordination between Janet Yellen and Jerome Powell.

Democrats’ victory prompted analysts to reconsider forecasts on a number of fronts. Goldman, for example, tweaked their projections for the US economy across the board.

“With control of the House, Senate, and White House, we expect Democrats to pass further fiscal stimulus totaling about $750 billion,” the bank said, breaking things down as shown in the figure (below).

As far as the timeline, the bank expects a new bill to pass as early as mid-February.

Quite obviously, more stimulus payments will boost disposable income, although when it comes to the economically beleaguered, I tend to think “disposable” is something of a misnomer.

The figure below, from Goldman, shows a big spike in the bank’s forecast for DPI in the first quarter. That “reflects both the recently-passed $900 billion package… as well as the further $750 billion package that we expect,” the bank remarked.

And yet, Goldman doubts the immediate impact of that jump will be as dramatic as it was following the passage of the CARES Act.

Why? Well, because, as you may have noticed, the virus isn’t yet “tired of winning,” so to speak.

Goldman cited the slower-than-hoped-for rollout of vaccines and the more transmissible variant of COVID in cautioning that “state restrictions to control the virus will probably remain tight in Q1, and many households are likely to continue to cautiously avoid high-contact consumer services.”

In that context, the outlook for consumer spending isn’t as robust as it might otherwise be considering the expected boost to DPI — or at least not initially.

For Goldman, the effects of the stimulus will likely be back-loaded. While announcing a “large upgrade” to their GDP forecast, the bank said “much of it only appears in the second half of the year.” The idea, in essence, is that the personal savings rate will surge in the first quarter, and that will eventually be spent into the economy on a lag once it’s safer to engage in economic activity.

Ultimately, the bank’s forecasts for the world’s largest economy are now “even further above consensus,” as they put it. Specifically, Goldman sees quarterly annualized GDP growth of “+5% / +9% / +7.5% / +5% in 2021Q1-Q4, versus our previous expectation of +5% / +8.5% / +5% / +4%.”

Consistent with the thesis briefly summarized above, the bank said it’s reasonable to expect “a boom in consumer services spending as virus fears diminish” in Q2 and Q3, when accumulated savings from new stimulus will be unleashed into a services-driven economy which, thanks to vaccine rollout, will be a much safer place.

And what of tax hikes? Aren’t they coming? And won’t they offset demand-side stimulus?

Yes and no, respectively.

As the bank explained, in straightforward terms, “we expect Democrats to eventually pass tax increases for 2022 and beyond [but] because [they] would be focused on corporations and high-income households, these tax and spending increases should net out as modestly positive for GDP.”

Of course, all of this is likely to mean a more rapid drop in the unemployment rate and a quicker pickup in inflation. That, in turn, means the normalization of Fed policy could be brought forward.

This underscores a point I’ve attempted (with varying degrees of success) to communicate over the past couple of years. It is very difficult to simultaneously argue against fiscal stimulus and for Fed normalization.

And yet, that’s what you get when you peruse some corners of the financial blogosphere. You get calls for fiscal rectitude, austerity, and simultaneously tighter monetary policy. That is a recipe for misery coming out of a recession. In fact, it’s a recipe for staying in a recession.

Fortunately, Georgia voters decided (narrowly) that the country should go in a different direction.

In short, Goldman economists believe the economy follows “liberal” principles…