A modicum of stability was restored Thursday following the melee on Capitol Hill, where legions of Donald Trump’s disciples briefly “occupied” Congress Wednesday.

It marked a fitting end to a dubious presidency — a disorganized, motley crew of supporters, indoctrinated by years of tacky, Trump-branded propaganda, wandering the halls of a building adorned with portraits of people they didn’t recognize.

Just hours later, lawmakers returned to the very same chambers to certify Joe Biden’s Electoral College victory.

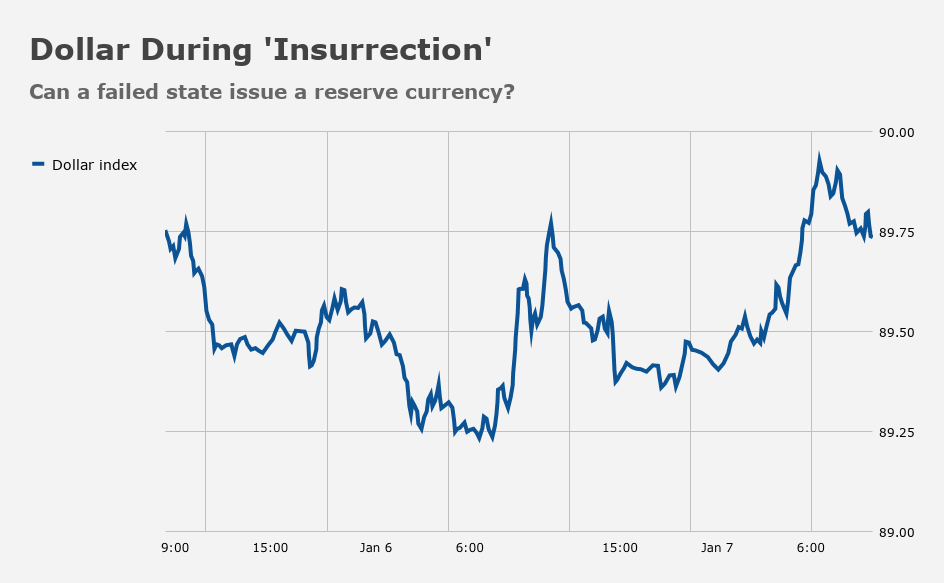

As Bloomberg wrote, “despite the disruption, markets showed little sign of worry and trading throughout the Asia day was normal.”

That snippet of boilerplate copy speaks to an important point, albeit accidentally. No living person knows how the world would react in the event America descended into domestic discord.

Obviously, there have been periods of extreme internal strife since the Civil War, but almost without exception, those movements played out under the banner of social justice or were otherwise aimed at compelling government to address a grievance, legitimate or not.

Consistent with this tradition, Trump and his allies have insisted that their movement is based on a grievance — namely, election fraud.

But the idea of a “stolen election” is beginning to seem more and more like a red herring. The truth may simply be that millions of Americans and a disconcertingly large number of lawmakers in the US, are now willing to countenance some form of autocratic governance.

In itself (i.e., forgetting for a moment about the fact that historically, autocratic rule is conducive to all manner of suffering and human rights abuses) that doesn’t have to be problematic. There’s nothing written in stone that says autocratic states will everywhere and always be abject failures.

As I (gently) noted last week, Putin’s Russia isn’t an abject failure. Erdogan’s Turkey isn’t an abject failure, either. And, quite obviously, Xi’s China isn’t “failing” (unless you mean on the human rights front, in which case, yes, Xi is venturing into darker and darker waters every, single day).

In order to get to autocracy, though, you have to do away with democracy first. Based on the results of November’s election, and adding an arbitrarily defined “adjustment factor” to account for the number of Trump voters who probably defected on Wednesday, there are around 80 million Americans who want democracy and around 50 million who would be fine with some kind of autocratic rule, likely of the “soft” variety.

That split means that for America to get to autocracy, there would have to be mass internal conflict.

For the rest of the world, and, far more narrowly, for market participants, the prospect of mass internal conflict in America isn’t tenable.

America issues the world’s reserve currency. It also issues (“sells”) an interest-bearing version of that currency (i.e., Treasurys), which serves not only as the collateral that greases the wheels of finance, but also as the key global vehicle for recycled savings. Anything that raises existential questions about those two things (the dollar and its interest-bearing counterpart) would be highly destabilizing to the rest of the world.

Crucially, existential questions about the dollar and Treasurys are something wholly different from the questions we often ask related to deficits, debt burdens, and trade balances. In a real insurrection that succeeds, or in a situation where a US president commandeers the government by force, the world would be compelled to immediately rethink whether Treasurys are desirable collateral. After that, the same shellshocked world would need to ponder whether global trade and commerce should still be settled primarily in dollars.

If you’re looking for a dollar collapse narrative, there’s one that makes sense. Forget hyperinflation. Forget “money printing.” Forget the dreaded “twin deficit.” Think more existential.

In that context, it’s notable that global equities held up Thursday and perhaps even more so that the dollar took its cues from rising Treasury yields and the comforting prospect of new management in the besieged American capital.

You might argue that the “new management” component compensates for the “besieged capital” problem — after all, the capital wouldn’t have been besieged were it not for current management. Still, this is a discussion that’s now at least worth having. It’s no longer science fiction.

“USD is slightly firmer in generally calm markets, despite the extraordinary scenes on Capitol Hill,” RBC said Thursday, somewhat incredulously.

An LA Times piece published Wednesday afternoon carried this headline: “In America’s capital, a day of images from a failed state: our own.”

“What we witnessed on social media and TV news is what we in the United States usually frame as the kind of political crisis that happens someplace else, but if you’re from a country that’s fallen to fascism, have family from places where coups are part of recent history or know someone who’s lived through the fall of a government at the hands of paramilitary forces or a military junta, you likely saw this coming,” the Times wrote. “Stoking division for personal gain has consequences, even in America.”

“I doubt even the writers for House of Cards would have come up with the events that transpired yesterday,” Rabobank’s Bas van Geffen said.

“With Washington D.C. in such disarray it must surely [be] a risk-off day right? Wrong!”, van Geffen went on to exclaim, noting that while “the rationalization… is a focus on the longer term, that does require that there’s still a country left for [Biden] to govern.”

That underscores the sentiment expressed earlier this week by Ian Bremmer. “A superpower torn down the middle cannot return to business as usual,” he wrote, adding that “when the most powerful country is so divided, everybody has a problem.”

Well, “everybody” other than investors, apparently. They’ll be fine. Right up until a “mob” breaches the Eccles Building. That’s when things get serious.

Thank god congress went back to formal business as quickly as possible.

Normalicy and a Big Military. Both are fleeting

yeah it might have been different this morning in the markets had congress evacuated and all gone home.

I wonder to what degree the breach of Capitol security sapped the will of the House reps who’d planned to let the confirmation drag on for hours or days. To that end, POTUS’ gambit backfired horribly.

Congress’ sharp rebuke of mob rule — we’re convening and getting this done TONIGHT — was an encouraging sign, and yes, I’m sure it helped define the market response overnight and this morning!

Big Business usually finds ways to accommodate itself with fascism/autocracy. Yes, autocrats/fascists can be a bit annoying with their pet peeves and whatnot but they are usually very into the status-quo, which, by definition, is pretty good for Big Business.

Of course, TWTR and FB would have to fall on their knees and beg for forgiveness and twist their algos to make sure a particular segment of the population is the only one allowed to speak freely but, hey, advertising dollars would still keep rolling in. And, ultimately, as investors, that’s the only thing we care about…

As well, not to be scoffed at any longer, is capital flight by American’s with capital, the fortunate few, out of the US and into other jurisdictions. Out of the US system. As a diversifier. From a risk management perspective. While the option is still available.

Such an event that could lead many to take this pause is still over the horizon. Our historical trajectory is not going to include a V-bounce return of our institutions. We’ve been warned.

So, a follow on question. When are our intellectuals and artists going to start being arrested? Will it be tech executives instead? What countries will they flee to when this starts? Seems like Spanish would be a good language to start learning.

I try not to let my mind go there and then I remember some of history’s lessons for those who choose to look away and then I’m looking for something powerful to ease the anxiety.

Big business can always find accommodation with fascism, by definition. The investor part of me is fine with it,too. The human part of me is revolted, and it comes first.

This is a thought provoking post… ! I immediately wound up in a schematic mode when seeing yesterday’s scenario… I am very certain the financial and political establishment were back to back protecting against a dismayed public who is /was not enamoured with either of these institutions irregardless of status in their respective lives .. Like a tree with a branch having been cut off a protective sap exuded in an attempt to protect and hopefully to heal …. Hopefully..!!? Interesting to watch the cast of characters and their respective actions…

We are focusing on the impact of autocrats on business. Can be good, as in Singapore.

But aren’t we talking about something else here? Shouldn’t we be looking at how business does when there is a populist regime? The right points to Venezuela as an example of socialism run wild. But isn’t it, at heart, a populist regime?

Or even some of Trump’s measures on immigration and drug pricing. They were popular but not great for many businesses.

Populism is not always business-friendly.

Fair point but in the US/via the GOP, it’s going to be right wing populism. It still isn’t going to be a universal good for businesses but, generally, you cannot count on such people for reversing societies’ established hierarchies.

It would be a very brave person who relied on such people for anything. Unpredictability and fickleness are that you can guarantee, and once they trash the rule of law you have no recourse. As Jack Ma has been taught.

Perhaps investors are increasingly realizing that the “risk-free” component of CAPM that underpins the entire immaculate theoretical castle of financial theory, and serves as the pristine collateral for the global financial system, is not so free of risk. The theories haven’t ever survived major instability, let alone a world war. They’ve also already, I would argue, been subordinated by a new regime that is, in substance not name, an implicit-to-explicit nationalization of most developed world economies. That Rubicon was crossed, and it seems there is no going back. That is the lesson of 2020, I believe. And that is why this bubble is different. It will now take sovereign defaults/collapses for it to truly pop. I suspect most of the theorists will hold on to the bitter end to defend their life’s work and twist it to fit the new realities, essentially a form of reductionism and a category error. They need new theories. This is the Karl Popper dynamic at play – and endless cycle of conjecture and refutation.

The symbolic significance of yesterday cannot be overstated, I think. The images shattered a symbol of authority, and of many, many other things, including the stability of the entire geopolitical world order. Like broken glass, it has been forever altered, and it isn’t possible to just glue it back together without credibly transformative change. If you don’t appreciate the power of images, think of how dramatically the US reshaped the world after 9-11, the ramifications of which continue on an on to this day particularly in our surveilled reality.

On a technical point, the risk free model, even in a collapsing economy, still holds. The bond is a guarantee by the owner of the printing press that you’ll get a bit more printed money after you delay your right to receive services or assets.

What it can’t capture by construction is the risk that you may no longer want to hold that money. But even then, you could treat the potentially undesired currency as a risky asset and some other unit of value storage as the reference currency with zero risk free return.