Earlier this week, I had a little fun at the expense of the latest musings from Jeremy Grantham, who’s convinced US equities are in the midst of a historic bubble that’s doomed to burst in spectacular fashion.

I’m never sure what kind of reception those types of pieces will get.

While readers with a sense of humor enjoy the overt sarcasm (some revel in it), others invariably take umbrage when I poke fun at “brand names” and “legends” of the business.

Read more: Jeremy Grantham Regales Youngins With ‘Real Humdinger’ Of A Bubble Story

To me, that seems a bit backwards in the context of how willing people are to deride “regular” folks, like, say, an equity analyst at a given sellside firm.

Most random analysts aren’t rigging Libor or fixing the precious metals market, they’re just people like everybody else, and yet they’re habitually cast as villains by the financial blogosphere and especially by “finance Twitter,” which is really just a nightmarish collection of sock puppets I now refuse to engage with in any fashion.

The point is: Just because you’re a billionaire or because your name is enshrined in the investing hall of fame, doesn’t mean you’re somehow exempt from humorous takes on the opinion pieces you choose to make available to the public.

On the flip side, analysts who are just doing their jobs by delivering, for example, a price target for the S&P in a given year, probably should be exempt from unfounded allegations of malfeasance emanating from a peanut gallery that can’t seem to wrap its head around the notion that not everyone who works at a Wall Street bank is a monocle-wearing cartoon villain who spends the day pillaging the poor.

Anyway, I bring this up because there’s one sellside analyst who is immune to criticism from that peanut gallery, mostly because his contrarian takes resonate (loudly) with the wild world of bearish netizens.

SocGen’s Albert Edwards is something of a cult hero amongst the contrarian crowd, but unlike other heroes from that universe, he’s actually been right about some things over the years. That, in turn, means he’s retained some credibility.

Specifically, he’s been right about deflation (or at least about disinflation), and that’s translated into being routinely right about bonds, and mostly right about the trajectory of the global macro environment, even if his sometimes tongue-in-cheek calls for the apocalypse haven’t always panned out.

Although I’ve never discussed this directly with him (I hope to one day, though), the problem as I see it, is that in a world where social media allows for the rapid and rampant dissemination of hyperbolic quotables, his prescient deflation calls and nuanced macro takes are habitually lost in the shuffle because the doomsday crowd tends to tout the punchlines from his missives, without alluding to any of the nuance or the self-deprecating humor or the sometimes tongue-in-cheek character of those same punchlines.

So, instead of “Albert Edwards, man whose deflation concerns proved prescient,” we have “Albert Edwards, stock ‘perma-bear’.” That’s unfortunate, in my eyes anyway, because the former characterization is far more accurate than the latter, and yet the latter is what gets all the attention.

Well, pulling this all together, Edwards was out Thursday with his first note of 2021, and he cited the same Jeremy Grantham piece that I lampooned on Monday. Of course, Albert loves it.

“I think one of the most important points that Grantham makes is that, ‘this bubble will burst in due time no matter how hard the Fed tries to support it, with consequent damaging effects on the economy,'” Edwards wrote, adding that “this is where the overwhelming majority of market participants disagree with we veteran equity bears who have seen bubble after bubble burst first hand.”

For the record, I’m no Methuselah, and I don’t claim to have been around for every burst bubble, but I’ve been alive long enough to see multiple spectacular busts. And, as I tried to make clear in my humorous piece on Grantham’s latest musings, I have by no means attempted to suggest that the current conjuncture shouldn’t be classified as a bubble. It probably should.

Rather, my point has consistently been that if you can’t time the damn thing (where “the damn thing” is just “the top”), then waxing hysterical about it doesn’t do anybody much good. By contrast, Michael Burry had a pretty good idea about when the housing bubble would burst. Was he early? Yes, but not “early” in the sense that we usually use the term in investing. Usually we get out (or get in, if you’re short) so early that we miss huge upside (or go broke burning premium waiting on the crash).

More importantly, Burry identified a quantifiable reason why the situation was unsustainable, and his argument wasn’t generally amenable to refutation. His was an exceedingly rare case when it was possible to say, with some degree of precision, when a bubble would burst and also explain, using numbers, why that prediction was virtually certain to pan out.

Clearly, the calculus here is different depending on what type of market participant you happen to be. If you’re a tactical investor (i.e., a trader) or you’re a hedge fund, then it is extremely relevant whether a heavy market is on the verge of collapsing under its own weight. If, on the other hand, you’re 22 years old, and you’re investing your first $10,000 in an index fund, it’s almost irrelevant, assuming you’re not prone to panic attacks.

For his part, Edwards says begrudging bulls (i.e., those who may think things are frothy but who are nevertheless sticking with it) are placing too much faith in the Fed.

“Even those who might agree that the stock market is a bubble remain bullish for one reason only: namely confidence that the Fed simply cannot allow this stock market bubble to burst due to the impact on the real economy,” he wrote Thursday, adding that,

They also buy the corollary that the Greenspan Put is alive and well and the Fed will not allow the bubble to burst. The incredible V-shaped recovery of the stock market in March last year has only further strengthened investors’ belief in the Fed.

As you can imagine, Albert isn’t buying that. Figuratively or literally.

“For people like Jeremy Grantham, Fred Hickey and myself, the idea that the Fed is omnipotent is bunk,” he went on to chide. “Sure, they can kick the can down the road for a long while but eventually that can will hit a brick wall to rebound and hit them right back in their faces,” he added, employing some of his signature balderdash.

One worry is, of course, rising yields. Most readers are familiar with this concern by now. Equities trading at dot-com multiples will struggle if yields rise too far, too fast, and the 10-year broke through 1% Wednesday after Democrats swept the Georgia runoffs.

1% doesn’t sound like much (and it’s not), but you have to consider the context. It’s all relative, and, as Goldman has repeatedly emphasized, it’s not always about the absolute level. Sometimes, it’s about the rapidity of rate rise.

When you throw in the distinct possibility that a Democratic Congress could push through more stimulus, triggering more Treasury supply, you’re left with a bearish catalyst for bonds, and that will be more acute if stimulus actually works.

With that in mind, think about the read-through for the Fed. While the “new” average inflation targeting regime does mean policymakers will tolerate overshoots, it doesn’t mean they won’t ever hike again no matter what.

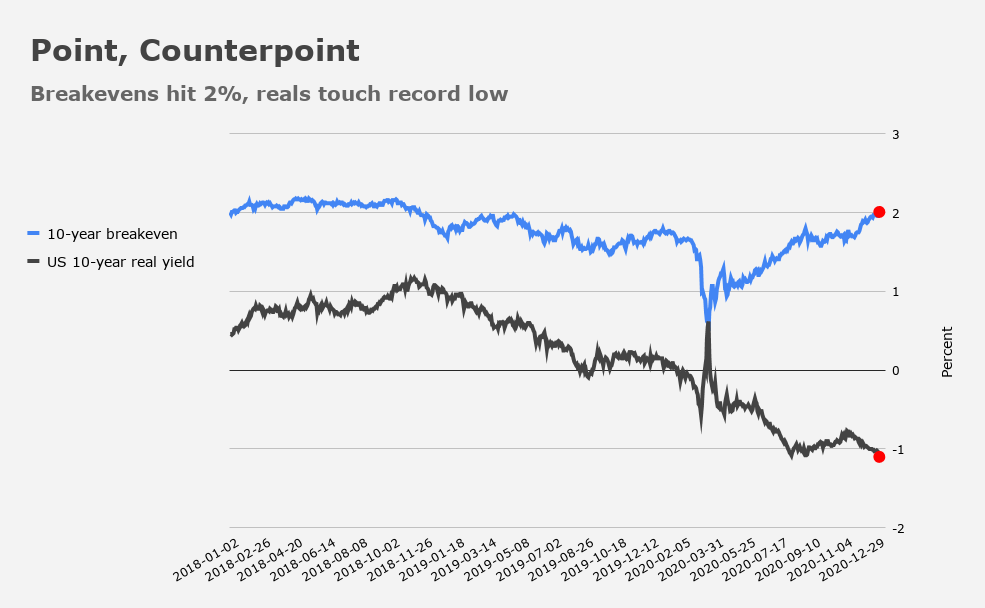

Of course, it’s also true that so far, the Fed has managed to engineer a picture perfect “X-ray,” if you will. Real yields have tumbled deeply into negative territory while breakevens, a referendum on the Fed’s reflation success, have risen in lockstep with stocks.

Equities are (more than) happy to tolerate modestly higher yields if it’s driven by breakevens, as that generally means economic prospects are improving — or at least in the mind of market participants.

Still, past a certain point, the composition won’t matter. And common sense suggests that if stocks couldn’t stomach 3.2% (nominals) on 10s back in October of 2018, the threshold is probably quite a bit lower now, given expanding multiples. Edwards underscores this.

“We all understood in 2018 (and we still know now) just how dependent this equity bull market is on low bond yields, especially in recent years with the ‘Growth’ and FAANG stocks leading the market higher,” he wrote Thursday, adding that,

“But back then, with the S&P just shy of 3,000 and much more moderate multiples than today it took a rise in 10y bond yields above 3% to ‘break’ the bull run. Now with the US tech sector on a forward PE close to 30x (vs 20x back in Q4 2018, see chart below), it will clearly take a lot less to break the equity market and trigger the bursting of this bubble. But what is that ‘danger level’ of bond yields?

He goes on to cite a former colleague who suggested that when you take a look at projections for Treasury supply going forward, real yields will need to rise in order to attract private capital away from assets where that capital is actually generating some semblance of income.

If equities trading at current valuations would have trouble digesting sharply higher nominals no matter what’s driving them, stocks will absolutely cringe at a sharp move higher in reals, which, incidentally, would likely also trigger dollar strength, in true “insult to injury” fashion (for risk assets.)

There’s considerably more to Edwards’s latest, but at 1,600 words, I think I’ve probably carried on long enough. Albert sums things up as only he can.

“In any case, I don’t believe there is a cat in hell’s chance that the Fed can tighten and/or that US 10-year yields can rise to 1½%,” he wrote. “The equity market bubble will burst long before we get there!”

The exclamation point is, of course, in the original.

What is preventing the Fed from implementing yield curve control to avoid the necessity of raising rates?

Good point, I don’t think anything will prevent the Fed from implementing YCC, to me it’s more a question of whether they’ll do that proactively trying to get ahead of major market indigestion or whether YCC arrives as a reaction to a mini (or not so mini) burst of the bubble.

Obviously, SocGen does not hire SocPuppets. Edwards’s analysis confirms my views, which are grounded in unverifiable hunch. It’s been a nice little ride since April, but at age 77 I’ll feel better trimming equities soon. Before Jan 20…

TSLA stock and half the SPAC mergers are all bubbles, but it is hard to see what can pop it.

Perhaps VW or Apple or another auto manufacturer putting up some real competition in the EV space would do it. A general and widespread stock market sell-off would also do it. It’s hard to see either of those two happening anytime soon.

Like Heisenberg said above, timing is everything and if you can’t time it you’ve got nothing.

One of the key advantages that Musk has is the ability to raise capital. He can sell 5 billion of stock with the snap of his fingers and it doesn’t budge the stock price at all.

Michael Burry did have the brilliant insight to see how a thing must fail.

Incidentally, Burry is now short TSLA.

Burry also buys into conspiracy theories like that yesterday was a false flag Antifa operation. He’s a savant of some sort, but he’s also not quite right in the head about plenty.

What is the BOA Michael Hartnett bull bear at? Are you approaching 7 or 8 yet or already getting ahead of that?

H

You are the only market expert to whom I pay real money to listen to what you have to say. One reason for this is that you understand and explain what is actually going on in the huge portion of the market “iceberg” that lives under the waterline better than any one else with whom I am familiar. The other reason is that you have access to a large group of leading market experts of all different stripes and regularly pass their observations and wisdom onto us, along with the synthesis of their ideas otherwise not included in the notes of others in the blogsphere. Synthesis is is a form of logical thinking foreign to most ordinary humans and I am happy to pay for access to your extraordinary skill in that arena. Thank you for sharing. Stay safe in 2021 and keep up the good work. I have a feeling this will be a wild ride. My primary advisor has a tool that stress tests each of my holdings for four scenarios I select. The results from a test run for me just after the election showed me I ‘m doing OK but to weather the ride for this year I may have a fair bit tweaking to do. Your commentaries will be an important input to this process.

Danger is TSLA. IV percentile @ 85% and $800B cap vs IV percentile of 37% of AAPL’s $2200B cap.

Means TSLA trades LARGE in market cap swing vs S&P biggest AAPL, AMZN (32% IV).