The Chinese economic recovery continued apace in August — or at least that’s the official story.

PMIs for the month held up well, and an upside surprise on the services gauge was especially welcome news Monday.

The “official” (i.e., NBS) non-manufacturing gauge printed 55.2 for the month, up from July and better than expectations. That sounds dry (and it is) but monthly activity data out of China has habitually disappointed on the retail sales front, suggesting a supply-driven recovery that may not be sustainable absent a more robust pickup in demand.

Despite the apparent stabilization of official PMIs in expansion territory, demand is still an issue, both domestically and abroad. “More than half of companies still list lack of demand as the main difficulty”, a Monday statement from China Logistics Information Center reads.

Additionally, there are burgeoning concerns about smaller companies. The small manufacturers PMI printed in contraction territory (again), and at least some commentators think that’s a bad omen for the ChiNext, which is riding one of its ridiculous runs, up some 50% in 2020, five times the gain on the Shanghai Composite.

Beijing recently loosened the rules around how much shares on the board are allowed to swing in any given session, a market-driven reform which, not surprisingly, produced massive gains for some debut offerings this month.

The index trades at almost 40X forward earnings, nearly triple the multiple for the CSI 300.

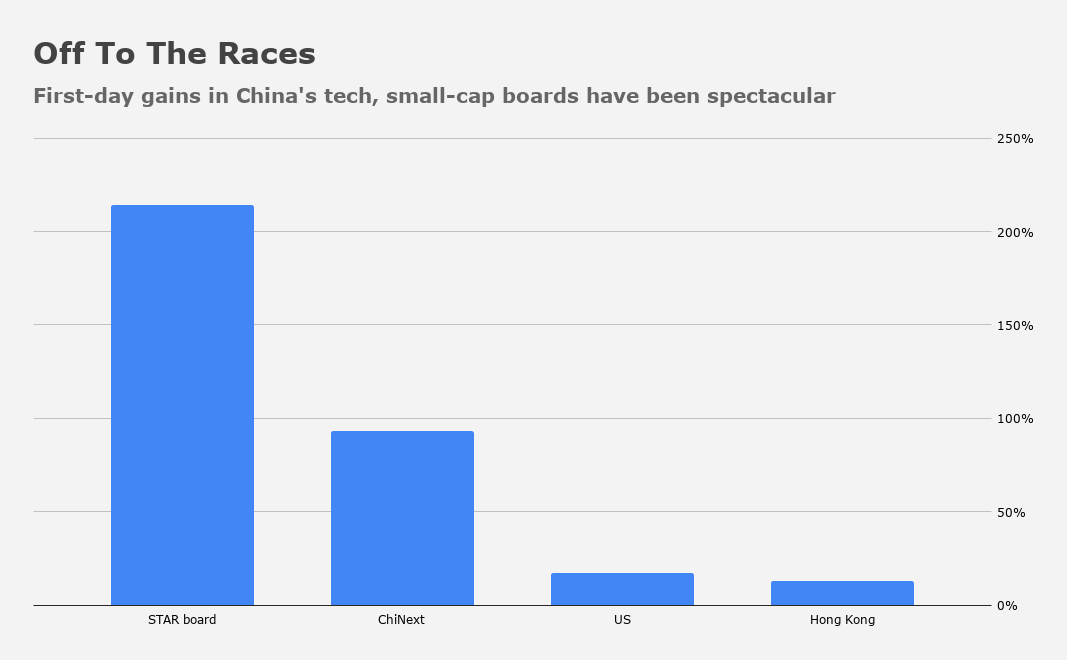

Including nearly two-dozen companies which went public on the ChiNext since relaxed rules went into effect earlier this month, new listings on the board this year have risen an average of 93% on their first day.

That pales in comparison to the already infamous “STAR” board, which turned one year old earlier this summer, but the new rules (which lifted daily price limits for IPOs during their first five days on the market, and doubled the band for existing listings) could well see it catch up.

These swings are, to a certain extent, a reflection of what happens when you reduce red tape and regulations in a market that is notoriously prone to retail investor-driven manias.

And yet, bubble risk aside, China is keen to create a friendly atmosphere for tech companies at a time when the administration in the US is cracking down on Chinese listings. The world’s two largest economies are embroiled in a tech war, and innovation requires capital.

Needless to say, Jack Ma’s gargantuan dual-listing (in Hong Kong and on the mainland) for Ant Group underscores the risk of shutting out Chinese firms from US capital markets.

Coming full circle, if equities do become totally detached from economic reality in China as a result of less regulation, I suppose we should celebrate a victory for capitalism — after all, that’s been a hugely successful model in America’s “thriving” capitalist system, which has never seen any sort of busts associated with lax regulations.