“The big surprise under a Democratic sweep would be a rally”, BofA’s Savita Subramanian wrote late last month, echoing the sentiments of many analysts who generally believe the knee-jerk reaction to a scenario that sees Republicans suffer heavy losses in November would be a risk-off move in equities.

In the same note, Subramanian characterizes a prospective Democratic sweep as not necessary “anathema” for stocks.

The accompanying analysis reflects Wall Street’s efforts to explain why stocks don’t seem to be perturbed by the rising odds of a less business-friendly climate in D.C. following the election. I highlight this in the context of a longer discussion around markets’ apathetic attitude towards unprecedented chaos in Washington.

Read more: Maybe We’re Already There (The ‘Story Out Of D.C.’)

In the linked post (above) I noted that analysts often resort to somewhat nebulous explanations to account for the disconnect between asset prices and the extremely fluid political climate.

For example, some models attempt to build in an earnings boost from less contentious foreign policy under a Joe Biden administration and/or from a normalization of domestic politics. I argued Sunday morning that while entirely plausible, you can’t quantify that boost ahead of time. What you can quantify, though, is the hit from higher corporate taxes.

“Nearly half of 2018’s whopping 23% S&P 500 EPS growth came from tax reform; we estimate reversing half of the benefit would be a mid-single digit hit to EPS”, BofA’s Subramanian said, in the same note mentioned above. She added the following:

Biden has also proposed 1) reducing the deductions for global intangible low-taxed income (GILTI) and 2) a 15% minimum tax on corporates with book profits >$100mn. We estimate the potential impacts to S&P 500 earnings from each in charts below. The overall tax hit to S&P earnings would likely be in the neighborhood of ~9%, where higher tax rate accounts for 6-7%, the higher GILTI tax ~2%, and the minimum tax ~1%.

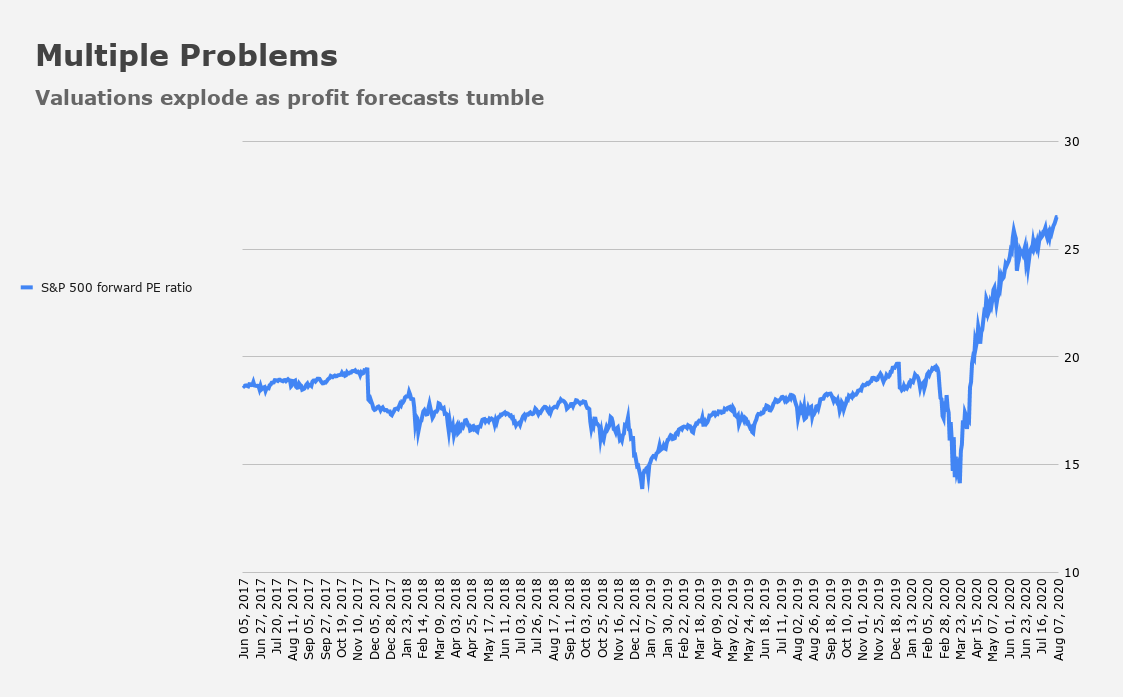

It’s hard to see how that’s priced in. For example, the S&P currently trades at around 21X consensus 2021 EPS ($165). And that’s assuming you believe earnings will basically recover to 2019 levels next year.

That forecast (a full recovery in earnings just a year on from the pandemic) at least implicitly assumes a widely-disseminated vaccine sometime in early 2021, the absence of a serious second wave, and minimal (or manageable) structural damage to the economy. If any one of those assumptions are violated, earnings could come up short next year.

When you toss in higher corporate taxes, you end up with even more ambiguity around the outlook. “We have previously estimated that Vice President Biden’s current plan, if fully enacted, could reduce our baseline 2021 EPS to $150 and our 2022 EPS could be closer to $170”, Goldman said last week, recapping previous research (more here).

But like virtually every other bank on the street, Goldman assumes that the combination of more stable politics and growth-friendly initiatives may offset some of the mechanical impact from the assumed tax hikes.

“The potential for changes in government policies outside of tax policy, such as fiscal spending, trade policy, and regulation, suggest a combination of upside and downside risks to earnings depending on the outcome of November’s elections”, the bank’s David Kostin remarked on Friday.

JPMorgan wrote last month that while “the consensus view is that a Democrat victory in November will be a negative for equities, we see this outcome as neutral to a slight positive”. The chart (below) is similar to the visual above, but uses JPMorgan’s figures and includes estimates for a deescalation of the trade conflict.

For her part, BofA’s Subramanian writes that Biden’s “Buy America” plan “could boost sales for domestic companies, and could further drive on-shoring efforts at multinational corporations and thus drive a pickup in US capex”.

Another boon to capex under a Biden administration could come from more predictable trade policy, even if Sino-US relations remain fraught (which they will).

“Biden’s trade tool of choice is to establish coalitions with other regions [and] under Biden, a ceasefire with the rest of the world could allay corporate reticence to commit capital to projects amid uncertainty about global relationships”, Subramanian went on to say, noting that “the capex guidance ratio peaked in late 2017, when trade tensions began escalating, and continued to decline throughout 2018 as guidance for planned spending fell amid uncertainty”.

In a separate analysis, Subramanian’s colleague Michelle Meyer reiterates the notion that less uncertainty on trade would help calm frayed C-suite nerves.

“The trade war with the rest of the world would likely only continue under Trump [so] a second term is likely to yield greater trade uncertainty and a bigger hit to corporate confidence than under a Biden Presidency”, Meyer says.

She also suggested last month that Biden’s programs aimed at improving the plight of the middle class could help offset the tax hikes. “Higher corporate and personal taxes under Biden can weigh on investment and spending [but] the emphasis on supporting the welfare of the middle class by offering greater access to education, job training, and lower student debt should offer longer-term benefits”, she said.

That is unequivocally true, and regular readers know I’ve repeatedly argued that putting more money in the pockets of those with the highest marginal propensity to consume is the surest way to bolster a consumption-driven economy over the longer-term. Indeed, that’s almost a tautology, even as it’s completely lost on supply-siders who, against all evidence, claim that handing windfalls to the folks who are least likely to spend, will somehow boost an economy which lives and dies by lower- and middle-class spending.

Subramanian offers a quick summary of many key points which together help make the case for why a Democratic sweep isn’t “anathema” (as she puts it) to equity gains:

But positives include the potential for unleashed capex amid less tariff uncertainty; “Buy America” is growth-positive; even hiking minimum wage and raising taxes of the wealthy could perversely benefit stocks, as discount retail is >6x luxury retail’s US public market cap. Moreover, the expected hit from environmental and social regulations is not clear-cut: Obama’s Energy sector outperformed Trump’s by over 15ppt, despite tighter regulations.

It goes without saying (or at least it will to most regular readers) that I’m sympathetic to, and supportive of, nearly all of the points made above.

However, from a cold, calculating perspective, one thing seems inescapable from my perspective: the majority of the potential pluses for stocks from a Democratic sweep will only be quantifiable in real-time, or in hindsight. By contrast, many of the negatives for equities in a Democratic sweep scenario are quantifiable now.

When you toss in existing, COVID-related uncertainty around the trajectory of the rebound in corporate profits, one is left with the distinct impression that SPX ~3,380 represents an equity market that is laughably unprepared for a Democratic victory.

That, I argued over the weekend, suggests that no matter what betting markets say, and no matter what any individual investors or analysts might claim about the odds of Republicans losing across the board, the market as a whole isn’t buying it.

“All in all, gridlock may be best for stocks (and so says history)”, BofA suggests, positing “a cessation of tariffs, some stimulus from bipartisan COVID support and no corporate tax change”.

Gridlock is already here. And it’s already been “best for stocks”, so to speak. If certainly not for the American people.

The first reaction to a Democratic sweep may well be a relief rally. Relief about the increased potential for an unfraught transition of power as well as the expectation for a more stable and predictable political and economic climate.

In subsequent months markets may well drift lower as Democratic plans regarding taxes and economic priorities crystallize into actual policies.

Policies and legislation.

Seems like the best outcome would be a Biden victory with GOP maintaining control of the Senate. Not sure what probability the betting markets are assigning to this particular scenario (…quite low, I’m guessing, since there’s been so little discussion of this outcome).

Right now Predictit has Biden at about a 62% chance, and a Democratic Sweep at about 52%, so the ballpark chance based on betting markets of a Biden win and Republican Control of at least one house of Congress is in the 10% range. 538 has Biden at 72%, and I don’t see a Senate Forecast there,- maybe someone else has some input on that… but with the higher odds for Biden at 538 I wouldn’t be surprised if the chance of split government in the event of a Biden win are a little higher based on their methodology. I’d guess about one in six.

Let’s say the market is (and has been) pricing in a P/E ration of 22 to 30– and no lower — due to the belief that if the P/E ratio were to move to let’s say a plebeian (and historical average level) of 16, the Feds would do what Japan is doing: buy equity ETFs. There is not much talk about this as an overriding possibility.

In the case that this premise holds, the markets could care less who is in office; what trade wars exist or continue; whether there exists a vaccine for Covid-19 epidemic or not; whether 100K, 200K or 400K die from Covid-19; whether 10 million or 40 million lose their jobs permanently; and whether the nearly 250 year test of democracy is being abraded at the edges. Nope. The only thing that matters is if there is a “greater fool [the Feds] than I” to buy equities at a greater price. That seems to be the case that makes the most sense to me. The Feds have made an implicit promise and the market expects it to keep it.

I am pretty sure when they say “gridlock may be best for stocks” then mean “gridlock with a Biden presidency may be best for stocks”…

The stock market soared under Bill Clinton and did fine under Barack Obama after Republicans blew the economy up. It will do fine under Biden and a Democratically controlled Congress. Indeed, if they manage to pass legislation that actually reduces inequality — and, yes, that means higher marginal and capital gains rates — it could go much higher. (And Grover Norquist can finally move to Brazil.)

There is an argument that renewable technologies having suffered (if that is the correct word when in fact booming) under Trump will propel a nationwide boom upon a Democratic sweep.