Headed into the new week, the S&P 500 hadn’t seen a losing session since July 30.

Emboldened by a determined Fed and encouraged by corporate earnings which, on the whole, came in better than feared, investors pushed the US benchmark higher for six consecutive sessions to within 1% of its all-time peak. The Nasdaq 100, despite Friday’s stumble, will be looking for a third straight weekly gain, having long ago erased the entirety of its pandemic plunge to reclaim record highs.

You’d be forgiven for thinking the easy money has already been made. It’s still unclear how investors will judge Donald Trump’s decision to take unilateral action after stimulus talks collapsed, and geopolitical tensions are running higher than ever ahead of trade discussions between the US and China. Taiwan welcomed Health and Human Services Secretary Alex Azar on Sunday, marking the highest-level visit by a US official in decades, much to Beijing’s chagrin.

Trump’s executive orders targeting TikTok and WeChat raised eyebrows late last week, as did sanctions against a handful of high-level officials including Carrie Lam. The yuan fell the most in two weeks Friday, but remains near the strongest levels since March (figure above).

China reports July activity data this week, which will be watched closely for signs that domestic demand is picking up alongside industrial output.

Retail sales, CPI, industrial production, and the first read on August consumer sentiment are on the data docket stateside, as well as jobless claims, which continue to command attention.

“Initial claims is once again experiencing a renaissance of relevance as investors search for a clearer understanding of the direction of hiring as the pandemic has settled in for a much longer duration than early optimists anticipated”, BMO’s Ian Lyngen notes, adding that “the dated nature of the NFP/UNR data has lessened the impact on the US rates market are we’re therefore assuming that anxieties linked to a second jobs downturn have rolled forward, leaving proxies once again potentially market moving”.

Initial claims fell to the lowest of the pandemic last week, and continuing claims declined as well, but the numbers are still unfathomably high outside of the current context.

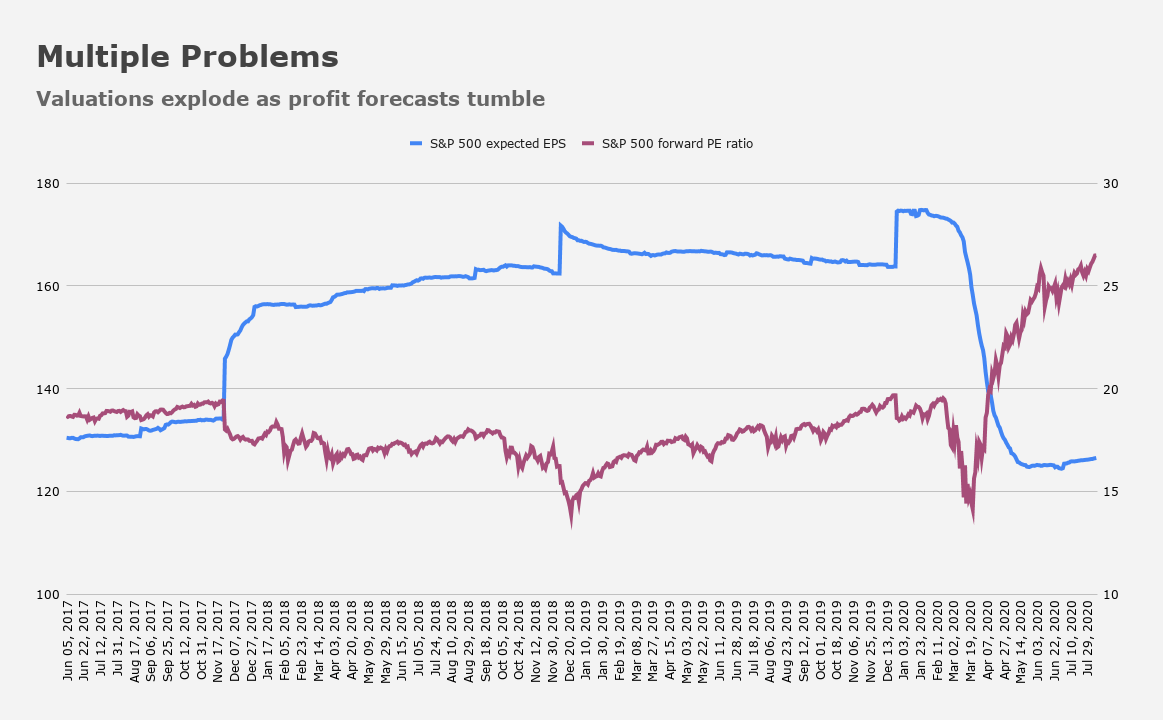

Speaking of “unfathomably high”, there’s still quite a bit of angst around valuations, which are stretched to levels last seen during the dot-com bubble.

When profit expectations suddenly collapse and equities manage to surge ~50% off the lows in just four months, you end up with a forward multiple that, for some market participants, is extremely uncomfortable.

It’s starting to occur to more and more investors that the Nasdaq’s inexorable rally might be telling us something disconcerting about the future. “A slightly scarier theory exists as to how the value of companies in the Nasdaq 100 has expanded by $2.9 trillion in this of all years”, Bloomberg’s Vildana Hajric wrote Saturday. “It’s that the COVID-19 crisis’s impact, or at least the social-distancing strictures it has forced upon the world, will prove to be permanent”.

With all due respect to Hajric (whose piece is well worth a read), that is not a “theory” (although it is “slightly scary”). Rather, it is a fact. That is, there is no question that mega-cap tech’s performance in this virus-blighted environment is attributable (at least in part) to the notion that consumer habits and, indeed, the way we live our lives has been forever altered, to the benefit of the tech giants.

On the bright side, earnings estimates may rise after second quarter results managed to clear a very low bar. S&P 500 profits fell “just” 34% compared the 45% drop consensus expected when companies began reporting.

Goldman cited better-than-expected Q2 results in raising their 2020 S&P EPS estimate from $115 to $130 last week. That would still represent a 21% plunge from 2019.

By the end of 2021, the bank sees earnings back at $170, although they note that not all sectors are created equal. “While we expect aggregate S&P 500 earnings to reach 2019 levels by the end of 2021, we do not expect every sector to recover this quickly”, the bank’s David Kostin remarked. “We forecast Info Tech and Health Care earnings will surpass 2019 levels by the end of 2021 [but] we expect more gradual earnings growth in cyclical sectors”, he added.

In any event, the dollar and gold will also be in focus over the next several days. Friday brought a strong bounce for the beleaguered greenback, while spot gold fell for only the second time in 17 sessions. One contributing factor: A lurch higher in US real yields. You’d be forgiven for calling that a one-off, but you never know.

Finally, as to the stimulus situation stateside, Goldman’s base case is still that something gets done. “We continue to believe that Congress is likely to pass legislation worth around $1.5 trillion, but the risk to that amount is to the upside”, the bank’s Alec Phillips said over the weekend.

“There is a risk that legislation falls through [but] we do not think these executive orders increase that risk”, Phillips added, noting that in Goldman’s view, “unilateral action might focus minds on Capitol Hill and increase the odds of an agreement”.

Let’s hope so. Because, as mentioned early Sunday, if there’s not a deal by late September, the virus relief discussion could become entangled with new spending legislation. That would, by definition, “force an agreement” (as Goldman puts it), but it would also be a harrowing experience.

It seems unlikely that either side will push things that far, though. After all, the money Trump repurposed for the extension of the federal unemployment supplement is expected to run out in just over four weeks.