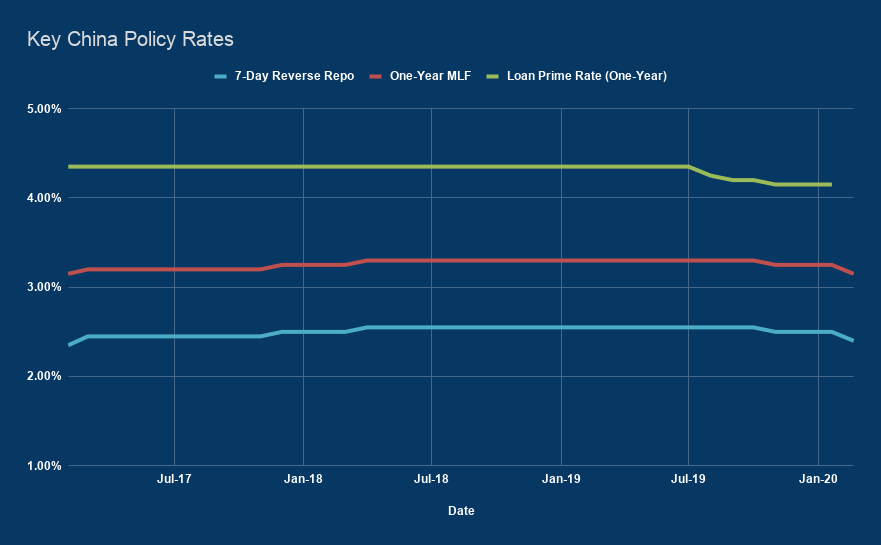

As expected, China paved the way for a cut to the de facto benchmark rate later this week, when the PBoC offered one-year medium term loans at 3.15% Monday, down from 3.25%.

The 10bps cut to the MLF rate follows similar reductions to the 7- and 14-day repo rates, which were cut on February 3, when mainland markets braved a tumultuous reopening coming off an extended holiday marred by the coronavirus outbreak.

Monday’s MLF cut sets up a cut to the loan prime rate (LPR) on Thursday.

Headed into 2020, China delivered a series of 5bps cuts to the revamped LPR, which essentially replaced the old benchmark one-year lending rate in August. The PBoC last cut the MLF rate (off which LPR is priced) in November. Three weeks later, LPR dropped by a commensurate 5bps, marking the third time the de facto benchmark was cut since the calculation was tweaked over the summer. The PBoC also cut the 7-day repo rate in November for the first time since 2015, and lowered the 14-day rate to match in December during a series of liquidity injections.

In January, the PBoC said financial institutions will cease to use the benchmark lending rate as a reference for pricing credit, shifting instead to the revamped LPR. Over the course of the six months from March to August 2020, existing loans will be converted to the new base as well.

Read more: China Orders All Loans Priced Off Revamped Rate, Ditching Old Benchmark For $21.7 Trillion In Credit

The three LPR cuts mentioned above pushed the one-year tenor 20bps lower than the old one-year lending benchmark, which means the conversion of the loan stock amounts to more easing. Assuming an additional 10bps LPR cut this week, it will be 30bps lower than the old benchmark.

While the rate was cut, the PBoC only offered 200 billion yuan in one-year funding Monday. Another 100 billion was injected via the 7-day facility. Although no MLF loans were maturing today, some 1 trillion yuan in reverse repos were due, which means the net result was a 700 billion yuan withdrawal.

That could put the brakes on the local bond rally. But it nevertheless speaks to policymakers’ intention to incrementally ease in order to offset various headwinds, from trade uncertainty to an epidemic which threatens to cut Q1 growth in half (or worse) on some estimates.

In other words, the liquidity will be there if and when it’s needed. And it will come cheaper than it did previously.