Money market rates plunged in China on Thursday.

The outsized moves came on the heels of the biggest combined OMO liquidity injection in nearly a year. After refraining from reverse repos for 20 days, Beijing came back with a bang, adding a combined 280 billion yuan (30 billion via 7-day agreements and 250 billion through the 14-day facility).

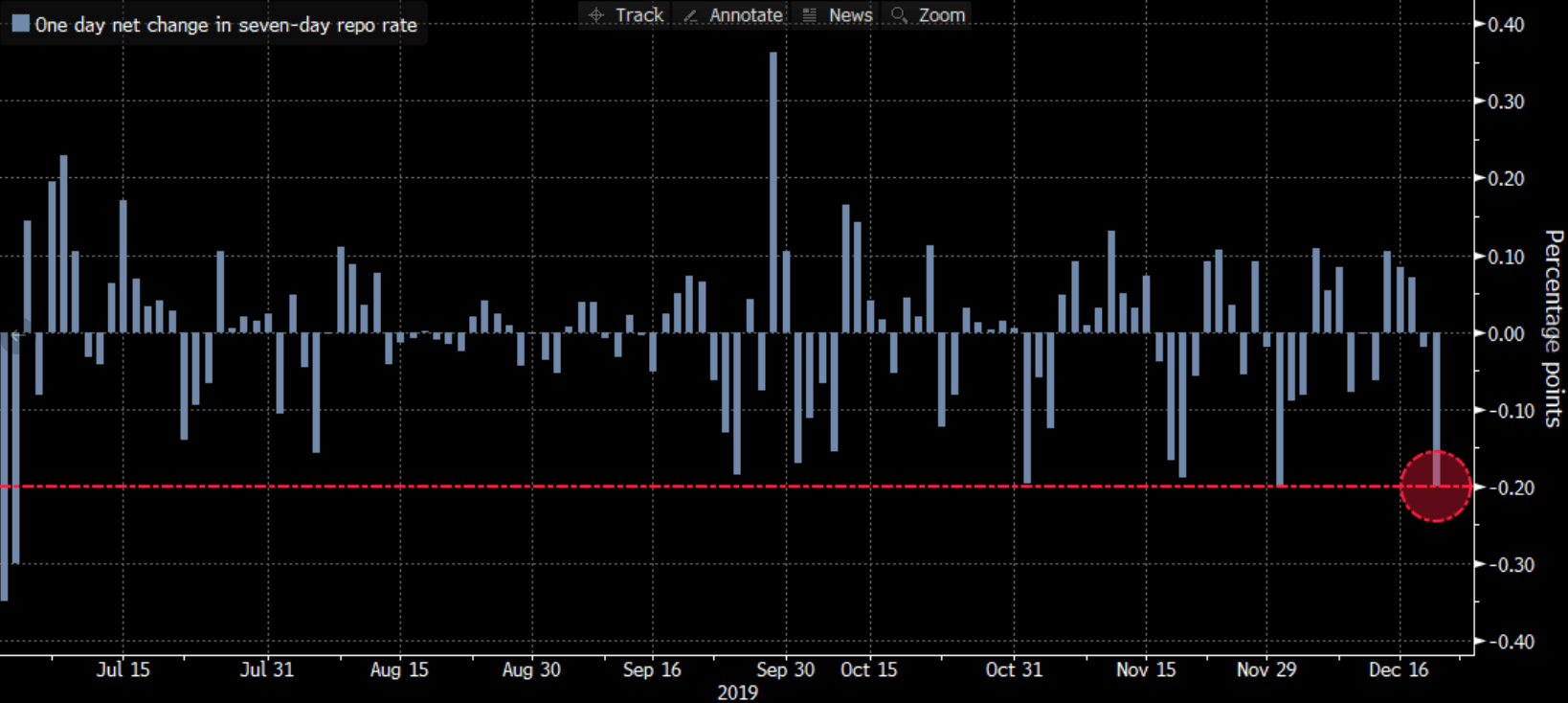

The overnight rate dropped some 40bps and the 7-day rate around 20bps, with that latter slide being the largest in more than two weeks and among the five largest since July.

(BBG)

This comes on the heels of a 300 billion yuan injection via MLF earlier this week, and also following a 5bps cut to the 14-day rate.

A couple of things are worth noting amid what I’m sure are a flurry of headlines touting a “massive” week of liquidity injections from the PBoC.

First of all, 286 billion yuan in MLF came due on Monday, so the net MLF injection was 14 billion yuan. They were rolling maturing loans. The rate was unchanged which, in turn, means the loan prime rate for December (due Friday) will likely print unchanged too (the MLF rate guides the LPR).

China cut the MLF rate early last month. Three weeks later, LPR dropped by a commensurate 5bps. The PBoC also cut the 7-day repo rate last month. It was the first cut since 2015.

So, this week’s cut to the 14-day repo rate was just a reflection of those cuts. Had they left the 14-day rate unchanged after last month’s moves, the curve would have been distorted. The PBOC did inject 200 billion yuan on Wednesday, though, a prelude to Thursday’s injections.

Still, there’s no real “shocker” here. It’s year-end, and the PBoC wants to make sure everything is in order.

And then there’s the Lunar New Year, which some say will prompt another RRR cut. The last broad reduction was in September, but it was accompanied by the announcement of two staggered, targeted cuts which were implemented in October and November.

“Rising cash demand for the Lunar New Year holiday and a flood of special bond issuance by local governments is likely to tighten cash conditions in January, and could prompt the central bank to free up funds banks must hold as reserves”, Reuters wrote Thursday, in a pretty decent summary of a note from Guotai Junan. “The Lunar New Year, which falls on January 25 next year, is expected to boost short-term demand for cash by about 1.5 trillion yuan [while] banks’ demand for cash for special bonds is also expected to peak in late January, bringing the total liquidity gap to as much as 2.8 trillion yuan”.

“The PBOC will continue to pay close attention to liquidity conditions and flexibly conduct open market operations to keep the year-end liquidity steady”, the central bank said this week, in a perfunctory statement.

None of this is to downplay the risks to the domestic economy or to otherwise suggest this week’s injections weren’t worth the headlines they received. It’s just to say that it’s worth taking a few minutes to make sure you understand the context.