Owen is a journalist and graduate student in economics at the New School. Bylines include Harpers, TPM, The Baffler, the Nation and Qz.

You can check out more from Owen on his site here and follow along on Twitter @odavis_

For financial journalists, pinpointing the source of the next meltdown is no easy task. The ones who did so pre-2008 were few. Yet today seems to be different. Read the business press and you’ll get the impression there’s a consensus as to the next recession trigger: profligate borrowing by corporations. The near-zero interest rates for much of the post-recession period encouraged companies to load up on credit. Now that the Fed is raising interest rates again, those debts could come due with greater force than expected, particularly if economic growth falters.

Here’s a sampling of pieces on corporate debt from just the last week. Reuters:

General Electric may be the canary in the credit market’s coal mine. The company’s bonds tanked this week even as an asset sale briefly lifted its shares. That’s a warning shot for all debt investors. U.S. companies owe more money than ever, and the quality of their loans and bonds has deteriorated. Rising interest rates and slowing growth could make this a big problem.

The largest exchange-traded fund that buys high-yield debt has lost more than $1.5 billion this week, with short interest, as calculated by IHS Markit, ticking higher to 26 percent of shares outstanding. Investors also soured on investment-grade companies, pulling money from iShares iBoxx $ Investment Grade Corporate Bond ETF for a second day, but piled into short-dated Treasuries, which are more insulated from rising rates and corporate defaults.

The FT:

In the US at least, Obama-era regulations until recently prevented businesses from ratcheting up debt even further. But private equity groups have taken advantage of the Trump administration’s more relaxed approach by doubling the proportion of deals done with leverage of seven times or greater, which had often been barred under the old rules. Bankers and deal lawyers warn that even these stark figures may understate the build-up of loose credit. That is because, as well as offering larger amounts of debt in proportion to a company’s profits, lenders have become less exacting about how those profits are defined.

The FT, again:

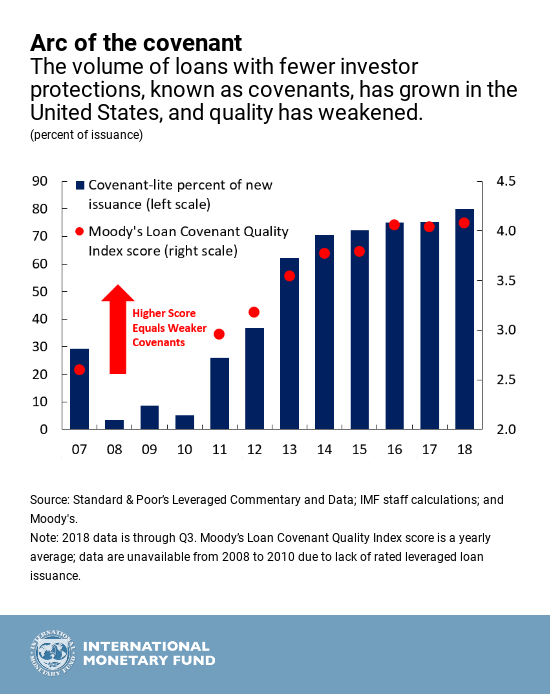

…beneath the boom lies an unsettling reality: lending protections are bad, and may be getting worse. In fact, they’re just about the weakest on record, according to a Moody’s gauge, which measures various metrics related to a lender’s ability to recoup capital. These include leverage requirements, the ability of borrowers to sell assets and collateral, among others. Given these conditions, Moody’s reckons recovery rates when the cycle turns will be much lower than in the past.

And the FT, yet again:

Paul Tudor Jones, the veteran hedge fund manager, has warned that “some really scary moments” in the swelling corporate debt market could precipitate another financial crisis. … “If you go across the landscape you have levels of leverage that probably aren’t sustainable and could be systemically threatening if we don’t have . . . appropriate responses,” he said at the Greenwich Economic Forum in Connecticut.

And in its latest financial stability report, the IMF points squarely to leveraged loans–perhaps the riskiest corner of the corporate debt market–as a potential trigger for instability:

At this late stage of the credit cycle, with signs reminiscent of past episodes of excess, it’s vital to ask: How vulnerable is the leveraged-loan market to a sudden shift in investor risk appetite? If this market froze, what would be the economic impact? In a worst-cast scenario, could a breakdown threaten financial stability?

The important stat here is the amount of leveraged loans that are deemed “covenant lite,” meaning they include fewer investor protections and looser income and collateral standards. In case the loan goes south, investors in these sorts of loans can claw less of their capital back. Here’s the growth in covenant lite loans globally:

Zooming out to the broader corporate debt market doesn’t make the picture any prettier. The growth in U.S. investment-grade credit–is disconcerting given the growing share of debt in the BBB group, that is, the lowest-quality tier a bond can have before it becomes “junk”.

Concerns over corporate debt have been brewing for some time now, but the pitch has grown louder in recent weeks, thanks in part to the travails of the woebegone GE (which, I can’t help but add, has spent more than $100 billion buying its own stock since 2000, $24 billion in just the last three years). Here’s Scott Minerd, the revered chief investment officer of the investment bank Guggenheim, a few days ago:

The selloff in GE is not an isolated event. More investment grade credits to follow. The slide and collapse in investment grade debt has begun.

— Scott Minerd (@ScottMinerd) November 13, 2018

Janet Yellen raised similar concerns last month in an interview with the FT (if you haven’t noticed, the FT is particularly worried about corporate debt):

“I am worried about the systemic risks associated with these loans,” said the former central banker. “There has been a huge deterioration in standards; covenants have been loosened in leveraged lending … There are a lot of weaknesses in the system, and instead of looking to remedy those weaknesses I feel things have turned in a very deregulatory direction.”

This all paints a concerning picture, but there are mitigating factors. Debt is up, but so are earnings and corporate liquid assets, the crucial determinants as to whether companies can continue paying their creditors. Analysts at JPMorgan recently wrote that while corporate debt is a “key vulnerability,” they don’t believe it to be as threatening as the subprime bubble of the mid-2000s. Their note tamps down some concerns around leverage, pointing to the fact that there hasn’t been disproportionate borrowing amongst companies that are already highly levered.

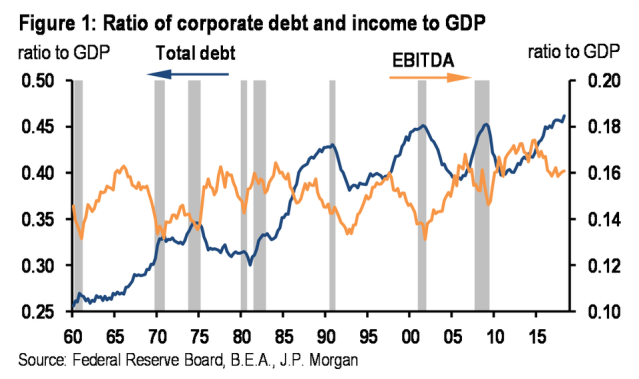

Still, the JPMorgan analysts present some cause from concern. Comparing the scale of debt to earnings (before interest and taxes have been deducted) yields this picture:

(JPMorgan)

Earnings (orange) are historically elevated, but debt is at record levels relative to GDP. Given low interest rates, that might not be such a concern. But higher rates plus lower growth could be a nasty recipe.

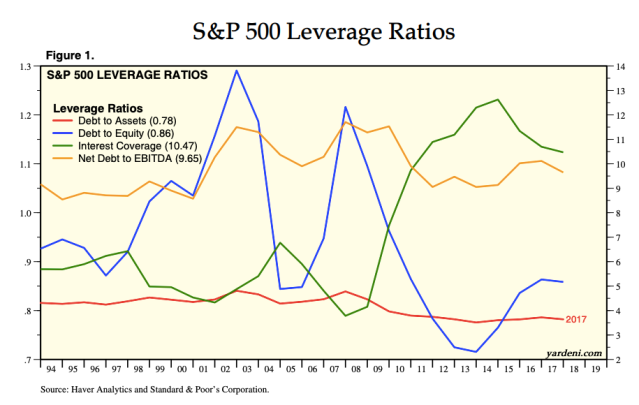

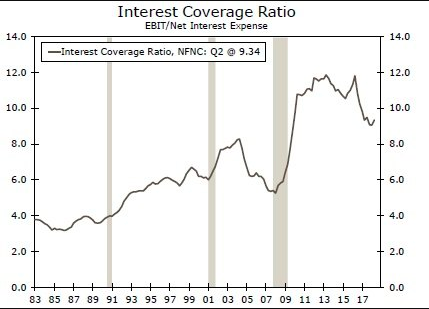

One of the best ways to quantify the dangers posed by the corporate debt is the interest coverage ratio. This tells you how many times over a company can pay its quarterly interest expenses with its quarterly earnings. Eg, if Owencorp earns $2 billion in a quarter and has to spend $1 billion in interest payments to creditors, Owencorp’s interest coverage ratio is 2x. Below 1.5 is considered the danger zone. The green line below, courtesy of Yardeni, is where the S&P 500 is at now:

There’s been some deterioration of late, but still way above where we were at in previous cycles. This is as expected given the historically low interest rates companies have secured in the past several years. And it’s not just corporate behemoths that can pay their interest with ease; small businesses are presently in the clear as well.

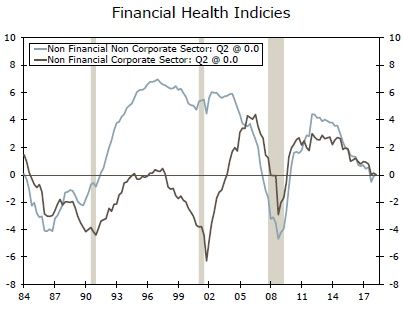

That chart comes from Wells Fargo, which–lest we grow too complacent–also gives us this 30,000-foot view of financial health of both corporate and noncorporate businesses. The upshot: the financial health is “not worrisome at present despite having deteriorated somewhat in recent years.”

Like everyone else, Wells Fargo urges caution about corporate debt, but suggests that should GDP growth continue apace and earnings remain strong, we have nothing to worry about.