Earlier this week, I mentioned in passing that home listings in the US posted their largest decline in more than two years during the four-week period ended December 7.

That was notable because more supply’s a big part of any constructive narrative for an otherwise beset US housing market headed into 2026.

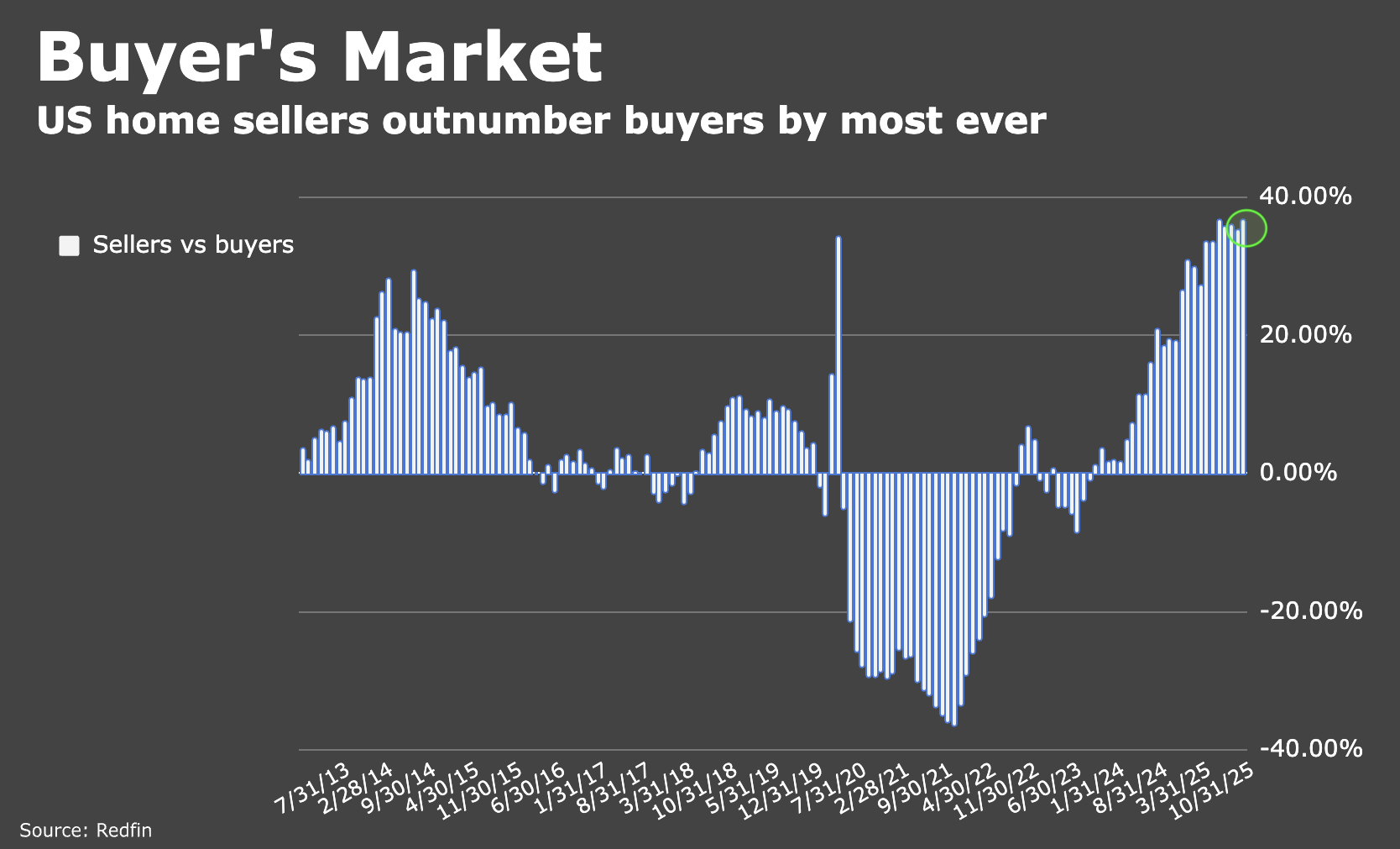

Inventories have generally — albeit slowly — recovered, but the affordability math’s now so challenging that even the lowest mortgage rates in 14 months and a preponderance of sellers compared to buyers isn’t enough to thaw the market.

Friday’s existing home sales update from the NAR underscored all of those points. Sales rose just 0.5% in November from October, less than half the gain consensus expected.

The good news is that November’s advance counted as the third gain in a row, but as the figure above reminds you, “good” remains a highly relative term.

NAR Chief Economist Lawrence Yun cited lower rates for the tepid increase in sales, but noted that “inventory growth is beginning to stall.” He attributed that to seasonality. “Homeowners are in no rush to list their properties during the winter months,” Yun said Friday.

There’s obviously some truth to that, but as noted here at the outset, it isn’t just the seasonal. Until the 30-year fixed sports a five-handle, the numbers won’t add up for a lot of homeowner hopefuls. That means they’ll be demanding steeper price cuts than sellers are willing (or able) offer, hence pulled listings.

I’ve said this again and again: If you could afford to buy with rates north of 6% and prices at or near records, you probably already bought. That leaves a pool of would-be buyers who are highly rate- and price-sensitive. They need more rate relief than they’ve enjoyed over the past few months, and bigger price breaks than they’ve been able to secure.

Friday’s release showed the median existing home price in November was $409,200, up 1.2% YoY.

Although gains aren’t keeping pace with inflation — leading to a contraction in real housing wealth — prices have risen for 29 consecutive months in absolute terms versus the same month the prior year.

In his remarks accompanying the data, Yun alluded tangentially to the inflation-adjusted contraction in housing wealth, noting that wage growth’s meaningfully outstripping property price appreciation.

Mathematically, that helps, but let’s be honest. If you’re a typical family earning the median household income, trying to save the $75,000 you’ll need for a respectable downpayment is a daunting task, particularly if you’re starting from scratch. The fact that your annual pay may be growing at a brisker clip than the price of the train you’re trying to catch isn’t a lot of help when that train ticket costs nearly half a million dollars.

The latest update from Redfin, released on Thursday, showed pending home sales fell nearly 6% from a year earlier in the four weeks to December 14. That, Dana Anderson remarked, was “the biggest decline since the start of 2025.” “House hunters are retreating amid high housing costs and a seasonal slowdown, leading prospective sellers to pull back, too,” she said.

{kind=link}

{kind=link}

I am trying to convince my oldest child that home ownership at this point (recently married, no kids) is a goal they should postpone, not just because of the initial cost but also because of the ongoing annual real estate taxes, insurance and maintenance costs.

I’m not having much luck with convincing them. They are Zillow addicts, but have yet to find something that they can afford that they would be excited to own.

H-Man, I believe relief is on the horizon — there will be falling interest rates and old goats like me will take a significant haircut to unload the homestead.