Is the US in a recession? Who knows. Probably. Some sort of recession. The sun’s setting on something. Maybe not on the economy specifically, but it’s gettin’ dark out there.

What do you do when night falls? Kamala Harris says we’re supposed to shine — “fill the sky with the light of a billion stars.” I don’t know about that. It might be better to stay dim for a while. Lest they should ship your shiny ass off to El Salvador.

I’m kidding. I’ve said it before and I’ll say it again: Sometimes you gotta laugh at life.

As far as the US economy’s concerned, it’s notable that we’re actually seeing a continuation of the dichotomy which defined the Biden years: Sentiment’s awful, but the hard data hasn’t really rolled over. It’s better, maybe, to watch what consumers do, rather than listen to what they say.

Late last week, the preliminary read on University of Michigan sentiment for May suggested Americans are even more pessimistic now than they were in April, no trivial observation considering April’s readout was among the worst on record.

The simple figure makes two important points simultaneously. First, the two marquee measures of household moods in America never recovered from the pandemic. Second, things took a demonstrable turn for the worst since Inauguration Day.

So, the “vibecession” lives on, and indeed it looks by now like whatever the “vibes” version of a depression is.

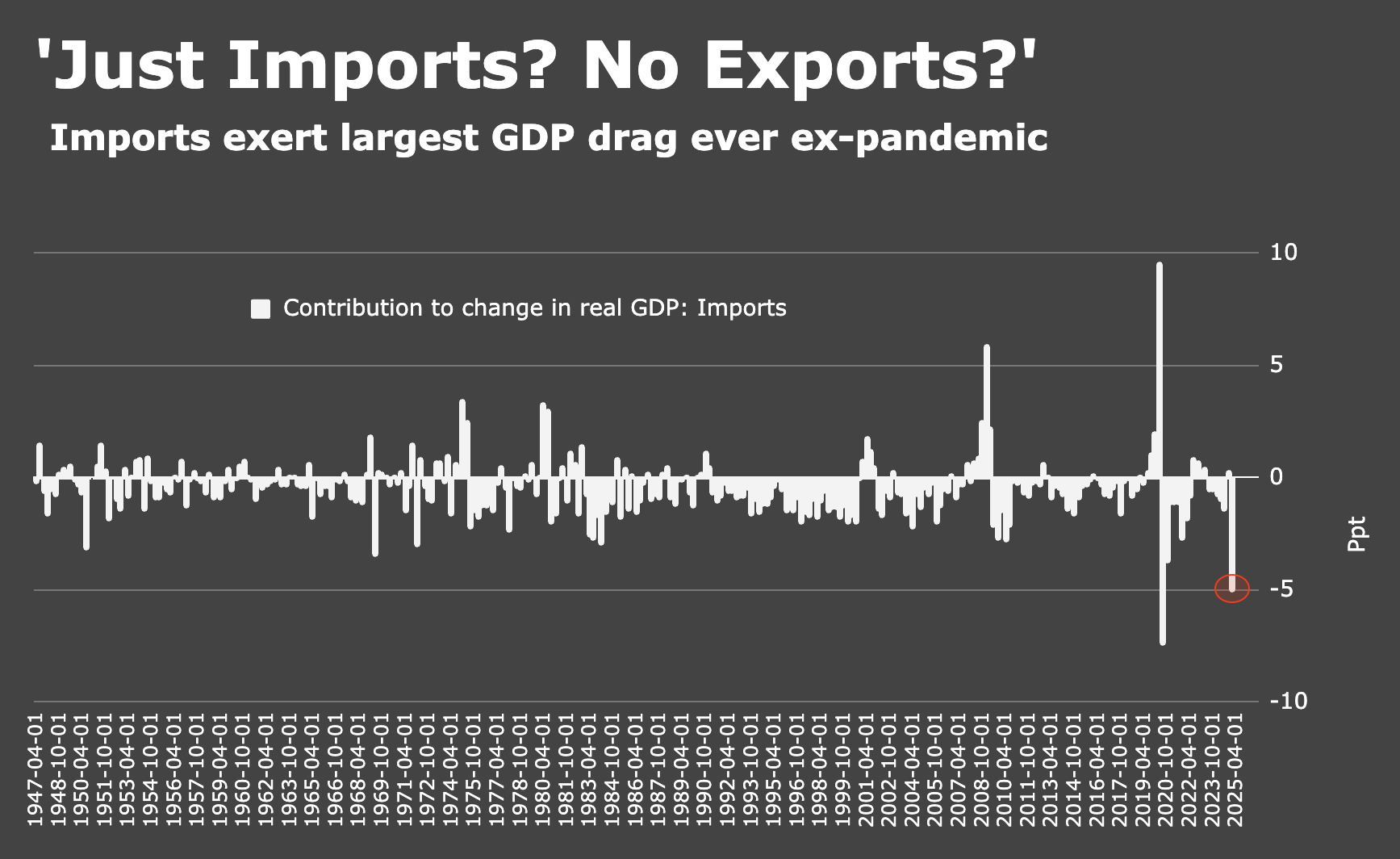

But again — and notwithstanding bad optics attributable to historic import drag in the Q1 GDP tally — there’s not a lot of hard evidence to back up a recession claim. Has hiring slowed? Yes. Has spending slowed? Yeah, at the margins maybe. But doomsayers are for now relying mostly on anecdotal accounts of gloom.

With that in mind, the figure below, from BMO’s Ian Lyngen, is interesting. It plots the change in 10-year US yields around previous instances where the expectations index in the Conference Board survey fell below 60.

You’re encouraged to note that the forward-looking measure Lyngen’s citing printed a truly unfortunate 54.4 in the April readout, more than 25ppt below the threshold which typically precedes a recession and the worst reading since October of 2011.

As the figure makes clear, the current episode’s an anomaly. “Despite the plunge in consumers’ expectations, 10-year notes have sold off 20bps since the confidence update,” Lyngen remarked, noting that in “the prior six instances in which consumers’ expectations dropped below 60, there was a clear downward bias for 10-year yields over the ensuing months.”

That makes sense. As noted, expectations this poor typically precede recessions and bonds tend to rally in the presence of deteriorating economic conditions. “Before the current episode, 10-year yields were typically 20bps lower by the corresponding stage and 40bps lower, on average, two months after consumers’ expectations dropped below 60,” Lyngen went on.

One takeaway is that bonds are simply reading the hard data and seeing no evidence of a downturn. The other explanation says US Treasurys are losing some of their haven appeal and/or demand isn’t what it used to be. As Lyngen put it, in characteristically diplomatic fashion, “the current macro landscape is anything but traditional and there has been no shortage of bearish crosscurrents at play in the Treasury market.”

{kind=link}

See FTSE USD IBOR Cash Fallbacks data

https://www.lseg.com/en/ftse-russell/benchmarks/usd-ibor-cash-fallbacks/usd-ibor-consumer-cash-fallbacks-sofr-compound-in-advance-summary

On 02 May 2025, the 12-month rate was 4.47740%

On 15 May 2025, the 12-month rate was 4.80518%

Seems like the immediate effects of tariffs are the Stag (see above) and the obvious tail effects will be the flation. By the time Trump either fires Powell or he leaves at the end of his term the Fed won’t be able to lower rates enough to get us out of this manufactured mess.

My impression of my milieu (middle class and upper-middle class millennials) is that we are all despondent over the state of the world but having two or three kids anyway and are now coming into our prime earning years and firing bazookas and machine guns into the economy – cars, houses, appliances, furniture, electronics, bikes, toys, clothes, fuggin sunglasses and espresso machines and PS4s and soccer cleats. Like so much crap. And we’re all doing it. Millennials are a large demographic group, too. Meaning I wonder if there is an inelastic demand impulse hidden beneath the suspect survey data. Perhaps the rise of the millennials will propel the American economy into the post Boomer epoch.

As a millenial parent, I was going to argue that I hate all the crap, but then I remembered how much the kids’ grandparents, aunts, uncles, and even my wife seem to buy the things you listed. Granted, we are among those fortunate enough to have plenty of disposable income.

If it were up to me, I’d rather save that money and retire early into a teaching or small business owner career, but others are clearly addicted to hitting that checkout button.

Fellow older millennial here can confirm… I have or will have purchased virtually all the items you outlined whether I want to or not due to kids. Two of them… My little broke blessings! 🙂