Good news, albeit news no one cares about.

Sorry, that’s insensitive. People in the UK care, and the UK still matters. Sort of.

Headline inflation across the world’s sixth-largest economy slipped in data released Wednesday, ahead of Rachel Reeves’s spring statement unveiling billions in government spending cuts.

At 2.8%, the headline CPI readout was below estimates and matched the BoE’s Q1 2025 forecast from the February projections, which’ll be updated in May.

Core printed 3.5%, which is obviously too high, but… well, I don’t know. I don’t know what comes after “but” in this context, which is to say I’m not sure there’s a silver lining. “But” it was lower than January’s core print, maybe.

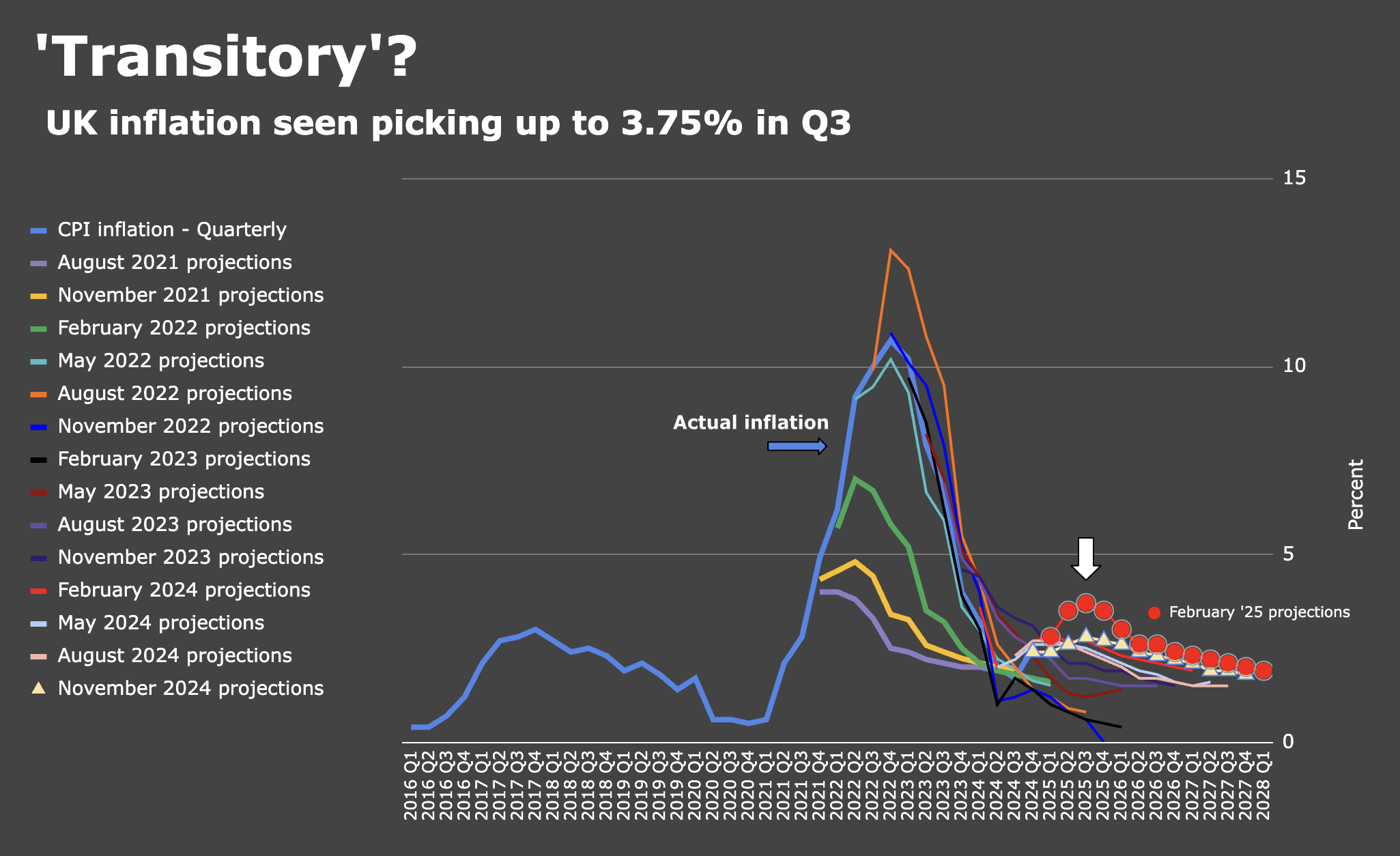

Recall that the BoE was very cautious in holding rates earlier this month. Only Swati Dhingra voted for a cut, and that’s like saying the Easter Bunny voted for chocolate eggs (she’s a dove’s dove). The bank delivered its third reduction of the cycle the month prior (i.e., at the February meeting) but it came packaged, somewhat awkwardly, with an upwardly-revised near-term inflation trajectory.

Wednesday’s ONS release doesn’t alter the outlook, but it at least suggests the situation hasn’t worsened. In that respect, market pricing will probably move incrementally towards a May cut.

The fly in the soup’s always services inflation, which stuck at 5% in February. As the figure below reminds you, inflation on the services side is 2.5x target, and notwithstanding a fleeting slowdown two months back, it’s intractable.

“There are tentative signs that the forthcoming rise in employer National Insurance is having an impact on service sector inflation, which came in a tad higher than expected,” ING’s James Smith said, adding that hospitality is “particularly exposed to the forthcoming tax hike, as well as the near-7% rise in the National Living Wage, given its labor-intensive nature.”

Smith went on to emphasize just how important the services story really is for the BoE, on the way to gently noting that “with no discernible rise in redundancies nor fall in employment, the hawks on Threadneedle Street might be tempted to conclude that the net impact of April’s tax hike is to push up prices rather than reduce jobs, despite survey after survey pointing to weaker hiring intentions.”

There you go. That’s really the long and the short of it. Of course, the BoE’s going to cut again in 2025, it’s just a matter of when and how many times, and while the consensus on Wednesday seemed to be that the February inflation data lifted the odds of a move in May, it’s important to note that headline price growth’s going to accelerate over the next two quarters, likely flirting with 4% in Q3.

It’s possible that services inflation decelerates over the same period, but in the simplest possible terms: There isn’t a snowball’s chance in hell that it (services inflation) will fall to 2% even if it undershoots, and headline inflation’s going to rise mechanically, so one way or another, the BoE’s going to be staring at a conjuncture which looks something like 4% services inflation and 3.5% headline price growth in and around late summer.

This is, you’re reminded, a monetary authority with a single mandate, although I guess that’s technically too strict. Inflation’s the “primary objective,” to use the official language. “Strong growth” and other objectives are “subject to” the inflation target, which is still very much in question.

{kind=link}