Economists will tell you to fear the inversion. Traders will tell you to fear the re-steepening.

I’m talking about the yield curve, of course, which is currently at risk of registering its first ever false alarm vis-à-vis recession “predictions.”

The rationale for fearing the re-steepening is straightforward: If the curve’s bull steepening, short rates are probably responding to rate cuts (or falling in anticipation of rate cuts), and rate cuts are indicative of monetary policy reacting to recession (or trying to head off recession). Recessions are bad for corporate profits, and falling profits are bad for stocks.

For equities, then, it’s not about yields (or curve shape), it’s about what the curve is probably saying about the economy. In his latest, Goldman’s David Kostin underscored the point. “Growth, rather than changes in yields or the shape of the curve, is the most important driver for equity returns,” he wrote, summarizing more than three decades of data.

Median monthly US equity returns when the curve steepened were 1.3% looking back nearly a quarter century, Kostin said, noting that stock performance was actually pretty consistent regardless of what the curve happened to be doing at any given time.

On the other hand, returns varied meaningfully depending on investors’ outlook for the economy, which Goldman proxies using relative performance for cyclicals versus defensives.

The figure above illustrates the point. “This relationship has held true regardless of whether the yield curve was steepening or flattening,” Kostin wrote. “In other words, the reason the yield curve shifts is far more important for stocks than the shape of the curve itself.”

That’s intuitive to the point of being tautological, and while I usually indulge in a little good-natured humor at the appearance of tautological “analysis,” I’ll refrain this time.

The dispersion comes when you look at sector-level (and factor) performance. Again, the results are intuitive: Financials, value stocks and small-caps outperform during bear steepening episodes, while bull steepeners benefit healthcare and equities with hefty margins given the likelihood of an accompanying recession.

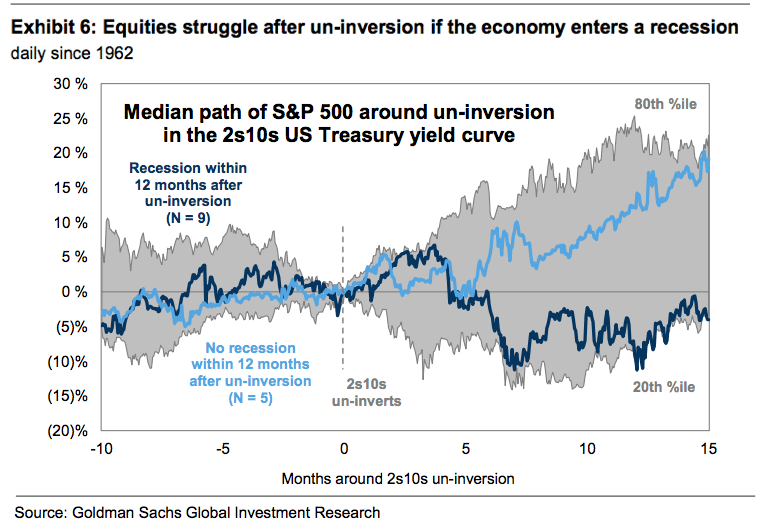

The figure below shows how stocks performed around historical dis-inversions.

Again, we’re treading dangerously close to tautology territory, but the takeaway is that stocks may fall if the dis-inversion presages a recession, while equities can keep rising after the curve dis-inverts as long as the economy holds up.

For what it’s worth, Goldman expects the 2s10s to reach positive territory sustainably by the end of the third quarter, and the bank’s economists put the odds of recession at just 15%, which obviously (or maybe “ostensibly” is better) bodes well for equities.

Kostin summed it up. “Simply put, equity investors focused on the implications of yield curve reshaping should follow the advice offered 32 years ago by James Carville, the manager for then-candidate Bill Clinton’s successful 1992 Presidential campaign: ‘It’s the economy, stupid.'”