“Multiple expansion has moved ahead of where macro fundamentals dictate fair value to be,” Morgan Stanley’s Mike Wilson said Monday, again reiterating a cautious stance on US equities, which he described as behaving consistent with late-cycle environments where investors expect a Fed pivot.

Now, with valuations stretched, stocks need a re-acceleration in growth or an incremental dovish turn from monetary policy to prevent de-rating, Wilson suggested.

I’m sympathetic, albeit with the usual caveats, many of which I’m compelled to reiterate week after painful week. It’s too late for last year’s bear calls to be “right.” That battle is lost. And it feels like some strategists (not necessarily Wilson) are trying to subtly “roll” their October 2022 lows retest calls into modified bear cases centered around de-rating in the face of stubbornly elevated yields.

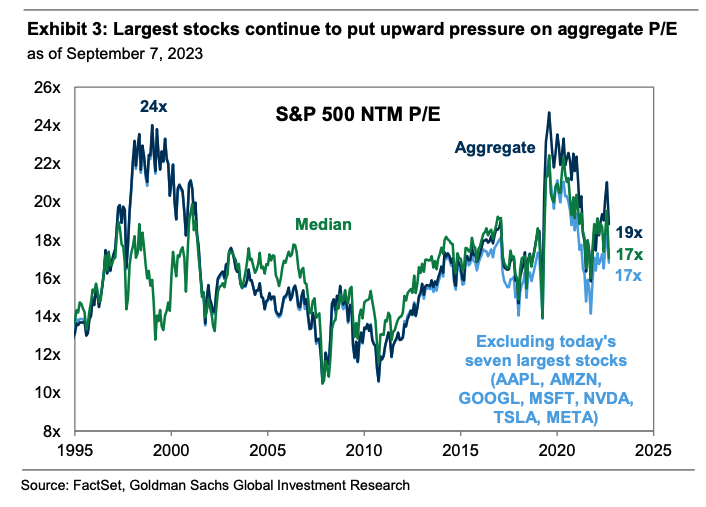

Even if you can get past what, let’s face it, is a steadfast refusal on the part of some bears to concede that even if stocks fell 20% this week, that wouldn’t make nine-month-old (and in some cases 12-month-old) bear cases “right,” the problem with the de-rating thesis is that the so-called “S&P 493” (so, the S&P without the big seven mega-caps) trades at 17x. That’s not cheap, but it’s not wildly expensive either.

So, you need the “Magnificent 7” to de-rate. And meaningfully. That, in turn, means you need 2023’s ostensible tech “bubble” to deflate. But not everyone thinks it’s a bubble in the first place, and even if it is, it’s far from obvious why it should burst imminently, as opposed to inflating further.

And you also need real yields to either climb or at least stay where they are. That might be a tall order. 10-year reals have doubled since April, and 30-year reals are up 50bps in less than two months to the highest in a dozen years. “The recent move higher in both real and nominal yields to cycle highs poses a headwind to equity valuation as the correlation between real rates and equities has once again pushed deeper into negative territory,” Wilson remarked.

As I’m always keen to note, rising reals are kryptonite for risk assets, and especially richly-valued, long duration equities. But the most vulnerable parts of the market in that regard (e.g., profitless tech) were bled out last year.

To be sure: There’s a level for US reals beyond which stocks will buckle. But we clearly haven’t seen it yet and it’s hard to imagine (for me anyway) that long run reals are going to move materially higher than 2%. If nothing else, a 2% real return over a long horizon with no credit risk (Fitch aside) is a decent proposition for investors.

I also see some tension between Wilson’s assessment that the “burden” is on a growth re-acceleration and a Fed pause/pivot to justify valuations. The implication is that neither is likely, which means Wilson needs decelerating growth and a stubborn Fed. You could very plausibly argue that’s precisely how things are likely to develop given Jerome Powell’s insistence on “finishing the job” (where that presumably means holding terminal for as long as possible, even in the face of a burgeoning slowdown). But stocks are going to trade every incremental piece of bad news as good news unless and until the news turns unequivocally bad — so, too bad to ignore. At that point, you’d expect a clear indication from the Fed that hikes are over, which would undercut reals and the dollar, potentially bolstering equity valuations.

Wilson confirmed that he does, in fact, expect a macro-policy conjuncture defined by a growth deceleration and a recalcitrant Fed. “Given our economists’ forecasts for muted GDP/PCE growth in the coming quarters and their view that the first Fed cut is still six months away, we’re skeptical that a significant re-acceleration in growth and easier policy are coming this year,” he wrote.

I agree. But equities don’t need “easier” policy to stay supported. Oblivious as stocks generally are, it’s not lost on equities that there’s just 110bps of easing priced into 2024. That might sound like a lot, but it’s just one 25bps increment every quarter. The point: Stocks don’t expect panic-easing. The spread between market pricing for Fed funds in December of 2024 and the current long run dot suggests markets expect policy to still be ~200bps into restrictive territory 15 months from now. Stocks know that, and they’re still where they are. Absent a complete economic meltdown, I’m not convinced that equities will be aggrieved at the prospect of waiting until March for the first rate cut.

Further (and Wilson readily acknowledged this) Morgan Stanley isn’t banking on a recession. Not in the economics research department, anyway. The bank’s economists do think faith in a soft landing might’ve left investors too complacent, but their subjective recession odds for the US are 35-40%. That’s well below consensus, which is still around 60%.

Wilson took a glass half-empty approach to that too, though. 35-40% is “notably higher than it is in a typical cyclical backdrop and is not priced into equities broadly, in our view,” he wrote, in the course of recommending a late cycle portfolio (a barbell of defensive growth and Industrials/ Energy).

Part of me wants the bears to be right. Or at least the ones who, like Wilson, seem committed to analytical rigor and earnestness. But I fear we’re just as likely as not to look up two or three months from now and find the S&P trading within 5% of where it is today on either side.

{kind=link}

“If nothing else, a 2% real return over a long horizon with no credit risk (Fitch aside) is a decent proposition for investors.”

As wealth gets passed down through estates to (younger) heirs – the investment horizon increases significantly; and 2% real returns doesn’t seem very compelling compared to potential SPY inflation adjusted returns- which were 6.86%, 9.73% and 7.16% over the past 5 years, 10 years and 30 years, respectively.

Long-term real rates should generally track potential GDP unless inflation is very low. To get real yields in excess of 2%, you need higher potential growth (e.g., a productivity boom).

For a couple of decades I enjoyed the fruits of a side-gig as an expert finance/econ expert witness. I worked both sides of the table in civil trials valuing businesses, assets, lives and other related items. Since guessing inflation 20 years into the future is a fruitless task, my research showed that in the long run a real discount rate of 2-2.5% has prevailed most of the time and would work well to deal with such valuation questions. Life insurance policies over my lifetime promise contract rates in that range, plus any dividends they earn. From the mid-18th to the early 20th centuries, trust fund gentlemen were described in terms of their yearly allowance — master Robert has 4200 (GBP) a year, etc. To give someone an allowance of GBP4200/yr required a principal balance of GBP210,000 earning 2% and would support a young gentleman with a nice flat and a “man” to take care of him, as long as he didn’t have a bad gambling habit. Two percent in a quiet economy with no inflation would carry one quite well for a couple of centuries at least.