Last month, I asked if the US consumer was “finally exhausted.”

I was editorializing around the monthly consumer credit update from the Fed, which showed the second-smallest increase in revolving credit since October of 2021.

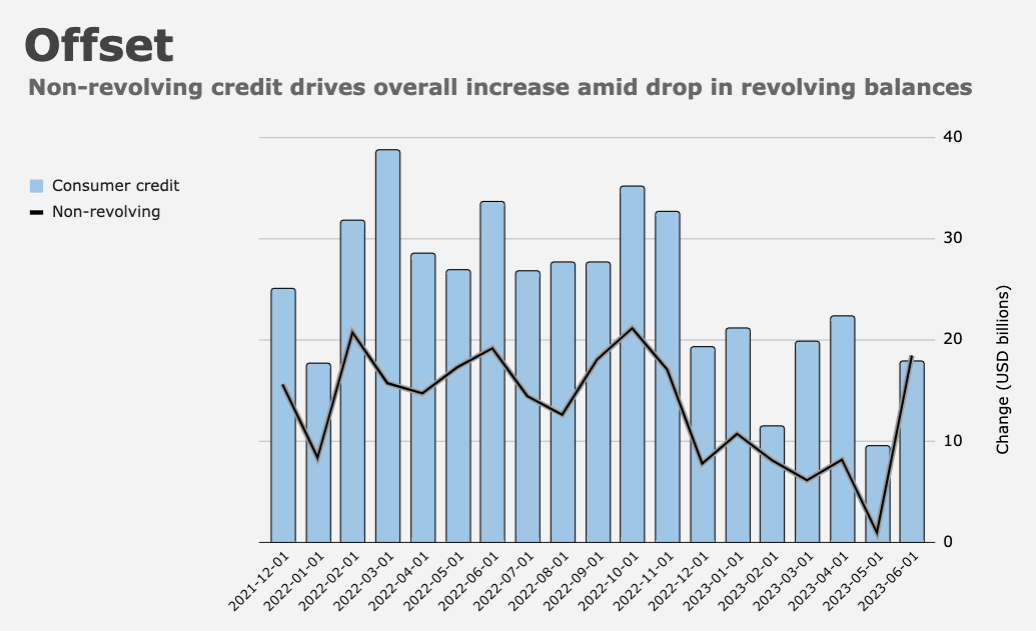

Fast forward four weeks, and data for June (the series is reported on what amounts to a two-month lag) showed a contraction in revolving credit, the first since inflation took off in earnest across the world’s largest economy. The consumer credit figures aren’t adjusted for prices.

The drop is notable. The streak is over. It lasted 25 months.

With allowances for much slower headline price growth, the decline nods in the direction of retrenchment. Recall that credit card rates are now the highest in data going back half a century.

I’ll include some familiar color which helps to contextualize the figures. NY Fed data released in May showed Americans’ card balances were flat at $986 billion in the first quarter. It was the first Q1 in the (relatively short) history of the dataset during which the nation’s credit card balance didn’t decrease. Americans are the proud owners of more than 570 million credit card accounts. The next household debt and credit report (covering Q2) is due Tuesday.

Meanwhile, Monday’s release showed non-revolving credit, like student and car loans, rose the most since October after falling for the first time since April of 2020, when the nation was still reeling from the onset of the pandemic and associated economic tumult. (May’s small drop was revised on Monday to show a small gain.)

It’s worth noting that the total value of car loans in America hit another new record.

At 7.81%, the rate on 60-month car loans is the highest since 2007, according to the Fed.

The jump in non-revolving credit drove a $17.8 billion net gain for overall consumer credit in June, more than expected.

Total non-revolving credit outstanding stood at $3.735 trillion at the end of the month. The tally for revolving credit was $1.262 trillion.

{kind=link}

So we’re saying American consumers are $5 trillion in debt. Add that to $12T in residential mortgage debt. For context estimated US GDP in 2023 of $27T.

What could possibly go wrong?