The American consumer is still spending, “albeit a little more slowly,” Jamie Dimon said Friday, as JPMorgan kicked off big bank earnings in the US. Household balance sheets “remain healthy,” he added.

The firm easily beat estimates on the top-line. Managed revenue of $42.4 billion was $3 billion ahead of consensus.

The bar for Wall Street was lowered significantly headed into reporting season. For example, the average adjusted EPS estimate for America’s largest banks fell more than 20%, thanks in part to Goldman’s uncharacteristic, if savvy, efforts to manage down expectations. At JPMorgan, Q2 EPS of $4.75 ($4.37 excluding significant items) looked like a large beat. Consensus was $3.83.

Net interest income was $21.8 billion for the quarter, up 44%, ahead of estimates and a new record. Recall that the bank raised its full-year NII forecast last quarter to $81 billion from $73 billion, and tipped additional upside to $84 billion in May. On Friday, they lifted that guidance again, to $87 billion.

The Street was looking for around $83 billion for the full year. In April, the bank cautioned on “significant sources of uncertainty” around NII, including the “magnitude and timing [of] deposit repricing,” the read-through of various macro scenarios for loan growth and the “impact of policy choices,” including RRP terms. So far so good, apparently, although CFO Jeremy Barnum told journalists Friday the uncertainty around NII remains.

The First Republic integration is going ok. Dimon invited 85% of 5,100 onboarded employees to join his flock. Nine out of every 10 accepted an offer they couldn’t refuse. $6 billion in net deposit inflows suggest former First Republic customers “trust our balance sheet and the strength and confidence it provides,” JPMorgan mused, adding that the bank now sees an “opportunity to outperform original expectations and accelerate our affluent strategy.”

The deal resulted in a net after-tax gain of $1.8 billion, but a related reserve build lopped $0.30 off EPS. In Corporate, credit costs were a net benefit, though — JPMorgan was able to release reserves after reclaiming the deposit put into First Republic during March’s botched rescue attempt.

Digging a little further into the report, Dimon described IB as “challenged.” That’s nothing new, and the bank managed to top estimates anyway. Revenue of $1.49 billion was a small beat.

For those interested, the breakdown showed advisory revenue missed, while equity and debt underwriting both beat. It’s been tough going for IB over the last several quarters on Wall Street.

JPMorgan’s trading results were decent. Note that uncertainty around the debt ceiling standoff hampered client activity at some banks, and the low vol environment thereafter didn’t exactly scream “trading windfall.”

Nevertheless, FICC revenue of $4.57 billion topped estimates, and fell just 3% YoY. Consensus was looking for $4.3 billion. The bank cited lower revenue in macro businesses, offset by higher revenue in the securitized products and credit.

Equities missed, but not by enough to matter. Revenue of $2.45 billion rounds up to “in line” if you’re feeling generous.

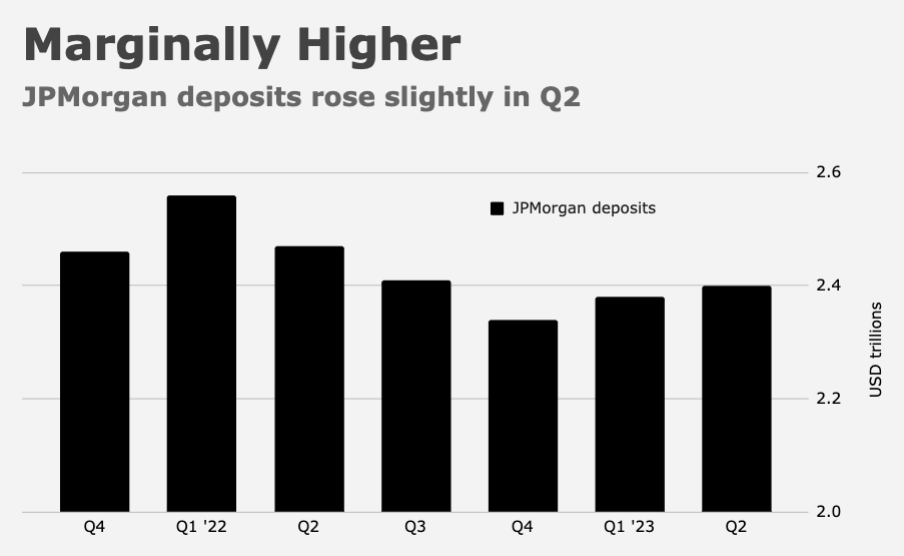

Deposits rose slightly from Q1, but obviously fell YoY. $2.4 trillion was a miss. Analysts expected $2.44 trillion.

I could go on, but I’m not sure there’s a lot of utility in additional editorializing. JPMorgan is fine. “Almost all of our lines of business saw continued growth in the quarter,” Dimon remarked.

As usual, he made a series of what some observers might describe as passive aggressive comments about regulatory ambiguity. But as is his wont, Dimon reiterated that what happens on that front won’t much matter for JPMorgan’s overall performance, even if it matters for everyone else, including Main Street.

“We will manage to any new requirements as we have demonstrated in the past,” Dimon said. “However, we caution that material regulatory changes would likely have real world consequences for markets and end users.”

{kind=link}

Borrowing at 0.01% ( rate JPM pays on bank deposits) and investing at 5% (ONRRP rates) is a sweet deal indeed!

Banks are now buying UST’s, instead of borrowing from ONRRP- which is yet one more indication that rates have peaked. If ONRRP balances heads back to somewhere between zero and $400B (where it normally resided prior to covid) – that is a lof of UST’s that will get purchased by banks.

https://fred.stlouisfed.org/series/RRPONTSYD/