I don’t want to call the situation hopeless, but Wednesday’s inflation update out of the UK counted as another very poor result for the Bank of England.

Headline CPI rose 8.7% in May from the same month a year ago, ONS said. Economists (silly them) were hoping for a deceleration to an 8.4% pace.

Context is important. The last inflation report (so, data covering April) was described with adjectives like “terrible ” and “crushing.” Wednesday’s figures thus constituted a dubious encore.

Particularly vexing was the core print. 7.1% counted as a new three-decade high and an acceleration from April’s YoY pace. Core inflation in the UK is running 3.5 times the rate observed in May of 2021, when price growth took off across the developed world.

The annual pace of services sector inflation rose markedly to 7.4% from 6.9% in April.

The 12-month rate for food and non-alcoholic beverages, while considerably lower versus April’s 19% pace, remained wholly disconcerting at 18.3%. For restaurants and hotels, the YoY pace ticked up to 10.3%. It remained above 12% for housing and household services. Notably, the contribution to the annual CPIH rate from recreation and culture was the largest in series history (the data there goes back to 2006).

A couple of days ago, while previewing this week’s BoE decision, I summarized the political and macroeconomic state of play in the UK. Long story short, Rishi Sunak has a multifaceted crisis on his hands, and the central bank has little choice but to keep raising rates until inflation comes down or the economy falls into recession, whichever comes first. I described the BoE’s inflation forecasting efforts in caustic terms, but if it’s any consolation, private sector economists haven’t done much better. Inflation has overshot consensus four months in a row with May’s upside surprise.

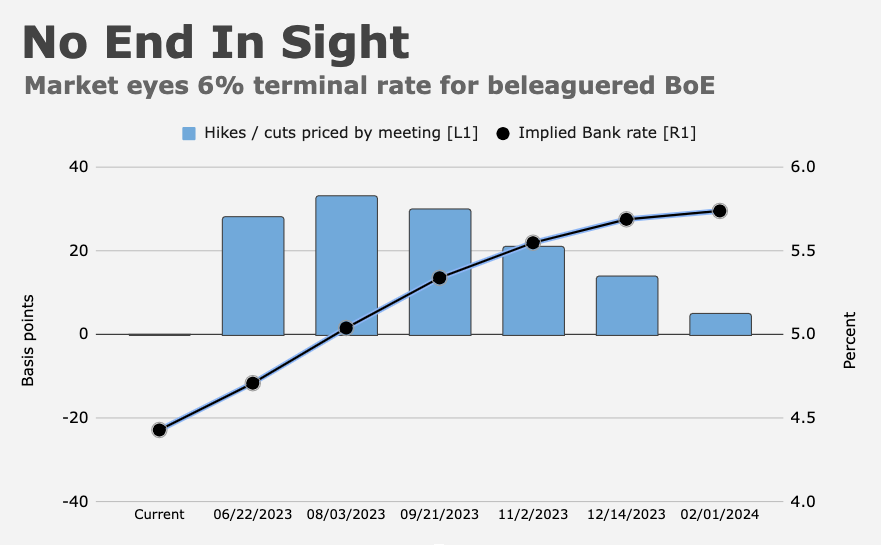

Market pricing for the terminal rate in the UK recently reflected as many as six more rate hikes. Those expectations firmed on Wednesday in the wake of the CPI figures. Plainly, a 25bps hike on Thursday is a foregone conclusion. There’s a solid argument for a half-point move, but MPC divisions and utter confusion (for lack of a better way to put it) as to the correct course of action, may prevent a re-escalation to upsized increments.

The market reaction Wednesday was concerning. Generally speaking, developed market currencies should strengthen when rate differentials move in their favor and/or when short-rates move up to reflect expectations for higher policy rates. Commentators were inclined to explain pound weakness purely as a function of recession concerns tied to prospective over-tightening from the BoE. That’s surely a factor, but I’d (gently) note that a weaker exchange rate concurrent with surging yields is EM-esque.

The UK 2s10s was the most inverted in nearly a quarter century. The optics there aren’t great, to put it mildly. Speaking of poor optics, another government report released Wednesday showed UK debt to GDP topping 100% for the first time in more than 60 years.

Two days ago, I suggested the BoE may hesitate before rebuking aggressive market pricing for terminal (as they did late last year) given the potential for such verbal intervention to further erode the bank’s credibility. “The longer inflation stays elevated, and the more times the BoE is proven wrong and forced to persist in tightening, the more justified the market is in doubting the official line,” I wrote Monday.

Following Wednesday’s CPI report, ING’s James Smith said something similar. “When rates got this high last November, the BoE offered some rare pushback [but] this time, with inflation consistently coming in hotter than expected, we suspect officials will be more reluctant to offer any firm guidance on what comes next,” he wrote. “Policymakers won’t want to steer market rate expectations lower, only to find that further inflation surprises force it to go further than it would like over the coming months.”

“May inflation surprised sharply to the upside again and further builds on April’s surprise relative to the MPC’s projections. As such, we no longer expect the MPC to push back against market pricing,” TD Securities said, in a brief update.

As ever, I’d prefer to avoid trafficking in hyperbole, but this situation is pretty dire. The figure above from TD provides some helpful context. It’s the rolling one-month change in terminal expectations across developed markets. The BoE is the clear outlier.

The bank, it seems, is being called upon to engineer a recession. Indeed, such calls were explicit from some market observers on Wednesday. Sunak promised to halve inflation this year. That may be wishful thinking.

Another quandary is the risk-reward of cushioning vulnerable households. If you’re the government, and you step in, you can do some good for the needy, but that could delay inflation’s return to more acceptable levels by forestalling demand destruction. Government officials are pondering steps to cushion the blow from higher rates to homeowners, at least a million of whom will need to refinance this year.

“The current structure of the mortgage market — whereby the vast majority of households are fixed for either two or five years — means rate hikes filter through to the economy fairly gradually [so] the length of time rates stay restrictive is arguably more important these days than the absolute level interest rates reach over the shorter-term,” ING’s Smith went on to say. “6% rates would be extremely restrictive.”

Jeremy Hunt insisted the government has to “stick to its guns.” Higher rates “do bring down inflation over time,” he said Wednesday.

{kind=link}

Besides everything else all dm’s suffer from, great britain has the adjustment from brexit. One of the dumbest moves ever.

Absolutely.

If not the dumbest.

Brexit isolation was an uneconomical position from the start. The Brits made their bed and that’s too bad for them. They didn’t want a boss that’s where they are. Funny, the meme for the UK is Prince Harry. But what we need to make sure of here is that the UK doesn’t become the meme for the US as it attempts to become more independent. The lesson is clear and following on will not be good.

pretty sure I recently read that US 2-10’s are most inverted in over 40 years…