The word “recession” came up exactly two times in minutes from the May FOMC meeting released on Wednesday afternoon. Once in the context of banks’ “substantial loss-absorbing capacity” and the other in the staff forecasts.

When asked during this month’s press conference whether Fed staff still anticipated a recession (consistent with what the minutes from March’s policy gathering revealed), Jerome Powell indicated the projections were “broadly similar,” even as he emphasized that a downturn isn’t his own assumption.

Fast forward three weeks and the minutes said staff “continued to assume that the effects of the expected further tightening in bank credit conditions, amid already tight financial conditions, would lead to a mild recession starting later this year, followed by a moderately paced recovery.” Growth, staff said, will likely “decelerate over the next two quarters before declining modestly in both the fourth quarter of this year and the first quarter of next year.”

Although Powell stressed this month that the diversity of opinions between staff and policymakers is a good thing, it’s nevertheless notable that you rarely (if ever) hear a Fed official say in public that a recession is their base case. Doing so would be to preemptively concede a policy mistake or else to acknowledge that a recession (mild or not) is the goal in light of inflation realities.

Whatever the case, the juxtaposition between the staff forecast for a recession and repeated references to additional hikes from multiple Fed officials over the past week, at least suggests the FOMC is willing to chance a downturn if it means curbing inflation.

On Wednesday, Christopher Waller echoed Jim Bullard, Neel Kashkari and Lorie Logan in emphasizing that the Fed can’t stop hiking until it’s “clear” that inflation is tamed. He expressed concern for the lack of moderation on core measures of price growth, said the labor market is still very tight, suggested the inverted yield curve could be interpreted as a sign of market confidence in the Committee’s inflation-fighting commitment and said he hopes the Fed “never” gets back into the MBS-buying business. He was, in a word, hawkish.

The May minutes suggested officials were split on whether additional hikes would be necessary. Obviously, there was quite a bit of discussion around the bank drama, and the extent to which any attendant tightening of credit conditions could substitute for additional rate hikes. Powell declined to quantify that substitution effect during the press conference, despite having put a number to it in March. The “split” passage from the minutes read as follows:

Many participants focused on the need to retain optionality after this meeting. Some participants commented that, based on their expectations that progress in returning inflation to 2% could continue to be unacceptably slow, additional policy firming would likely be warranted at future meetings. Several participants noted that if the economy evolved along the lines of their current outlooks, then further policy firming after this meeting may not be necessary.

So, June may be a pause, but it may not. Certainly, the hawks are inclined to additional hikes with inflation still running double target, although it sounds like pretty much everyone is ok with a pause next month.

The issue continues to be that markets aren’t really priced for a “pause then restart” scenario, and the fund managers you might’ve heard from on business television recently have suggested such an outcome is unthinkable. If nothing else, the odds of the Fed pausing then hiking again later this year are higher than many market participants believe. That’s a risk.

Notably (if predictably), the Fed isn’t willing to concede the possibility that RRP is working at cross purposes with financial stability. “Balances at the ON RRP facility remained within their recent range, indicating that use of the facility was not an important factor driving outflows of deposits from the banking system,” the minutes said.

Forgive me, but that’s a deliberately obtuse assessment. Of course RRP is contributing to deposit flight. Just because the total amount parked in the facility hasn’t surged even higher (or varies day to day) doesn’t mean the dynamic we can also see with our own two eyes isn’t real.

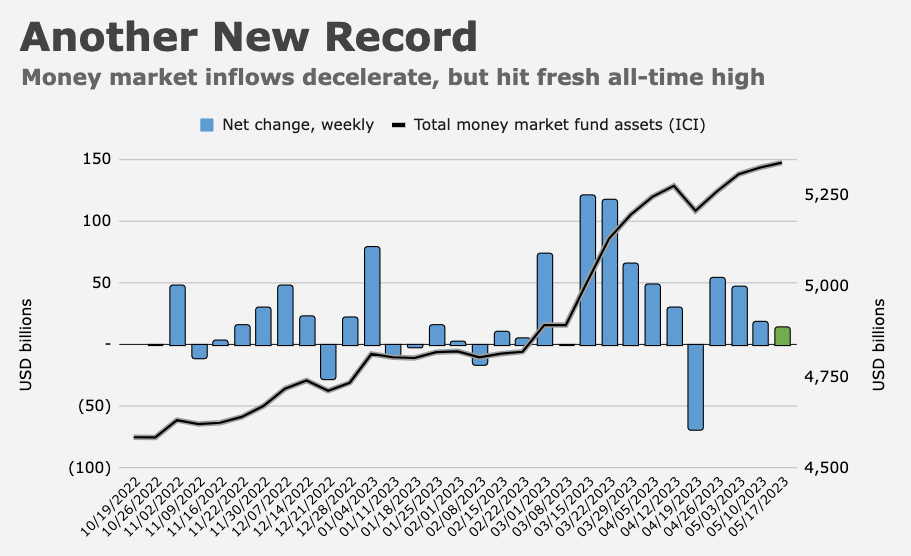

RRP usage will oscillate depending on a number of factors including rates on alternatives, but money market funds have seen inflows every week since SVB failed (with the exception of tax week). The lion’s share of that winds up in RRP. Unless you want to argue that concerns about the sanctity of bank deposits aren’t contributing to government money market fund inflows, then what other conclusion can you come to if not that RRP is at least an aggravating factor?

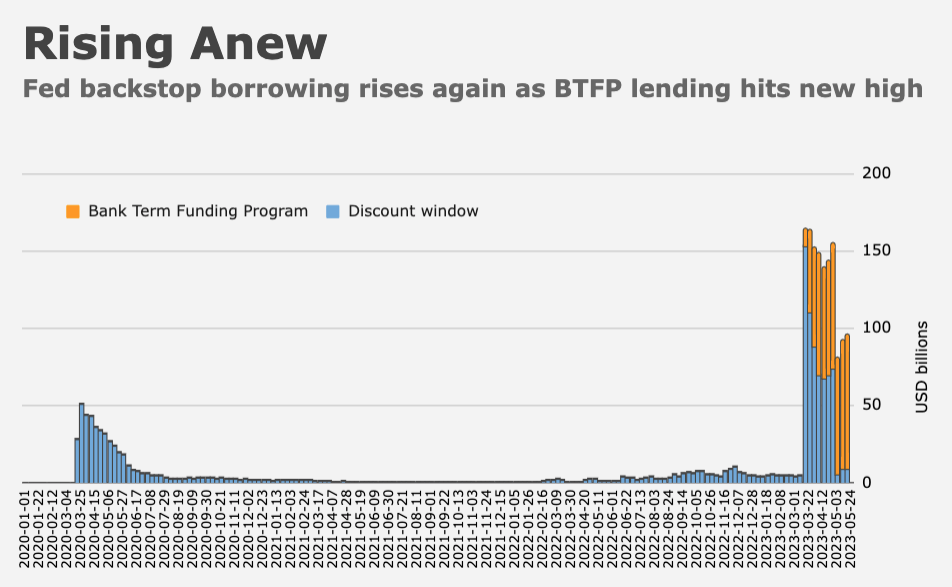

When you consider that with the fact that use of the Fed’s newly-created Bank Term Funding Program has hit record after record, the implication is that one Fed facility (RRP) is indirectly driving up borrowing from another Fed facility to the detriment of banks’ profitability. To conclude otherwise is to be deliberately obtuse or hopelessly naive and at least on this point, I don’t think the Fed is naive. It’s true that, as the minutes noted, deposit outflows have abated (or at least slowed), but the stress on individual institutions hasn’t. And as Powell learned when PacWest plunged on a scary Bloomberg headline just hours after his post-meeting press conference earlier this month, the drama can flare anew at a moment’s notice.

Anyway, “almost all participants” said downside risks to growth and upside risks to unemployment had increased “because of the possibility that banking-sector developments could lead to further tightening of credit conditions.” At the same time, “almost all participants” said “upside risks to inflation remained a key factor shaping the policy outlook.” So, stagflation then?

There was a push by the hawks to ensure the May statement wasn’t amenable to an overtly dovish spin. “Some participants stressed that it was crucial to communicate that the language in the post-meeting statement should not be interpreted as signaling either that decreases in the target range are likely or that further increases in the target range had been ruled out,” the minutes said.

{kind=link}

{kind=link}

Pause in June. And Waller is right: The Fed should never again be in the MBS-buying business.

Someone forgot to tell me when they changed the meaning of pause to peak or inflection point.

Of course they are willing to chance a recession to kill inflation. Recessions can be combated, losing your inflation fighting credibility, otoh, is more serious…