For the second time in as many policy meetings, the Fed will hike rates in the shadow of bank stress.

May’s FOMC meeting comes as First Republic, the domino that didn’t fall in March, spirals towards a denouement. Whether it’s the last domino in a very short line or one more “next shoe” on the way to a wider event is a question for 2025’s policymakers. If you get ahold of them, let me know.

Minutes from the last Fed gathering showed March’s rate hike was a close call. Staff saw a late-year recession and the meeting played out in the days after the Swiss government arranged for UBS to acquire Credit Suisse in a hastily-arranged merger. In other words: A SIFI had effectively failed. The sense of angst when officials deliberated in March was palpable. If they went ahead with a hike then, they surely will in May, particularly given evidence that inflation is entrenched across the US economy.

This week’s meeting won’t come with forecasts or dots, but if it did, officials would convey that “higher for longer” remains their base case. Or at least what they’d like for markets to believe is their base case at a time when traders continue to speculate on cuts in the back half of the year.

In the press conference, Jerome Powell will emphasize that policymakers don’t expect to be cutting rates in 2023. At “best,” cutting rates in H2 would constitute an admission that a recession is likely. At worst, it’d suggest the Fed knows that putting inflation on a sustainable path to 2% before cuts commence isn’t a goal that’s attainable, or that r-double-star is so far below r-star that inflation-targeting is now impossible unless by “targeting” you mean engineering disinflation by triggering a financial crisis.

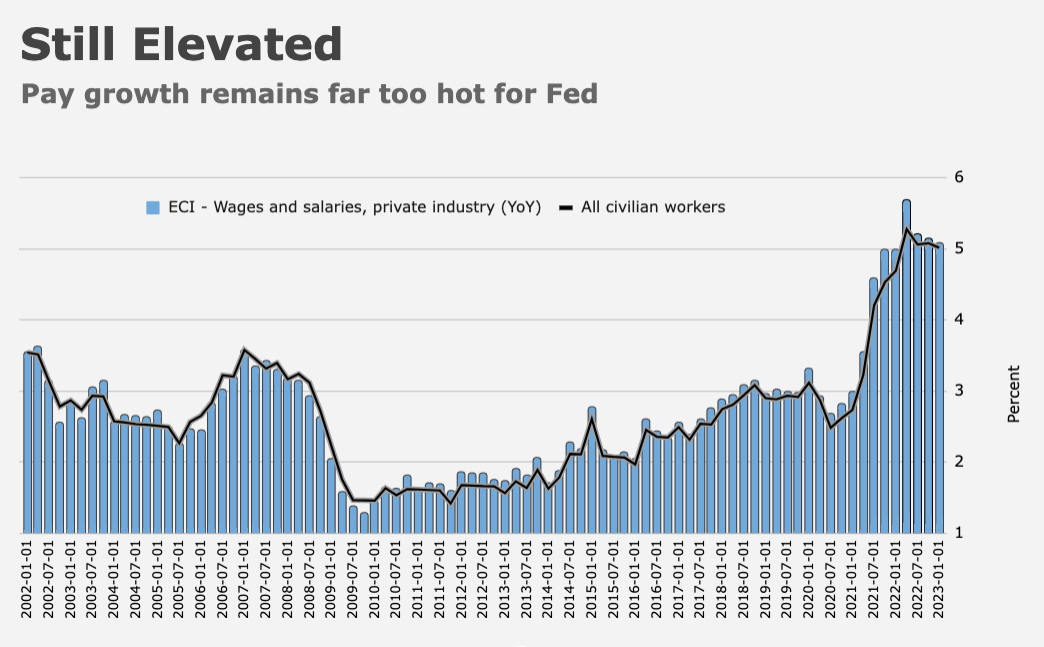

Although 2% doesn’t admit of ambiguity (inflation is either 2% or it isn’t), and while it’s impossible to argue that inflation is close enough to 2% to constitute success, the Fed has considerable leeway when it comes to suggesting inflation is “on a path” back to 2%. But core inflation is rising again on a YoY basis, the MoM prints are stubborn and wage growth is still wholly inconsistent with stable consumer prices. There’s no arguing that this job is done.

“Our best guess is that the Fed will wait until a growth scare emerges to cut rather than cutting anytime soon solely because inflation has come part way down, though we softened our stance on that a bit last month and could also imagine a combination of a convincing decline in inflation and a desire to reduce pressure on banks from a deeply inverted yield curve adding up to a reason to lower the funds rate,” Goldman analysts led by Jan Hatzius wrote, in their May FOMC preview.

“By now it is clear that there are two focal points for the Fed’s rate path outlook in 2023: The pace of inflation based on core services ex-housing PCE prices and labor market tightness,” TD analysts including Jan Groen and Oscar Munoz said. “On both accounts, trends in the corresponding data point to continued elevated inflationary pressures in the economy, suggesting the Fed has still more to do in order to gain back control over inflation dynamics.”

Note that the ECI data released late last week cast considerable doubt on the AHE figures which seemed to suggest wage growth was cooling. And core goods prices are no longer a disinflationary tailwind for policymakers. “In fact,” TD’s analysts went on to emphasize, core goods prices are now “pushing up core inflation” on a MoM basis, and the core services ex-housing measures currently “show no sign whatsoever of slowing towards a level in line with the Fed’s 2% target.”

Obviously, the specter of bank stress and never-ending recession predictions will give policymakers pause, and that could very well mean that this week’s hike is the last.

That’s Goldman’s base case, but Powell will at least try to preserve optionality. “We expect the Committee to signal that it anticipates pausing in June but retains a hawkish bias, stopping earlier than it initially envisioned because bank stress is likely to cause a tightening of credit,” Hatzius said.

The figures above show various scenarios as mapped by Goldman. Suffice to say a number of outcomes are possible and uncertainty is elevated.

The “problem” is still the labor market. The scare quotes denote that jobs are generally a good thing, but when inflation is double (or triple) target, the risk is that an acute imbalance between demand for workers and supply will keep labor costs high, prompting companies to pass along elevated wage bills to consumers in the form of higher prices, which will precipitate worker demands for even higher wages and so on.

Make no mistake: That’s already happening. It’s the reason core services inflation refuses to recede. Colloquially, it’s why you’re paying more for everything every time you leave your house. Don’t get so lost in noble, well-meaning pretensions to a literal interpretation of the term “full employment” that you can’t acknowledge reality.

The May Fed meeting comes two days before the April jobs report lands, but officials will probably have a good idea about what the numbers will show, and they’ll have March JOLTS in hand too.

The bottom line, as vexingly orthodox and as unsympathetic as it may be, is that the Fed needs to engineer job losses. The job isn’t done until the jobs are — done, I mean. We’ve danced around that for a year, and it’s deeply unpopular among progressives, but nothing else seems to be working. We may need to do it the old fashioned way, or just give up and call 4% “price stability.”

{kind=link}

In a sane world taxes would be the other option Mr. H.

Fiscal policy aimed at deliberately cooling the economy isn’t a popular notion inside the Beltway. It’s only been tried (where “tried” means with the express purpose of cooling things down) one time in modern history that I’m aware of. I doubt we’ll ever see it tried again.

Reminds me of something I read somewhere about how politicians are keen on heeding Keynes’s advice on spending their way out of a recession, but unwilling to apply the other part of Keynes’s prescription of running a budget surplus (eg by raising taxes) in good times.

The permanent state of exception only runs in one direction!

The FOMC never listens to me, but I hope they don’t overtly signal a potential pause in June lest they unleash the financial conditions roller coaster again. Stick with data dependence and the dual mandate mantra — that’s all the market needs right now. It’s not the Fed that is confusing the markets, but the economy. The Fed can’t do much about that.