The data calendar in the US is relatively sparse in the new week, which could make for an uninteresting several sessions. As one rates strategy team recently put it, “it’s summer in April.”

The docket isn’t completely bare. Starts and permits, as well as existing home sales will give market participants an opportunity to assess the extent to which the modest decline in mortgage rates from last year’s highs, alongside that spring “FOMO” feeling, are conspiring to reinvigorate housing market activity.

As a reminder, existing home sales surged in February, snapping a 12-month streak of declines in the process. Consensus expects a 1.8% decline for March, but as NAR Chief Economist Lawrence Yun put it last month, “conscious of changing mortgage rates, homebuyers are taking advantage of any rate declines.”

The average 30-year fixed has fallen every week since SVB failed. “Prospective homebuyers this year have been quite sensitive to any drop in mortgage rates,” MBA SVP Mike Fratantoni said last week, editorializing around an 8% increase in purchase apps.

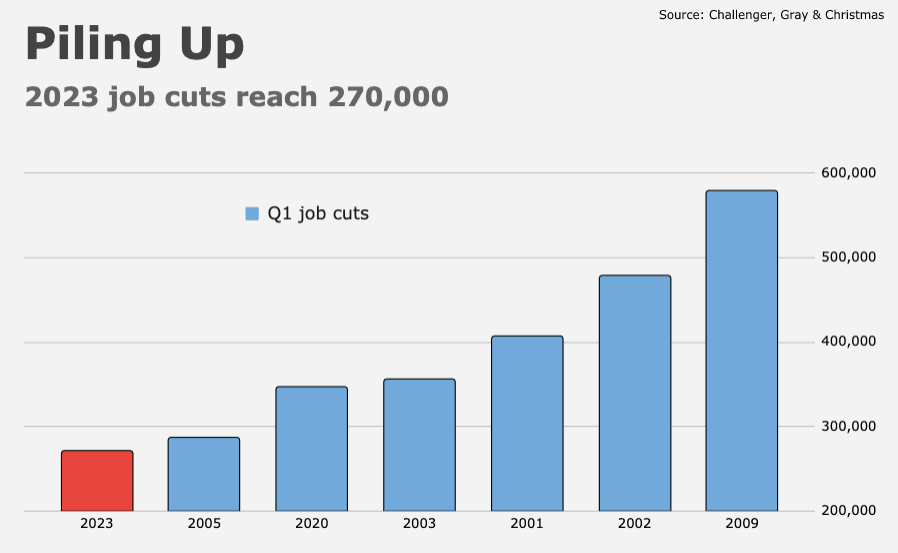

At this point, I’m somewhat agnostic about US housing. One one hand, the outlook for business spending is challenging and although consumption is (still) resilient, job cuts are piling up. The economy needs residential investment to inflect for the better. On the other hand, home prices need to stop rising. At least for a year or two. If they don’t, the “pipeline” housing disinflation the Fed is counting on to help moderate overall price growth could prove fleeting and unreliable. Somewhere, there’s a middle ground. I hope the economy can find it.

One key takeaway from last week’s relatively constructive US CPI report was that the pace of housing inflation is indeed moderating, even as it’s still far too robust for comfort.”Given the lagged impact from private-rents data and the CPI series, we believe we are going through the final passthrough of peak strength,” TD analysts including Oscar Munoz and Jan Groen said. “While we acknowledge this process is taking longer than initially expected, the March report signals that the widely anticipated shift to disinflation in shelter has finally begun.”

Here’s hoping. According to Redfin data, median rents are now falling on a YoY basis for the first time since the onset of the pandemic+. That’s the good news for America’s legions of renters. The bad news is, rents remain 20% above pre-COVID levels on an absolute basis.

Overall, the incoming data uniformly suggests the US economy is cooling, but it’s not fast enough for some Fed officials. Although Jerome Powell will likely manage to herd the proverbial cats in the interest of fostering a begrudging consensus at the Fed both among voters and nonvoters, recent public remarks suggest+ the hawks and the doves are drifting further apart.

For its part, the market still expects rate cuts commencing in the back half of the year, and the March FOMC minutes showed staff were rattled enough by the bank drama to pencil in a mild recession. Since then, though, the situation has stabilized.

Markets are fully priced for one more 25bps hike through the June meeting.

Rates traders will get a look at more bank earnings this week. That should help when it comes to refining the outlook, with the obvious caveat that it won’t be possible to assess the full impact of last month’s unfortunate events until later this year.

For what it’s worth, Goldman cut its US yield forecasts in light of what are likely to be tighter credit conditions going forward. “One month after SVB’s collapse, the risk of a disorderly broadening of banking system stress has receded, and the potential impact of the turmoil is becoming less uncertain,” the bank’s Praveen Korapaty said. “This credit tightening appears likely to have substituted for Fed hikes. A lower terminal rate level, combined with somewhat higher downside risks to the economy as a result of credit tightening, has led us to revise our US Treasury yield forecasts across the curve.”

Goldman now expects 10-year yields to end 2023 at 3.9%, 30bps below their previous forecast. Although the bank’s new target for 2s (4.4%) is a mere 40bps above current levels (given recent volatility, that could be achieved within two sessions), it’s almost 100bps above forwards. That’s a notable distinction. As Korapaty explained, “we acknowledge some amount of easing ought to be priced late in the monetary policy cycle [but] there is too much easing discounted at the front end, in our view [as] we assign a considerably lower-than-consensus probability to recession and it is not our base case.”

You can write your own script. This is an environment in which the old “your guess is as good as anyone’s” adage can be taken 100% literally.

Also on deck in the new week: Q1 GDP and March activity data out of China, flash April PMIs from S&P Global, UK inflation and a G7 foreign ministers gathering.

{kind=link}

The economy is slowing and we will are likely to get a recession. For investors, the question is how much and how much is already discounted?

It seems to me that once the Fed confirms (in the next 60 days) they’ll stop raising rates there’s going to be a surge in equities to “front run” the eventual rate reductions.

That’s an interesting timing challenge.

To be clear, I agree the macro is murky and that a run up could collapse quickly due to a recession or external events – but then you’d be playing the psychology of whether the Fed will cut more or even start QE to “help”.

It seems to me that the single most helpful thing the Fed could do for asset prices and investors is to hold long rates generally around current historically-low levels. And the only way for the Fed to do that is to decisively bring inflation down, and not let mid-single-digit inflation get even more embedded into the economy.

If inflation settles stickily in at 4-5%, what will 10 year UST rates go to? Investors demand at least a couple points of real yield, in the long run. Run stock valuations with risk free at 6-7%, look at the duration impact on bonds, think of mortgages at 9-10%, imagine what will break.

Losing control of inflation and sending the 10 Y UST at 6-7% will be more destructive to asset prices than another 50 bp of FF hikes.