Look behind the rally since mid-October and you’ll find two things: Falling rates volatility and a weaker dollar.

I’ve been over both in these pages at considerable length. December was, of course, quite onerous for US equities, but counting January, three of the last four months were very kind to beleaguered stock investors.

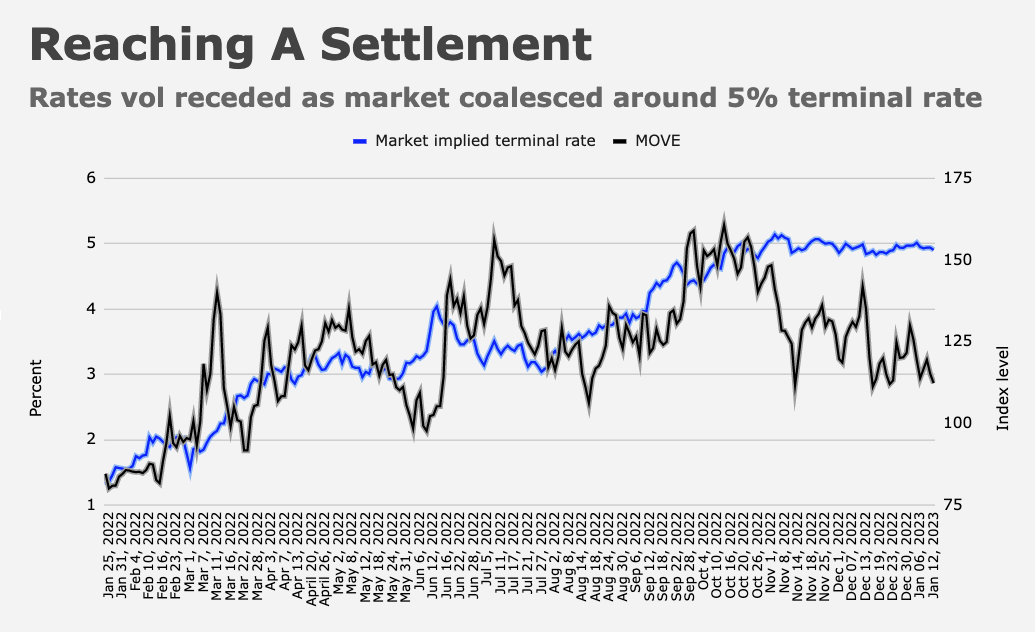

Bonds were the sponsor of 2022’s market “event,” so it’s hard to say whether the drop in rates volatility or the falling dollar is to thank for the turnaround in stocks, but both date to a tenuous truce between markets and the Fed regarding the likely peak for policy rates.

The figure above will be familiar to regular readers, and I’d note that a chart of rates vol and terminal rate pricing paints a very similar picture.

The path forward for the dollar is ambiguous, just like everything else in 2023. Last year was a “USD wrecking ball” story. The greenback’s inexorable ascent on the back of the Fed’s escalating rate-hike campaign wreaked havoc on risk sentiment and worsened terms of trade shocks in Japan and Europe.

Now, with the Fed set to downshift to 25bps hike increments ahead of an expected pause, and the US economy decelerating, there’s a fundamentals-based case for ongoing dollar weakness given ECB hawkishness, better-than-expected growth outcomes in Europe and a prospective BoJ pivot away from yield-curve control, among other factors.

That notion — that the dollar will, at the least, refrain from staging the kind of rally that helped torpedo risk assets in 2022 — is a key pillar of support for stocks. A stronger dollar and higher US real yields are kryptonite, as investors re-learned last year, and one simple visual suggests the greenback is due for a bounce.

The dollar index is down more than 8% over just a dozen weeks, a virtually unprecedented drop over such a short timeframe.

“The US dollar has rarely, if ever, had this precipitous of a decline,” Morgan Stanley’s Mike Wilson said Monday.

There’s no shortage of potential catalysts for a rebound. A hawkish Jerome Powell on Wednesday or hotter-than-expected wage growth either from Tuesday’s ECI figures or accompanying Friday’s NFP report would fit the bill, for example.

Food for thought during a week which, in addition to a deluge of top-tier economic data, includes key central bank decisions in Europe and the UK.

{kind=link}