Jerome Powell’s birthday is coming up. Upon ascending the Fed chairmanship in 2018, Powell was 65. He’ll be 93 in February.

Or at least that’s how it probably feels on some days for Powell who, during his tenure atop the Fed, has seen quite a lot. The market for VIX exchange-traded products imploded on his very first day in the big seat, and it’s been a rollercoaster since. Powell labored beneath and through a trade war, shrill social media fault-finding by America’s only twice-impeached president, a global plague, the first economic depression in nine decades, the most intense urban street protests since 1968, the sacking of the US Capitol by costumed vandals and the worst bout of developed market inflation in a generation, among other things.

It’d be too generous to suggest Powell rose to any occasion. It’s more accurate to say he didn’t fold which, considering the circumstances, is a compliment.

Some people relish the assertion, wielding and defense of power vested in their office. Powell, say what you will about the man, isn’t such a person. He’d almost surely rather have gone down as a placeholder Fed chair — the non-economist who kept the seat warm between Janet Yellen and the next “acclaimed” PhD.

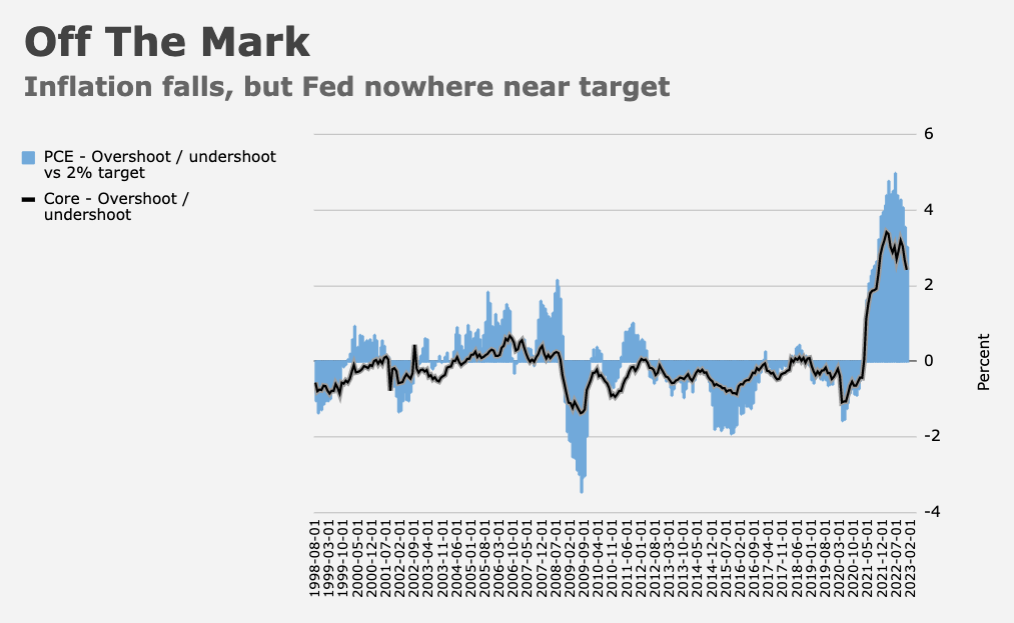

On Wednesday, three days before his 70th birthday and five years nearly to the day since he took the reins from Yellen, Powell will confront his latest challenge: Putting a hawkish spin on a second consecutive step-down in the pace of rate hikes with headline and core PCE inflation still running three and two full percentage points hotter than the Fed’s target, respectively.

The problem isn’t the trajectory of overall price growth anymore. And notwithstanding the very real risk that inflation might prove to be an unpredictable beast going forward, the issue isn’t the outlook either. The immediate concern for Powell vis-à-vis the February FOMC decision is that financial conditions have eased materially of late. Equities are off to a galloping start in 2023, real rates in the US are sharply lower and the dollar is nearly 11% off its 2022 peak. If Powell “fails” to convey enough conviction in the Fed’s intentions to reach the terminal rate tipped by the December dot plot, that chances an extension of the FCI easing impulse. And that’s to say nothing of the rate cuts that traders continue to price for the latter half of the year. In simpler terms: If Powell opens the door to a pause in March, the attendant price action in markets could effectively offset February’s 25bps rate hike.

Traders were already predisposed to fading the Committee’s pretensions to even reaching 5% Fed funds, let alone holding it for the duration of 2023. The Bank of Canada last week paired its own step-down to 25bps hikes with an explicit going-forward “hold” guide. The Fed almost certainly wouldn’t chance that just yet, but everyone knows the last hike is near. 47bps (so, not quite 50) of hikes are priced through the March meeting.

I should note that the market’s obsession with pinpointing the terminal rate is probably a bit misplaced. Late last year, Powell emphasized the evolution of the FOMC’s thinking behind rate increases. The first phase emphasized rapid hikes, while the second and third phases were centered on locating “sufficiently restrictive” and determining how long to stay there. It’s fair to assess that the Fed is now reasonably confident in the notion that the difference between 5% and 5.25% isn’t material when it comes to the “sufficiently restrictive” debate. The idea that 5% isn’t sufficiently restrictive, but 5.25% is, seems dubious. After Wednesday’s hike, the focus among policymakers will surely shift towards how long to hold terminal.

“We’re onboard with the quarter-point assumption for the next two Fed meetings and, all else being equal, also anticipate May will be in play as the final move,” BMO’s Ian Lyngen and Ben Jeffery wrote. “That said, all else is rarely equal, particularly as the spread between the February and March meetings contains two NFP and CPI reports, and as such [could] easily reveal a shift in the trajectory of the economic data that would prevent Powell from a May move,” they added.

Powell and his colleagues have tried, in vain, to disabuse markets of the idea that rate cuts are likely in the back half of the year. That effort will continue until such a time as the incoming data suggests a real recession is around the corner. The advance read on Q4 GDP was less robust than the headline print suggested. Consumption missed estimates widely, and investment decelerated. December’s personal income and spending data, released the next day, showed real spending fell into year-end.

For now, all of that’s just fine with the Fed. They want a certain amount of consumer retrenchment, and while a downshift in spending on goods is a foregone conclusion just like goods disinflation, the first flat read on real services spending (which accompanied Friday’s data) indicated Americans are pulling back where it counts for the “sticky” inflation fight.

Evidence of cooling aside, Powell will be keen to hold the line. Right, wrong or otherwise, the Fed won’t be inclined to preemptively pause on the notion that the data is backward looking. The most markets can hope for in that regard is more emphasis on the “long and variable” lags talking point, which is a tacit way of conceding the job might in fact already be done, even if policymakers can’t say as much aloud. If Powell hints that a March hike might be the last in the cycle, or if he so much as blinks in the direction of a sub-5% peak, he’ll surely undercut the dollar further, igniting a risk rally.

The last three FOMC meetings were accompanied by steep stock selloffs, and given 2023’s earliest price action, it surely wouldn’t hurt Powell’s feelings if the February meeting resulted in a similar pullback.

“Core services inflation in general is tightly linked to wage developments [and] while wage growth seemed to have eased somewhat recently, it still remains quite elevated when compared with the 3%-3.5% range that is consistent with the Fed’s 2% inflation target,” TD analysts including Jan Groen and Priya Misra said. “It is clear that the Fed’s job is not done yet and, consequently, we are expecting additional 25bps rate hikes at the March and May FOMC meetings,” they added, suggesting that in their view “sticky core services inflation will keep the Fed on hold at the terminal rate level for the remainder of the year.”

That’s really the crux of the issue going forward. The tail risk is that the “sufficiently restrictive” debate isn’t settled. It’s possible that the wage-services inflation knot proves very difficult to untangle, and that the Fed will find itself compelled to keep hiking rates past May or be forced to start hiking again later this year after a pause. If that ends up being the case, all bets are off. Figuratively and literally.

{kind=link}

You nailed it.

Perfect….

I hope Mr. Powell is a subscriber. If not, maybe a freebie, Walt?

So, the bottom line is it doesn’t really matter what Powell says. What matters is what algos, CTA’s , etc. are smoking.

Seems to me that greed is always a longer term event than fear. Therefore, there may be some kind of sell-off at 2:00 Wed. followed by a big buy the dip rally the following days. Of course, he could say 50bps and then all bets are off.

I am sympathetic to those people in their 20’s and 30’s, who are trying to put together their lives in this inflationary and/or uncertain environment.

Yeah it’s pretty annoying

Yeah, 5% with a bit of inflation is a killer. When my wife and I were putting our lives together, we had to go through an oil embargo in 1973 where gas was not just expensive, it was rationed! You could only buy gas 3 days a week and only in the county you lived in. Travel was literally impossible. Inflation was so high Nixon enacted price controls and Volcker pushed the Fed rate to 18%! In 1982, my wife and I took every dime we had a built a house. Ours was the only residential building permit approved anywhere in the county that year. The upside was that there was so little work for contractors that we got amazing prices from those folks. The bad news was, we were broke when we got done. The other good news was that interest rates on Treasuries were very high and starting to fall … for the next 35 years. Bonds beat stocks for virtually the whole period. Boy, was I lucky.

If only higher inflation were as transitory as tighter financial conditions …

I anticipate the second hawkish step down might prove harder than the first, although stocks have soared enough to start the year that some profit taking following Fed day would make sense.

I read today that the top 100 corporate pension funds had the highest surplus in 20 years; they will probably put that surplus to work in the bond market as they like to lock in decent returns? Will that drive yields down, counter to what the Fed wants?