To say it’ll be a busy week for fundamentals-focused traders and investors would be to understate the case.

The US data and earnings docket is standing-room only, with January payrolls and big-tech earnings headlining.

Consensus expects 185,000 from the headline NFP print. Recall that December’s jobs report was a “Goldilocks” affair: The headline was ahead of expectations, but not by “too” much, the unemployment rate dropped back to the lows, ostensibly arguing for Fed aggression, but an uptick in the participation rate helped temper the “good news is bad” news spin and crucially, November’s scorching-hot MoM average hourly earnings print was revised lower and December’s AHE reading was below estimates.

If January’s jobs report checks the same boxes, markets would be pleased. Economists expect the unemployment rate to move slightly higher and see another downshift in the pace of wage growth.

Note that recent jobless claims figures continued to point to a tight labor market, and there’s scant evidence to support the notion that an unprecedented imbalance between demand for workers and the supply of labor is set to resolve imminently. Still, an in line MoM AHE print would bring the 12-month pace down to 4.3%, the slowest since August of 2021. That’d be meaningful.

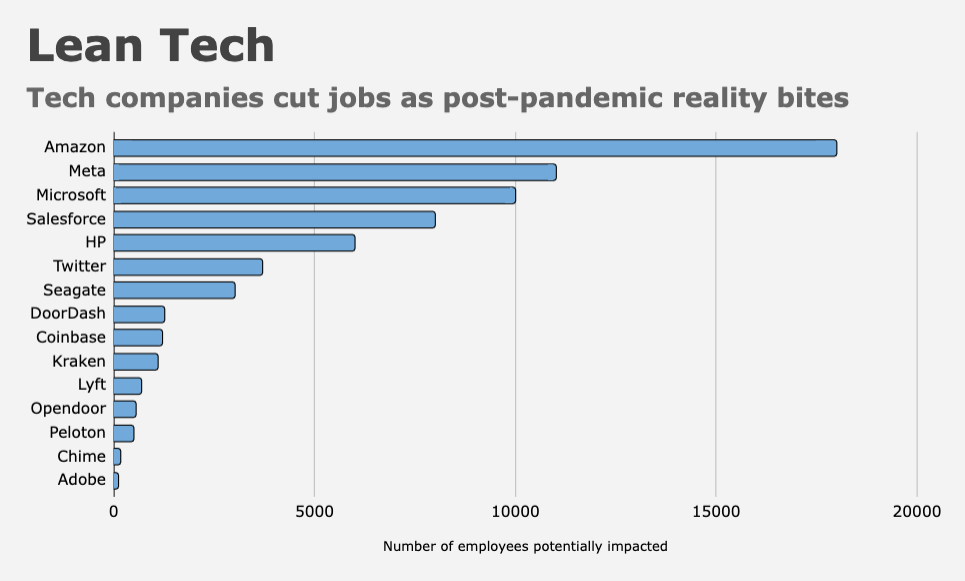

Tech layoffs have dominated the news cycle recently, but to reiterate a familiar talking point, the US economy is dependent on the willingness of modern day serfs to perform menial tasks in the services sector for pennies. The pandemic was a tipping point for that wholly unfortunate state of affairs. The serfs want more money now, God bless ’em, and if not, you can fix your own $8 latte and wait in long self-checkout lines at Walmart. That’s where the friction is. That’s where the worker shortages are. And that’s where the wage growth is. Tech layoffs are largely irrelevant to that equation.

It’s with that in mind that markets will get a look at the Q4 Employment Cost Index on Tuesday and December JOLTS on Wednesday. That one-two data punch raises the stakes for Jerome Powell who, upon delivering a 25bps rate hike on Wednesday, will face questions about wage growth and the labor market as a variable in the Fed’s decision calculus.

Recall that it was the Q3 2021 ECI report which, according to his own dramatized retelling, changed Powell’s mind about the viability of what, at the time, was a still-dovish policy bent. For most of 2022, Powell cited the JOLTS report (specifically the disparity between the headline job openings print and the number of Americans officially counted as unemployed) as evidence that a soft landing is possible.

The point: Traders and investors will get an update on both Powell’s key wage growth proxy and his soft landing rabbit’s foot in the lead up to Wednesday’s post-FOMC press conference. Consensus expects 1.1% from the ECI headline, which would still count as elevated.

As for the headline JOLTS reading, forecasters expect to hear there were around 150,000 fewer openings on the last business day of December versus the prior month.

I assume this is obvious, but what Powell (and traders) would very much like is for ECI (and the underlying wage aggregates) to come in cooler on Tuesday, and for job openings and quits to recede materially in Wednesday’s data.

It’s possible that market participants and economists will come away from this week with the impression that a wage-price spiral was successfully averted. That’d require a clean sweep across ECI, JOLTS and the AHE prints accompanying January’s jobs report, though. The more likely outcome is a continuation of the mixed messaging theme that’s defined the macro zeitgeist for months.

All of that should be contextualized by 2023’s nascent bond rally. As BMO’s Ian Lyngen and Ben Jeffery put it, “confirmation that the Fed has managed to avoid a wage-inflation spiral will further reinforce the peak rates dynamic and, regardless of the NFP move, contribute to the building bullishness in the Treasury market.”

In addition to NFP, ECI and JOLTS, traders can look forward to Conference Board confidence, ISM manufacturing and services, factory orders, home price data from FHFA and Case-Shiller as well as unit labor costs and productivity figures for Q4. Those latter numbers are also relevant for the macro narrative.

On the earnings front, Meta reports on Wednesday, followed by Alphabet, Amazon and Apple on Thursday.

{kind=link}