I don’t think I can remember a time when such a stupendous (and stupefying) rally across traditional assets was so readily relegated to obscurity by financial media portals.

This week’s CPI-driven barnburner on Wall Street was the stuff headlines are made of, only not when crypto’s most recognizable mogul is busy taking his empire into bankruptcy.

I understand why the Sam Bankman-Fried debacle is the biggest story in the financial universe. If I didn’t, I surely wouldn’t have spent as much time as I did editorializing around it. But lest we should totally lose the plot (and our sanity along with it), I think it’s important to note that whether FTX is or isn’t Lehman from the perspective of journalists, it most assuredly isn’t Lehman from the perspective of serious market participants. Suggesting as much will get you laughed out of any room where serious people are (assuming there are any such rooms left in 2022).

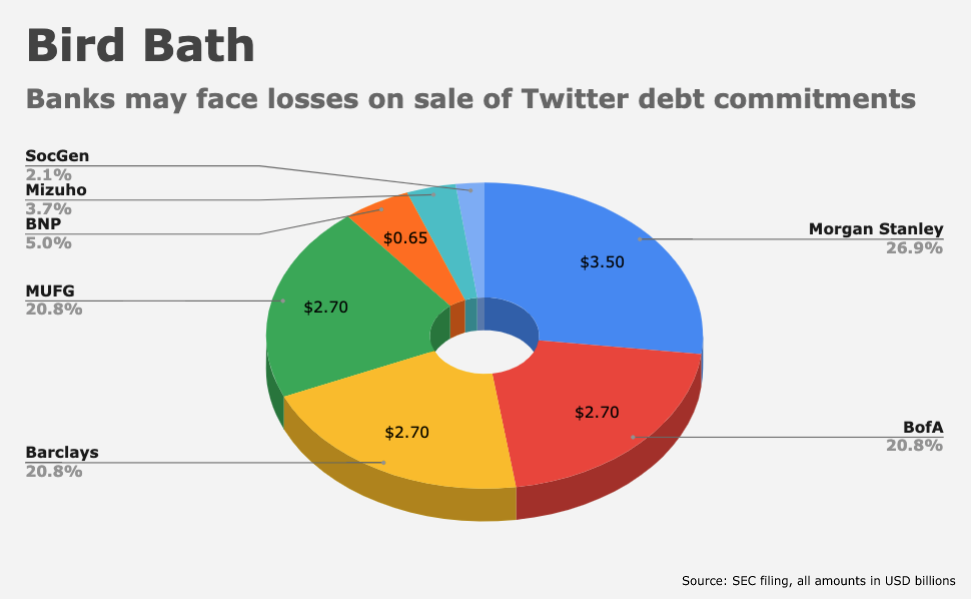

Relatedly, the Elon Musk-Twitter soap opera is only relevant for what it says about the perils of entrusting one man to administer the proverbial “town square” and, more existentially, what Musks’s early stumbles might mean for his tenure as a surveillance capitalist. Those are social issues, though. For the market, the only thing that matters now with regard to Musk and Twitter, is whether he’s too preoccupied to run Tesla and whether the banks that helped finance the deal end up stuck with billions in losses on the commitments (initial offers on the buyout debt were reportedly as low as 60 cents on the dollar).

What matters more than FTX and Twitter is that, according to at least one technical analyst (and regular readers know how much I revere technicians), “the bear as we know it is dead, and a new bull has begun.” That’s a quote from Evercore’s Rich Ross.

I’ll leave it to people who divine the arrival of spirit animals from imaginary lines superimposed on squiggles to declare the onset of a new, secular trend in stocks. All I’d note is that while everyone was busy documenting every twist and turn in the FTX saga and tweeting about Twitter, the world’s foremost gauge of large US tech companies surged 9%, among the best weekly showings since the dot-com days (simple figure below).

Take a moment to internalize everything I’ve just said. Market participants and media outlets dedicated a very large share of mental bandwidth, digital ink and air time this week to i) the implosion of an exchange where people trade made-up money and ii) one guy’s attempt to extract $8 from social media users for the privilege of having a blue star appended to their profiles, while the biggest and most important technology companies on Earth were in the process of gaining nearly 10% in value collectively in the space of five days.

I’m not feeling especially generous this week when it comes to sugarcoating the issues that concern us all, so allow me to call that silly. There’s no sense (none) in which FTX or Twitter are deserving of more coverage than US equities, if what we’re talking about are markets, narrowly construed (i.e., if we set aside the myriad questions posed by crypto as a concept and by Musk as the owner of people’s data).

The financial media isn’t a competition for the best coverage. It’s a competition for attention. So, this week, they waved the crashing arcade tokens around, and whenever there was a 15 minute break in Bankman-Fried news, they filled it up with whatever Elon Musk was tweeting. By Saturday morning, we’d come full circle: Musk was imploring market participants to follow the latest news on FTX’s bankruptcy on Twitter, which Elon reportedly suggested might itself go bankrupt. “FTX meltdown/ransack being tracked in real-time on Twitter,” he said, in a tweet, at 1:14 AM in New York. Insert laugh track.

In any event, it wasn’t just big-cap tech that put on an astounding show this week. Another simple figure (below) shows that five-year US yields fell the most since the original COVID drama on the heels of October CPI. During any other week, that’d be a top story on its own.

The bond rally was accompanied by a dramatic repricing of Fed terminal rate expectations. In the hours after the CPI report, the fourth eurodollar contract rallied the most since the financial crisis.

“We’ll argue the most consequential session for the US rates market before the next CPI report on December 13th is in hand. Coming into the week, the chatter had been waning bearish conviction as shorts were covered and those who were underweight duration have moved neutral,” BMO’s Ian Lyngen and Ben Jeffery said, of rates. “The market is transitioning from a bias to sell rallies in favor of buying dips, and it’s this stance we expect will become increasingly relevant as the specter of a hard landing solidifies.”

And how about the dollar? While journalists were wearing out thesaurus.com in an effort to out-hyperbole their last crypto collapse article, the world’s reserve currency fell by the second-most in at least 30 years (figure below).

Suffice to say that’s helpful for risk assets, unhelpful for the Fed and a massive relief for currencies not called the dollar, even as it was small comfort for “currencies” that aren’t currencies, which were busy fretting over a five-alarm blaze at some guy’s defunct casino.

The gravity of what transpired in real markets this week wasn’t lost on SPI Asset Management’s Stephen Innes. “This is clearly on top of catch-up FOMO trades after the softer US CPI caught the street flatfooted,” he wrote. “If there’s an interpretation to be had, investors were far from being positioned for good inflation news, with massive amounts of cash on the sidelines.”

On the eve of the CPI report, the Long-Short crowd’s beta to the S&P sat in just the 0.7%ile on a one-month rolling basis looking back two decades. Those figures for mutual funds and macro hedge funds were 26%ile and 18%ile, respectively.

“Even if you were betting CPI would come in soft, there was just no way to position for this kind of generational 36-hour move,” Innes went on to say. “‘Could have,’ ‘should have,’ ‘would have’ is a lousy way for a trader to end the week.”

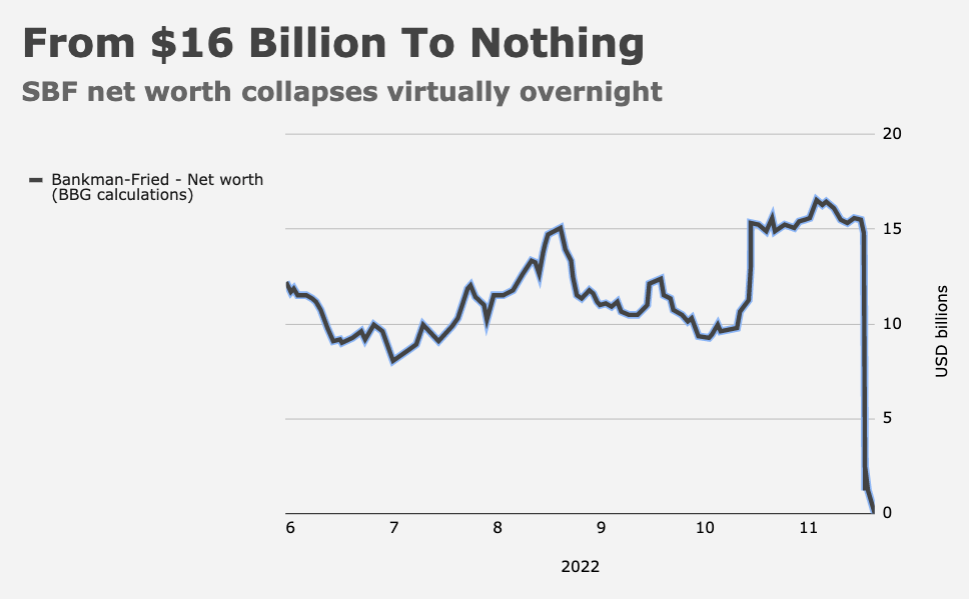

Indeed. But, for anyone who missed the rally, look at the bright side: It could’ve been worse. You could’ve lost $16 billion in five days.

{kind=link}

{kind=link}

I’m never clear whether it’s a good idea to talk about price without volume. It’s been seeming to me that volumes have been thin lately overall, lots of things I’ve been trading have been annoyingly volatile. Maybe this “generational” event could only have happened precisely because nobody was positioned for it; everybody was sitting out so price rebounded hard on thin volume.

I dunno. Glancing at the charts it doesn’t look like volume is that low, but it’s nowhere near as high as it was at the major bottoms (or tops) of the last few years. I personally just trade my rules and don’t try to forecast, but, until I see evidence that this happened on volume, I’m still trading on the basic assumption that we’re in a bear market. I’m thinking twice before going long on anything.

I’d argue that liquidity is more important than volume if you’re looking to assess the extent to which a given move is reliable. The two are sometimes related, but they aren’t the same. Liquidity is impaired across virtually all assets. That opens the door to large swings. When you throw in low volume, you’ve got a recipe for fireworks.

A question for yiu, SBR. Did the arrival of high frequency traders change your view of the predictive value of that indicator?

Do they simply put a “floor” under the expected daily volumes? I’ve wondered how technical traders are handling this.

Strangely enough, it does tie in with what our Dear Leader just wrote when it comes to volume versus liquidity, doesn’t it?

It is absolutely crazy that I trust H, a human that I do not know very much about, over any known media reporters, analysts or investment/financial gurus.

Thanks for your endless commitment to your readers. I always know if your publish something, it is because you think we should know about what you are saying.

Out of everyone who’s attempted to sketch a portrait of me over the years in comments, you’ve hit the nail on the head a couple of times, although I won’t say in which comments, because that’d ruin the fun.

🙂

Maybe it’s just the subject matter that you’ve summarized so well, but I enjoyed reading this piece more than anything of yours I can recall previously. It truly was a bizarre day/week. And you’ve pointed that out better than anyone.

And yet…..H left out the political fireworks,which made this the wildest week I can remember…….as well as a weekty that restored some of my lost optimism.

Let me make a case for using technical analysis, those “imaginary lines superimposed on squiggles” as H would have it. Let me first say that I am not a ‘true believer’ who actually is convinced that there is any particular scientific truth in any given technical signal; I am agnostic regarding that.

But scientific truth doesn’t matter a whit, with markets. What matters is if a critical mass of market participants believe enough in these market signals to act upon them. If enough people put enough money to work on the belief that sunny Mondays always end bullishly, then sunny Mondays will end bullishly much of the time. And to not pay attention to that belief while being a market participant, when so many others do believe it and act on it, is foolish. Just look at how buy recommendations by influential analysts often become self-fulfilling prophecies by the crowd jumping aboard the bandwagon.

Markets, though influenced by many fundamental factors, are very human constructs driven by strong emotions. Thus, if a technical signal is accepted as having value by a substantial part of those who are trading markets and they act upon that belief there is a decent chance that the signal will prove ‘true’.

I started out trading looking purely using fundamentals and still pay attention to them, but so many things that happened in my trading only became understandable when I started to pay attention to technical signals. And I have made pretty good money trading for my own account for several decades by paying close attention to certain patterns and acting upon them.

This rally began with an enormous engulfing candle (look it up) on October 13 on strong volume along with positive divergences in the MACD and RSI and probably other secondary signals. A positive divergence is when the price is lower than the previous low, but the MACD or RSI is higher than the previous low. Many of us were waiting for that kind of signal then, because of seasonal tendencies (markets usually bottom in mid-October) and the historically bad positioning in October of those who run money and the fact that their year end bonuses, which are a huge part of their annual comp, were now in peril.

Plus, so many who were going to sell, had already sold and so there was so much cash on the sidelines and finally there were a lot of shorts and puts in the market. Morning of the 13th, in the futures there was a bloodbath of a sell off, which had the look of a capitulation bottom. When shorts started to cover and puts were sold and calls bought, the rally was on despite whatever terrible news had caused the sell off in the futures (news is only important in what the market reaction is, not the news itself. Bad news that causes a market to rally is very bullish)

Now the market is basically bullying those money managers in peril into buying into year end and is also seeing some of that cash coming off the sidelines, something that can snowball the higher we go and commentators begin predicting a new bull. I personally don’t see a new bull market coming, although if Putin fell out of a 6th story window or the mullahs fell in Iran, it could happen, but I am happy to make 15 to 20% on the sharp rallies bear markets afford us, before going to cash. I personally think we will have a long bear market, punctuated by more sharp rallies. The eventual bottom will be much lower than the October 13 bottom and is quite a few years away.

By the way I did mention that I had become very bullish on the markets in these very comments a few days after October 13, although I have no idea how I would find those comments again, unfortunately.